Taxation history of the United States

Encyclopedia

The history of taxation in the United States

began when it was composed of colonies

ruled by the British Empire

, French Empire

, and Spanish Empire

. After independence from Europe

the United States collected poll taxes, tariffs

, and excise taxes. The United States imposed income taxes

intermittently until 1895 when unapportioned taxes on interest, dividends and rents were ruled unconstitutional. The advent of the 16th Amendment

to the United States Constitution

modified the apportionment requirement in 1913, and since then the income tax has become one of the means of funding the Federal Government

.

passed by the Parliament of Great Britain

. It revised the earlier Sugar and Molasses Act

, which had imposed a tax of six cents per gallon upon imported molasses in order to make English products cheaper than those from the French West Indies

.

The Stamp Act of 1765 was the fourth Stamp Act to be passed by the Parliament of Great Britain and required all legal documents, permits, commercial contracts, newspapers, wills, pamphlets, and playing cards in the American colonies to carry a tax stamp. The exact date the Act was enacted was on November 1, 1765. The Act was enacted in order to defray the cost of maintaining the military presence protecting the colonies.

passed in 1767, which were proposed by Charles Townshend

, Chancellor of the Exchequer

, just before his death. These law

s placed a tax

on common products imported into the American Colonies

, such as lead, paper, paint, glass, and tea (though they did not place a tax on silk

). In contrast to the Stamp Act of 1765

, the laws were not a direct tax, but a tax on imports. The Townshend Acts also created three new admiralty court

s to try Americans who ignored the laws.

of 1773 was received the royal assent on May 10, 1773. This act was a "drawback on duties and tariffs" on tea. The act was designed to undercut tea smugglers to the benefit of the East India Company

.

The Boston Tea Party was an act of protest

by the American colonists against Great Britain

for the Tea Act

in which they destroyed many crate

s of tea brick

s on ships in Boston Harbor

. The incident, which took place on Thursday, December 16, 1773, has been seen as helping to spark the American Revolution

.

. Tariffs were the largest source of federal revenue from the 1790s to the eve of World War I

, until it was surpassed by income taxes. Since the revenue from the tariff was considered essential and easy to collect at the major port

s, it was agreed the nation should have a tariff for revenue purposes.

; it was the political dimension of the tariff. From the 1790s to the 2000s, the tariff (and closely related issues such as import quotas and trade

treaties) generated enormous political stresses whether during the 19th century with the Nullification crisis

or the WTO.

was the United States Secretary of the Treasury

he issued the Report on Manufactures

, which reasoned that applying tariffs in moderation, in addition to raising revenue to fund the federal government, would also encourage domestic manufacturing and growth of the economy by applying the funds raised in part towards subsidies (called bounties in his time) to manufacturers. The main purposes sought by Hamilton through the tariff were to: (1) protect American infant industry for a short term until it could compete; (2) raise revenue to pay the expenses of government; (3) raise revenue to directly support manufacturing through bounties (subsidies). This resulted in the passage of three tariffs by Congress, the Tariff of 1789, the Tariff of 1790

, and the Tariff of 1792

which progressively increased tariffs.

increased tariffs in order to protect American industry in the face of cheaper imported commodities such as iron products, wool and cotton textiles, and agricultural goods from England. This tariff was the first in which the sectional interests of the North and the South truly came into conflict because the South advocated lower tariffs in order to take advantage of tariff reciprocity from England and other countries that purchased raw agricultural materials from the South.

The Tariff of 1828

, also known as the Tariff of Abominations, and the Tariff of 1832

accelerated sectionalism between the North and the South. For a brief moment in 1832, South Carolina made vague threats to leave the Union over the tariff issue. In 1833, to ease North-South relations, Congress lowered the tariffs. In the 1850s, the South gained greater influence over tariff policy and made subsequent reductions.

In 1861, just prior to the Civil War, Congress enacted the Morrill Tariff

, which applied high rates and inaugurated a period of relatively continuous trade protection in the United States that lasted until the Underwood Tariff of 1913. The schedule of the Morrill Tariff and its two successor bills were retained long after the end of the Civil War.

, which increased rates on wheat

, sugar

, meat

, wool

and other agricultural products brought into the United States

from foreign nations, which provided protection for domestic producers of those items.

However, one year later Congress passed another tariff, the Fordney-McCumber Tariff

, which applied the scientific tariff and the American Selling Price. The purpose of the scientific tariff was to equalize production costs among countries so that no country could undercut the prices charged by American companies. The difference of production costs was calculated by the Tariff Commission. A second novelty was the American Selling Price. This allowed the president to calculate the duty based on the price of the American price of a good, not the imported good.

During the outbreak of the Great Depression in 1930, Congress raised tariffs on over 20,000 imported goods to record levels, and, in the opinion of most economists, worsened the Great Depression by causing other countries to reciprocate thereby plunging American imports and exports by more than half.

(GATT), which reduced tariff barriers and other quantitative restrictions and subsidies on trade through a series of agreements.

In 1993 the GATT was updated (GATT 1994) to include new obligations upon its signatories. One of the most significant changes was the creation of the World Trade Organization

(WTO). Whereas GATT was a set of rules agreed upon by nations, the WTO is an institutional body. The WTO expanded its scope from traded goods to trade within the service sector and intellectual property rights. Although it was designed to serve multilateral agreements, during several rounds of GATT negotiations (particularly the Tokyo

Round) plurilateral agreements created selective trading and caused fragmentation among members. WTO arrangements are generally a multilateral agreement settlement mechanism of GATT.

Federal excise taxes are applied to specific items such as motor fuels, tires, telephone usage, tobacco products, and alcoholic beverages. Excise taxes are often, but not always, allocated to special funds related to the object or activity taxed.

the power to impose "Taxes, Duties, Imposts and Excises," but Article I, Section 8 requires that, "Duties, Imposts and Excises shall be uniform throughout the United States."

In addition, the Constitution specifically limited Congress' ability to impose direct taxes, by requiring it to distribute direct taxes in proportion to each state's census population. It was thought that head taxes and property tax

es (slaves could be taxed as either or both) were likely to be abused, and that they bore no relation to the activities in which the federal government had a legitimate interest. The fourth clause of section 9 therefore specifies that, "No Capitation, or other direct, Tax shall be laid, unless in Proportion to the Census or enumeration herein before directed to be taken."

Taxation was also the subject of Federalist No. 33

penned secretly by the Federalist Alexander Hamilton

under the pseudonym

Publius. In it, he explains that the wording of the "Necessary and Proper" clause should serve as guidelines for the legislation of laws regarding taxation. The legislative branch is to be the judge, but any abuse of those powers of judging can be overturned by the people, whether as states or as a larger group.

What seemed to be a straightforward limitation on the power of the legislature based on the subject of the tax proved inexact and unclear when applied to an income tax, which can be arguably viewed either as a direct or an indirect tax. The courts have generally held that direct taxes are limited to taxes on people (variously called "capitation", "poll tax" or "head tax") and property. All other taxes are commonly referred to as "indirect taxes," because they tax an event, rather than a person or property per se.

, Congress imposed its first personal income tax in 1861. It was part of the Revenue Act of 1861

(3% of all incomes over US $800; rescinded in 1872). Congress also enacted the Revenue Act of 1862

, which levied a 3% tax on incomes above $600, rising to 5% for incomes above $10,000. Rates were raised in 1864. This income tax was repealed in 1872.

A new income tax statute was enacted as part of the 1894 Tariff Act. At that time, the United States Constitution

specified that Congress could impose a "direct" tax only if the law apportioned that tax among the states according to each state's census

population.

In 1895, the United States Supreme Court ruled, in Pollock v. Farmers' Loan & Trust Co.

, that taxes on rent

s from real estate, on interest

income from personal property and other income from personal property (which includes dividend

income) were direct taxes on property and therefore had to be apportioned. Since apportionment of income taxes is impractical, the Pollock rulings had the effect of prohibiting a federal tax on income from property. Due to the political difficulties of taxing individual wages without taxing income from property, a federal income tax was impractical from the time of the Pollock decision until the time of ratification of the Sixteenth Amendment (below).

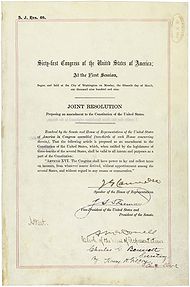

In response to the Supreme Court decision in the Pollock case, Congress proposed the Sixteenth Amendment

In response to the Supreme Court decision in the Pollock case, Congress proposed the Sixteenth Amendment

, which was ratified in 1913, and which states:

The Supreme Court

in Brushaber v. Union Pacific Railroad

, , indicated that the Sixteenth Amendment did not expand the federal government's existing power to tax income (meaning profit or gain from any source) but rather removed the possibility of classifying an income tax as a direct tax on the basis of the source of the income. The Amendment removed the need for the income tax on interest, dividends and rents to be apportioned among the states on the basis of population. Income taxes are required, however, to abide by the law of geographical uniformity.

Congress enacted an income tax in October 1913 as part of the Revenue Act of 1913

, levying a 1% tax on net personal incomes above $3,000, with a 6% surtax on incomes above $500,000. By 1918, the top rate of the income tax was increased to 77% (on income over $1,000,000) to finance World War I

. The top marginal tax rate was reduced to 58% in 1922, to 25% in 1925 and finally to 24% in 1929. In 1932 the top marginal tax rate was increased to 63% during the Great Depression

and steadily increased, reaching 94% (on all income over $200,000) in 1945. During World War II, Congress introduced payroll withholding and quarterly tax payments.

Top marginal tax rates stayed near or above 90% until 1964 when the top marginal tax rate was lowered to 70%. The top marginal tax rate was lowered to 50% in 1982 and eventually to 28% in 1988. It slowly increased to 39.6% in 2000, then was reduced to 35% for the period 2003 through 2010.

on incomes above $500,000. By 1918, the top rate of the income tax was increased to 77% (on income over $1,000,000) to finance World War I

. The top marginal tax rate was reduced to 58% in 1922, to 25% in 1925, and finally to 24% in 1929. In 1932 the top marginal tax rate was increased to 63% during the Great Depression

and steadily increased.

During World War II, Congress introduced payroll withholding and quarterly tax payments, Franklin D. Roosevelt

tried to impose a 100% tax on all incomes over $25,000 to help with the war effort. For tax years 1944 through 1951, the highest marginal tax rate for individuals was 91%, increasing to 92% for 1952 and 1953, and reverting to 91% for tax years 1954 through 1963.

For the 1964 tax year, the top marginal tax rate for individuals was lowered to 77%, and then to 70% for tax years 1965 through 1981. The top marginal tax rate was lowered to 50% for tax years 1982 through 1986.

For tax year 1987, the highest marginal tax rate was 38.5% for individuals. It was lowered to 28%, eliminating many loopholes and shelters, (with a 33% "bubble rate") for tax years 1988 through 1990.

For the 1991 and 1992 tax years, the top marginal rate was increased to 31% in a budget deal President George H. W. Bush

made with the Congress.

In 1993 the Clinton

administration proposed and the Congress accepted (with no Republican support) an increase in the top marginal rate to 39.6% for the 1993 tax year, where it remained through tax year 2000.

In 2001, President George W. Bush

proposed and the Congress accepted an eventual lowering of the top marginal rate to 35%. However, this was done in stages: with a highest marginal rate of 39.1% for 2001, then 38.6% for 2002 and finally 35% for years 2003 through 2010. This measure had a sunset provision and was scheduled to expire for the 2011 tax year, when rates would have returned to those adopted during the Clinton years unless Congress changed the law; Congress did so by passing the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010, signed by President Barack Obama on December 17, 2010.

At first the income tax was incrementally expanded by the Congress of the United States, and then inflation automatically raised most persons into tax bracket

s formerly reserved for the wealthy until income tax brackets were adjusted for inflation. Income tax now applies to almost two-thirds of the population. The lowest earning workers, especially those with dependents, pay no income taxes as a group and actually get a small subsidy from the federal government because of child credits and the Earned Income Tax Credit

.

While the government was originally funded via tariff

s upon imported goods, tariffs now represent only a minor portion of federal revenues. Non-tax fees are generated to recompense agencies for services or to fill specific trust funds such as the fee placed upon airline ticket

s for airport expansion and air traffic control

. Often the receipts intended to be placed in "trust" funds are used for other purposes, with the government posting an IOU

('I owe you') in the form of a federal bond or other accounting instrument, then spending the money on unrelated current expenditures.

Net long-term capital gain

s as well as certain types of qualified dividend

income are taxed preferentially. The federal government collects several specific taxes in addition to the general income tax. Social Security

and Medicare

are large social support programs which are funded by taxes on personal earned income (see below).

The modern interpretation of the Sixteenth Amendment taxation power can be found in Commissioner v. Glenshaw Glass Co.

. In that case, a taxpayer had received an award of punitive damages from a competitor, and sought to avoid paying taxes on that award. The Court observed that Congress, in imposing the income tax, had defined income to include:

The Court held that "this language was used by Congress to exert in this field the full measure of its taxing power", id., and that "the Court has given a liberal construction to this broad phraseology in recognition of the intention of Congress to tax all gains except those specifically exempted."

The Court then enunciated what is now understood by Congress and the Courts to be the definition of taxable income, "instances of undeniable accessions to wealth, clearly realized, and over which the taxpayers have complete dominion." Id. at 431. The defendant in that case suggested that a 1954 rewording of the tax code had limited the income that could be taxed, a position which the Court rejected, stating:

In Conner v. United States, a couple had lost their home to a fire, and had received compensation for their loss from the insurance company, partly in the form of hotel costs reimbursed. The court acknowledged the authority of the IRS to assess taxes on all forms of payment, but did not permit taxation on the compensation provided by the insurance company, because unlike a wage or a sale of goods at a profit, this was not a gain. As the court noted, "Congress has taxed income, not compensation". By contrast, at least two other Federal courts have indicated that Congress may constitutionally tax an item as "income," regardless of whether that item is in fact income. See Penn Mutual Indemnity Co. v. Commissioner and Murphy v. Internal Revenue Serv.

The origins of the estate and gift tax occurred during the rise of the state inheritance tax in the late 19th century and the progressive era

.

In the 1880s and 1890s many states passed inheritance taxes, which taxed the donees on the receipt of their inheritance. While many objected to the application of an inheritance tax, some including Andrew Carnegie

and John D. Rockefeller

supported increases in the taxation of inheritance.

At the beginning of the 20th century President Theodore Roosevelt

advocated the application of a progressive inheritance tax on the federal level.

In 1916, Congress adopted the present federal estate tax, which instead of taxing the wealth that a donee inherited as occurred in the state inheritance taxes it taxed the wealth of a donor's estate upon transfer.

Later, Congress passed the Revenue Act of 1924

, which imposed the gift tax, a tax on gifts given by the donor.

In 1948 Congress allowed marital deductions for the estate and the gift tax. In 1981, Congress expanded this deduction to an unlimited amount for gifts between spouses.

Today, the estate tax is a tax imposed on the transfer of the "taxable estate

" of a deceased person, whether such property is transferred via a will

or according to the state laws of intestacy

. The estate tax is one part of the Unified Gift and Estate Tax system in the United States. The other part of the system, the gift tax, imposes a tax on transfers of property during a person's life; the gift tax prevents avoidance of the estate tax should a person want to give away his/her estate just before dying.

In addition to the federal government, many states also impose an estate tax, with the state version called either an estate tax or an inheritance tax

. Since the 1990s, the term "death tax" has been widely used by those who want to eliminate the estate tax, because the terminology used in discussing a political issue affects popular opinion.

If an asset is left to a spouse or a charitable organization, the tax usually does not apply. The tax is imposed on other transfers of property made as an incident of the death of the owner, such as a transfer of property from an intestate estate or trust, or the payment of certain life insurance

benefits or financial account sums to beneficiaries.

, the following economic problems were considered great hazards to working-class Americans:

introduced Social Security

to rectify the first three problems (retirement, injury-induced disability, or congenital disability). It introduced the FICA tax as the means to pay for Social Security.

In the 1960s, Medicare

was introduced to rectify the fourth problem (health care for the elderly). The FICA tax was increased in order to pay for this expense.

introduced the Social Security (FICA) Program. FICA began with voluntary participation, participants would have to pay 1% of the first $1,400 of their annual incomes into the Program, the money the participants elected to put into the Program would be deductible from their income for tax purposes each year, the money the participants put into the independent "Trust Fund" rather than into the General operating fund, and therefore, would only be used to fund the Social Security Retirement Program, and no other Government program, and, the annuity payments to the retirees would never be taxed as income.

During the Lyndon B. Johnson

administration Social Security moved from the trust fund to the general fund. Participants may not have an income tax deduction for Social Security withholding. Immigrants became eligible for Social Security benefits during the Carter administration. During the Reagan administration Social Security annuities became taxable.

Some lower income individuals pay a proportionately higher share of payroll taxes for Social Security

and Medicare

than do some higher income individuals in terms of the effective tax rate. All income earned up to a point, adjusted annually for inflation ($94,200 for the year 2006 and $97,500 for the year 2007) is taxed at 7.65% (consisting of the 6.2% Social Security tax and the 1.45% Medicare tax) on the employee with an addition 7.65% in tax incurred by the employer. The annual limitation amount is sometimes called the "Social Security tax wage base amount" or "Contribution and Benefit Base." Above the annual limit amount, only the 1.45% Medicare tax is imposed. In terms of the effective rate, this means that a worker earning $20,000 for 2006 pays at a 7.65% effective rate ($1,530) while a worker earning $200,000 pays at an effective rate of about 4.37% ($8,740).

Self employed people pay the entire 15.3%, but are allowed to deduct one-half of this amount in computing taxable income for Federal income tax purposes. These taxes fund the Social Security Trust Fund

and Medicare Trust Funds.

, and became operative in 1970. It was intended to target 155 high-income households that had been eligible for so many tax benefits that they owed little or no income tax under the tax code of the time.

In recent years, the AMT has been under increased attention. With the Tax Reform Act of 1986

, the AMT was broadened and refocused on home owners in high tax states. Because the AMT is not indexed to inflation and recent tax cuts, an increasing number of middle-income taxpayers have been finding themselves subject to this tax.

In 2006, the IRS's National Taxpayer Advocate's report highlighted the AMT as the single most serious problem with the tax code. The advocate noted that the AMT punishes taxpayers for having children or living in a high-tax state, and that the complexity of the AMT leads to most taxpayers who owe AMT not realizing it until preparing their returns or being notified by the IRS. http://www.irs.gov/pub/irs-utl/arc-exec_summary-2006.pdf

Congress began to distinguish the taxation of capital gains from the taxation of ordinary income according to the holding period of the asset with the Revenue Act of 1921

, allowed a tax rate of 12.5 percent gain for assets held at least two years.

In addition to different tax rates depending on holding period, Congress began excluding certain percentages of capital gains depending on holding period. From 1934 to 1941, taxpayers could exclude percentages of gains that varied with the holding period: 20, 40, 60, and 70 percent of gains were excluded on assets held 1, 2, 5, and 10 years, respectively. Beginning in 1942, taxpayers could exclude 50 percent of capital gains from income on assets held at least six months or elect a 25 percent alternative tax rate if their ordinary tax rate exceeded 50 percent.

Capital gains tax rates were significantly increased in the 1969

and 1976

Tax Reform Acts.

The 1970s and 80s saw a period of oscillating capital gains tax rates. In 1978, Congress reduced capital gains tax rates by eliminating the minimum tax on excluded gains and increasing the exclusion to 60 percent, thereby reducing the maximum rate to 28 percent. The 1981 tax rate reductions further reduced capital gains rates to a maximum of 20 percent.

Later in the 1980s Congress began increasing the capital gains tax rate and repealing the exclusion of capital gains. The Tax Reform Act of 1986

repealed the exclusion from income that provided for tax-exemption of long term capital gains, raising the maximum rate to 28 percent (33 percent for taxpayers subject to phaseouts). When the top ordinary tax rates were increased by the 1990 and 1993 budget acts, an alternative tax rate of 28 percent was provided. Effective tax rates exceeded 28 percent for many high-income taxpayers, however, because of interactions with other tax provisions.

The end of the 1990s and the beginning of the present century heralded major reductions in taxing the income from gains on capital assets. Lower rates for 18-month and five-year assets were adopted in 1997 with the Taxpayer Relief Act of 1997

. In 2001, President George W. Bush

signed the Economic Growth and Tax Relief Reconciliation Act of 2001

, into law as part of a $1.35 trillion tax cut program.

United States

The United States of America is a federal constitutional republic comprising fifty states and a federal district...

began when it was composed of colonies

European colonization of the Americas

The start of the European colonization of the Americas is typically dated to 1492. The first Europeans to reach the Americas were the Vikings during the 11th century, who established several colonies in Greenland and one short-lived settlement in present day Newfoundland...

ruled by the British Empire

British Empire

The British Empire comprised the dominions, colonies, protectorates, mandates and other territories ruled or administered by the United Kingdom. It originated with the overseas colonies and trading posts established by England in the late 16th and early 17th centuries. At its height, it was the...

, French Empire

French colonial empire

The French colonial empire was the set of territories outside Europe that were under French rule primarily from the 17th century to the late 1960s. In the 19th and 20th centuries, the colonial empire of France was the second-largest in the world behind the British Empire. The French colonial empire...

, and Spanish Empire

Spanish Empire

The Spanish Empire comprised territories and colonies administered directly by Spain in Europe, in America, Africa, Asia and Oceania. It originated during the Age of Exploration and was therefore one of the first global empires. At the time of Habsburgs, Spain reached the peak of its world power....

. After independence from Europe

American Revolution

The American Revolution was the political upheaval during the last half of the 18th century in which thirteen colonies in North America joined together to break free from the British Empire, combining to become the United States of America...

the United States collected poll taxes, tariffs

Tariff in American history

Tariffs in United States history have played different roles in trade policy, political debates and the nation's economic history. Tariffs were the largest source of federal revenue from the 1790s to the eve of World War I, until it was surpassed by income taxes. Tariffs are taxes on imports and...

, and excise taxes. The United States imposed income taxes

Income tax in the United States

In the United States, a tax is imposed on income by the Federal, most states, and many local governments. The income tax is determined by applying a tax rate, which may increase as income increases, to taxable income as defined. Individuals and corporations are directly taxable, and estates and...

intermittently until 1895 when unapportioned taxes on interest, dividends and rents were ruled unconstitutional. The advent of the 16th Amendment

Sixteenth Amendment to the United States Constitution

The Sixteenth Amendment to the United States Constitution allows the Congress to levy an income tax without apportioning it among the states or basing it on Census results...

to the United States Constitution

United States Constitution

The Constitution of the United States is the supreme law of the United States of America. It is the framework for the organization of the United States government and for the relationship of the federal government with the states, citizens, and all people within the United States.The first three...

modified the apportionment requirement in 1913, and since then the income tax has become one of the means of funding the Federal Government

Federal government of the United States

The federal government of the United States is the national government of the constitutional republic of fifty states that is the United States of America. The federal government comprises three distinct branches of government: a legislative, an executive and a judiciary. These branches and...

.

Sugar Act

The Sugar Act (citation 4 Geo. III c. 15), passed on April 5, 1764, was a revenue-raising ActRevenue Act

-British Empire:*Revenue Act of 1764, popularly known as the Sugar Act*Revenue Act of 1766*Revenue Act of 1767 , one of the Townshend Acts-United States:* Revenue Act of 1861* Revenue Act of 1862...

passed by the Parliament of Great Britain

Parliament of Great Britain

The Parliament of Great Britain was formed in 1707 following the ratification of the Acts of Union by both the Parliament of England and Parliament of Scotland...

. It revised the earlier Sugar and Molasses Act

Sugar and Molasses Act

The Molasses Act of March 1733 was an Act of the Parliament of Great Britain , which imposed a tax of six pence per gallon on imports of molasses from non-British colonies. Parliament created the act largely at the insistence of large plantation owners in the British West Indies...

, which had imposed a tax of six cents per gallon upon imported molasses in order to make English products cheaper than those from the French West Indies

French West Indies

The term French West Indies or French Antilles refers to the seven territories currently under French sovereignty in the Antilles islands of the Caribbean: the two overseas departments of Guadeloupe and Martinique, the two overseas collectivities of Saint Martin and Saint Barthélemy, plus...

.

Stamp Act

The Stamp Act of 1765 was the fourth Stamp Act to be passed by the Parliament of Great Britain and required all legal documents, permits, commercial contracts, newspapers, wills, pamphlets, and playing cards in the American colonies to carry a tax stamp. The exact date the Act was enacted was on November 1, 1765. The Act was enacted in order to defray the cost of maintaining the military presence protecting the colonies.

Townshend Revenue Act

The Townshend Revenue Act refers to two Acts of the Parliament of Great BritainParliament of Great Britain

The Parliament of Great Britain was formed in 1707 following the ratification of the Acts of Union by both the Parliament of England and Parliament of Scotland...

passed in 1767, which were proposed by Charles Townshend

Charles Townshend

Charles Townshend was a British politician. He was born at his family's seat of Raynham Hall in Norfolk, England, the second son of Charles Townshend, 3rd Viscount Townshend, and Audrey , daughter and heiress of Edward Harrison of Ball's Park, near Hertford, a lady who rivalled her son in...

, Chancellor of the Exchequer

Chancellor of the Exchequer

The Chancellor of the Exchequer is the title held by the British Cabinet minister who is responsible for all economic and financial matters. Often simply called the Chancellor, the office-holder controls HM Treasury and plays a role akin to the posts of Minister of Finance or Secretary of the...

, just before his death. These law

Law

Law is a system of rules and guidelines which are enforced through social institutions to govern behavior, wherever possible. It shapes politics, economics and society in numerous ways and serves as a social mediator of relations between people. Contract law regulates everything from buying a bus...

s placed a tax

Tax

To tax is to impose a financial charge or other levy upon a taxpayer by a state or the functional equivalent of a state such that failure to pay is punishable by law. Taxes are also imposed by many subnational entities...

on common products imported into the American Colonies

Colonial America

The colonial history of the United States covers the history from the start of European settlement and especially the history of the thirteen colonies of Britain until they declared independence in 1776. In the late 16th century, England, France, Spain and the Netherlands launched major...

, such as lead, paper, paint, glass, and tea (though they did not place a tax on silk

Silk

Silk is a natural protein fiber, some forms of which can be woven into textiles. The best-known type of silk is obtained from the cocoons of the larvae of the mulberry silkworm Bombyx mori reared in captivity...

). In contrast to the Stamp Act of 1765

Stamp Act 1765

The Stamp Act 1765 was a direct tax imposed by the British Parliament specifically on the colonies of British America. The act required that many printed materials in the colonies be produced on stamped paper produced in London, carrying an embossed revenue stamp...

, the laws were not a direct tax, but a tax on imports. The Townshend Acts also created three new admiralty court

Admiralty court

Admiralty courts, also known as maritime courts, are courts exercising jurisdiction over all maritime contracts, torts, injuries and offences.- Admiralty Courts in England and Wales :...

s to try Americans who ignored the laws.

Tea Act of 1773

The Tea ActTea Act

The Tea Act was an Act of the Parliament of Great Britain. Its principal overt objective was to reduce the massive surplus of tea held by the financially troubled British East India Company in its London warehouses. A related objective was to undercut the price of tea smuggled into Britain's...

of 1773 was received the royal assent on May 10, 1773. This act was a "drawback on duties and tariffs" on tea. The act was designed to undercut tea smugglers to the benefit of the East India Company

East India Company

The East India Company was an early English joint-stock company that was formed initially for pursuing trade with the East Indies, but that ended up trading mainly with the Indian subcontinent and China...

.

Boston Tea Party

The Boston Tea Party was an act of protest

Protest

A protest is an expression of objection, by words or by actions, to particular events, policies or situations. Protests can take many different forms, from individual statements to mass demonstrations...

by the American colonists against Great Britain

Great Britain

Great Britain or Britain is an island situated to the northwest of Continental Europe. It is the ninth largest island in the world, and the largest European island, as well as the largest of the British Isles...

for the Tea Act

Tea Act

The Tea Act was an Act of the Parliament of Great Britain. Its principal overt objective was to reduce the massive surplus of tea held by the financially troubled British East India Company in its London warehouses. A related objective was to undercut the price of tea smuggled into Britain's...

in which they destroyed many crate

Crate

A crate is a large shipping container, often made of wood, typically used to transport large, heavy or awkward items. A crate has a self-supporting structure, with or without sheathing. For a wooden container to be a crate, all six of its sides must be put in place to result in the rated strength...

s of tea brick

Tea brick

Tea bricks or compressed tea are blocks of whole or finely ground black tea, green tea, or post-fermented tea leaves that have been packed in molds and pressed into block form...

s on ships in Boston Harbor

Boston Harbor

Boston Harbor is a natural harbor and estuary of Massachusetts Bay, and is located adjacent to the city of Boston, Massachusetts. It is home to the Port of Boston, a major shipping facility in the northeast.-History:...

. The incident, which took place on Thursday, December 16, 1773, has been seen as helping to spark the American Revolution

American Revolution

The American Revolution was the political upheaval during the last half of the 18th century in which thirteen colonies in North America joined together to break free from the British Empire, combining to become the United States of America...

.

Capitation tax

- Main Articles: Poll TaxPoll taxA poll tax is a tax of a portioned, fixed amount per individual in accordance with the census . When a corvée is commuted for cash payment, in effect it becomes a poll tax...

, Shays' RebellionShays' RebellionShays' Rebellion was an armed uprising in central and western Massachusetts from 1786 to 1787. The rebellion is named after Daniel Shays, a veteran of the American Revolutionary War....

Income for federal government

Tariffs have played different roles in trade policy and the economic history of the United StatesEconomic history of the United States

The economic history of the United States has its roots in European colonization in the 16th, 17th, and 18th centuries. Marginal colonial economies grew into 13 small, independent farming economies, which joined together in 1776 to form the United States of America...

. Tariffs were the largest source of federal revenue from the 1790s to the eve of World War I

World War I

World War I , which was predominantly called the World War or the Great War from its occurrence until 1939, and the First World War or World War I thereafter, was a major war centred in Europe that began on 28 July 1914 and lasted until 11 November 1918...

, until it was surpassed by income taxes. Since the revenue from the tariff was considered essential and easy to collect at the major port

Port

A port is a location on a coast or shore containing one or more harbors where ships can dock and transfer people or cargo to or from land....

s, it was agreed the nation should have a tariff for revenue purposes.

Protectionism

Another role the tariff played was in the protection of local industryProtectionism

Protectionism is the economic policy of restraining trade between states through methods such as tariffs on imported goods, restrictive quotas, and a variety of other government regulations designed to allow "fair competition" between imports and goods and services produced domestically.This...

; it was the political dimension of the tariff. From the 1790s to the 2000s, the tariff (and closely related issues such as import quotas and trade

Trade

Trade is the transfer of ownership of goods and services from one person or entity to another. Trade is sometimes loosely called commerce or financial transaction or barter. A network that allows trade is called a market. The original form of trade was barter, the direct exchange of goods and...

treaties) generated enormous political stresses whether during the 19th century with the Nullification crisis

Nullification Crisis

The Nullification Crisis was a sectional crisis during the presidency of Andrew Jackson created by South Carolina's 1832 Ordinance of Nullification. This ordinance declared by the power of the State that the federal Tariff of 1828 and 1832 were unconstitutional and therefore null and void within...

or the WTO.

Origins of protectionism

When Alexander HamiltonAlexander Hamilton

Alexander Hamilton was a Founding Father, soldier, economist, political philosopher, one of America's first constitutional lawyers and the first United States Secretary of the Treasury...

was the United States Secretary of the Treasury

United States Secretary of the Treasury

The Secretary of the Treasury of the United States is the head of the United States Department of the Treasury, which is concerned with financial and monetary matters, and, until 2003, also with some issues of national security and defense. This position in the Federal Government of the United...

he issued the Report on Manufactures

Report on Manufactures

The Report on Manufactures is the third report, and magnum opus, of American Founding Father and 1st U.S. Treasury Secretary Alexander Hamilton...

, which reasoned that applying tariffs in moderation, in addition to raising revenue to fund the federal government, would also encourage domestic manufacturing and growth of the economy by applying the funds raised in part towards subsidies (called bounties in his time) to manufacturers. The main purposes sought by Hamilton through the tariff were to: (1) protect American infant industry for a short term until it could compete; (2) raise revenue to pay the expenses of government; (3) raise revenue to directly support manufacturing through bounties (subsidies). This resulted in the passage of three tariffs by Congress, the Tariff of 1789, the Tariff of 1790

Tariff of 1790

In 1790, Alexander Hamilton, the secretary of the treasury, calculated that the United States required $3 million a year for operating expenses as well as enough revenue to repay the estimated $75 million in foreign and domestic debt. Under the rates established by the Tariff of 1789, the...

, and the Tariff of 1792

Tariff of 1792

The Tariff of 1792 was the third of Alexander Hamilton's protective tariffs in the United States . Hamilton had persuaded the United States Congress to raise duties slightly in 1790, and he persuaded them to raise rates again in 1792, although still not to his satisfaction...

which progressively increased tariffs.

Sectionalism

Tariffs contributed to sectionalism between the North and the South. The Tariff of 1824Tariff of 1824

The Tariff of 1824 , was a protective tariff in the United States designed to protect American industry in the face of cheaper British commodities, especially iron products, wool and cotton textiles, and agricultural goods...

increased tariffs in order to protect American industry in the face of cheaper imported commodities such as iron products, wool and cotton textiles, and agricultural goods from England. This tariff was the first in which the sectional interests of the North and the South truly came into conflict because the South advocated lower tariffs in order to take advantage of tariff reciprocity from England and other countries that purchased raw agricultural materials from the South.

The Tariff of 1828

Tariff of 1828

The Tariff of 1828 was a protective tariff passed by the Congress of the United States on May 19, 1828, designed to protect industry in the northern United States...

, also known as the Tariff of Abominations, and the Tariff of 1832

Tariff of 1832

The Tariff of 1832 was a protectionist tariff in the United States. It was largely written by former President John Quincy Adams, who had been elected to the House of Representatives and been made chairman of the Committee on Manufactures, and reduced tariffs to remedy the conflict created by the...

accelerated sectionalism between the North and the South. For a brief moment in 1832, South Carolina made vague threats to leave the Union over the tariff issue. In 1833, to ease North-South relations, Congress lowered the tariffs. In the 1850s, the South gained greater influence over tariff policy and made subsequent reductions.

In 1861, just prior to the Civil War, Congress enacted the Morrill Tariff

Morrill Tariff

The Morrill Tariff of 1861 was a protective tariff in the United States, adopted on March 2, 1861 during the administration of President James Buchanan....

, which applied high rates and inaugurated a period of relatively continuous trade protection in the United States that lasted until the Underwood Tariff of 1913. The schedule of the Morrill Tariff and its two successor bills were retained long after the end of the Civil War.

Early 20th century protectionism

In 1921, Congress sought to protect local agriculture as opposed to industry by passing the Emergency TariffEmergency Tariff of 1921

The Emergency Tariff of 1921 of the United States was enacted on May 27, 1921. Due to the Underwood Tariff passed during the Wilson Administration, Republican leaders in the United States Congress rushed to create a temporary measure to ease the plight of farmers until a better solution could be...

, which increased rates on wheat

Wheat

Wheat is a cereal grain, originally from the Levant region of the Near East, but now cultivated worldwide. In 2007 world production of wheat was 607 million tons, making it the third most-produced cereal after maize and rice...

, sugar

Sugar

Sugar is a class of edible crystalline carbohydrates, mainly sucrose, lactose, and fructose, characterized by a sweet flavor.Sucrose in its refined form primarily comes from sugar cane and sugar beet...

, meat

Meat

Meat is animal flesh that is used as food. Most often, this means the skeletal muscle and associated fat and other tissues, but it may also describe other edible tissues such as organs and offal...

, wool

Wool

Wool is the textile fiber obtained from sheep and certain other animals, including cashmere from goats, mohair from goats, qiviut from muskoxen, vicuña, alpaca, camel from animals in the camel family, and angora from rabbits....

and other agricultural products brought into the United States

United States

The United States of America is a federal constitutional republic comprising fifty states and a federal district...

from foreign nations, which provided protection for domestic producers of those items.

However, one year later Congress passed another tariff, the Fordney-McCumber Tariff

Fordney-McCumber Tariff

The Fordney–McCumber Tariff of 1922 raised American tariffs in order to protect factories and farms. Congress displayed a pro-business attitude in passing the ad valorem tariff and in promoting foreign trade through providing huge loans to Europe, which in turn bought more American goods...

, which applied the scientific tariff and the American Selling Price. The purpose of the scientific tariff was to equalize production costs among countries so that no country could undercut the prices charged by American companies. The difference of production costs was calculated by the Tariff Commission. A second novelty was the American Selling Price. This allowed the president to calculate the duty based on the price of the American price of a good, not the imported good.

During the outbreak of the Great Depression in 1930, Congress raised tariffs on over 20,000 imported goods to record levels, and, in the opinion of most economists, worsened the Great Depression by causing other countries to reciprocate thereby plunging American imports and exports by more than half.

Era of GATT and WTO

In 1948, the US signed the General Agreement on Tariffs and TradeGeneral Agreement on Tariffs and Trade

The General Agreement on Tariffs and Trade was negotiated during the UN Conference on Trade and Employment and was the outcome of the failure of negotiating governments to create the International Trade Organization . GATT was signed in 1947 and lasted until 1993, when it was replaced by the World...

(GATT), which reduced tariff barriers and other quantitative restrictions and subsidies on trade through a series of agreements.

In 1993 the GATT was updated (GATT 1994) to include new obligations upon its signatories. One of the most significant changes was the creation of the World Trade Organization

World Trade Organization

The World Trade Organization is an organization that intends to supervise and liberalize international trade. The organization officially commenced on January 1, 1995 under the Marrakech Agreement, replacing the General Agreement on Tariffs and Trade , which commenced in 1948...

(WTO). Whereas GATT was a set of rules agreed upon by nations, the WTO is an institutional body. The WTO expanded its scope from traded goods to trade within the service sector and intellectual property rights. Although it was designed to serve multilateral agreements, during several rounds of GATT negotiations (particularly the Tokyo

Tokyo

, ; officially , is one of the 47 prefectures of Japan. Tokyo is the capital of Japan, the center of the Greater Tokyo Area, and the largest metropolitan area of Japan. It is the seat of the Japanese government and the Imperial Palace, and the home of the Japanese Imperial Family...

Round) plurilateral agreements created selective trading and caused fragmentation among members. WTO arrangements are generally a multilateral agreement settlement mechanism of GATT.

Excise tax

- Main articles: Excise tax in the United States, Whisky Rebellion

Federal excise taxes are applied to specific items such as motor fuels, tires, telephone usage, tobacco products, and alcoholic beverages. Excise taxes are often, but not always, allocated to special funds related to the object or activity taxed.

Income tax

The history of income taxation in the United States began in the 19th century with the imposition of income taxes to fund war efforts. However, the constitutionality of income taxation was widely held in doubt until 1913 with the ratification of the 16th Amendment.Legal foundations

Article I, Section 8, Clause 1 of the United States Constitution assigns CongressUnited States Congress

The United States Congress is the bicameral legislature of the federal government of the United States, consisting of the Senate and the House of Representatives. The Congress meets in the United States Capitol in Washington, D.C....

the power to impose "Taxes, Duties, Imposts and Excises," but Article I, Section 8 requires that, "Duties, Imposts and Excises shall be uniform throughout the United States."

In addition, the Constitution specifically limited Congress' ability to impose direct taxes, by requiring it to distribute direct taxes in proportion to each state's census population. It was thought that head taxes and property tax

Property tax

A property tax is an ad valorem levy on the value of property that the owner is required to pay. The tax is levied by the governing authority of the jurisdiction in which the property is located; it may be paid to a national government, a federated state or a municipality...

es (slaves could be taxed as either or both) were likely to be abused, and that they bore no relation to the activities in which the federal government had a legitimate interest. The fourth clause of section 9 therefore specifies that, "No Capitation, or other direct, Tax shall be laid, unless in Proportion to the Census or enumeration herein before directed to be taken."

Taxation was also the subject of Federalist No. 33

Federalist No. 33

Federalist No. 33 is an essay by Alexander Hamilton, the thirty-third of the Federalist Papers. It was published on January 2, 1788 under the pseudonym Publius, the name under which all the Federalist Papers were published. This is the fourth of seven essays by Hamilton on the then-controversial...

penned secretly by the Federalist Alexander Hamilton

Alexander Hamilton

Alexander Hamilton was a Founding Father, soldier, economist, political philosopher, one of America's first constitutional lawyers and the first United States Secretary of the Treasury...

under the pseudonym

Pseudonym

A pseudonym is a name that a person assumes for a particular purpose and that differs from his or her original orthonym...

Publius. In it, he explains that the wording of the "Necessary and Proper" clause should serve as guidelines for the legislation of laws regarding taxation. The legislative branch is to be the judge, but any abuse of those powers of judging can be overturned by the people, whether as states or as a larger group.

What seemed to be a straightforward limitation on the power of the legislature based on the subject of the tax proved inexact and unclear when applied to an income tax, which can be arguably viewed either as a direct or an indirect tax. The courts have generally held that direct taxes are limited to taxes on people (variously called "capitation", "poll tax" or "head tax") and property. All other taxes are commonly referred to as "indirect taxes," because they tax an event, rather than a person or property per se.

Pre-16th Amendment

In order to help pay for its war effort in the American Civil WarAmerican Civil War

The American Civil War was a civil war fought in the United States of America. In response to the election of Abraham Lincoln as President of the United States, 11 southern slave states declared their secession from the United States and formed the Confederate States of America ; the other 25...

, Congress imposed its first personal income tax in 1861. It was part of the Revenue Act of 1861

Revenue Act of 1861

The Revenue Act of 1861, formally cited as , included the first U.S. Federal income tax statute . The Act, motivated by the need to fund the Civil War , imposed an income tax to be "levied, collected, and paid, upon the annual income of every person residing in the United States, whether such...

(3% of all incomes over US $800; rescinded in 1872). Congress also enacted the Revenue Act of 1862

Revenue Act of 1862

The Revenue Act of 1862 , was passed by the United States Congress to help fund the American Civil War. The Act was signed into law by President Abraham Lincoln, introducing the first progressive rate income tax to the country....

, which levied a 3% tax on incomes above $600, rising to 5% for incomes above $10,000. Rates were raised in 1864. This income tax was repealed in 1872.

A new income tax statute was enacted as part of the 1894 Tariff Act. At that time, the United States Constitution

United States Constitution

The Constitution of the United States is the supreme law of the United States of America. It is the framework for the organization of the United States government and for the relationship of the federal government with the states, citizens, and all people within the United States.The first three...

specified that Congress could impose a "direct" tax only if the law apportioned that tax among the states according to each state's census

United States Census

The United States Census is a decennial census mandated by the United States Constitution. The population is enumerated every 10 years and the results are used to allocate Congressional seats , electoral votes, and government program funding. The United States Census Bureau The United States Census...

population.

In 1895, the United States Supreme Court ruled, in Pollock v. Farmers' Loan & Trust Co.

Pollock v. Farmers' Loan & Trust Co.

Pollock v. Farmers' Loan & Trust Company, , aff'd on reh'g, , with a ruling of 5–4, was a landmark case in which the Supreme Court of the United States ruled that the unapportioned income taxes on interest, dividends and rents imposed by the Income Tax Act of 1894 were, in effect, direct taxes, and...

, that taxes on rent

Economic rent

Economic rent is typically defined by economists as payment for goods and services beyond the amount needed to bring the required factors of production into a production process and sustain supply. A recipient of economic rent is a rentier....

s from real estate, on interest

Interest

Interest is a fee paid by a borrower of assets to the owner as a form of compensation for the use of the assets. It is most commonly the price paid for the use of borrowed money, or money earned by deposited funds....

income from personal property and other income from personal property (which includes dividend

Dividend

Dividends are payments made by a corporation to its shareholder members. It is the portion of corporate profits paid out to stockholders. When a corporation earns a profit or surplus, that money can be put to two uses: it can either be re-invested in the business , or it can be distributed to...

income) were direct taxes on property and therefore had to be apportioned. Since apportionment of income taxes is impractical, the Pollock rulings had the effect of prohibiting a federal tax on income from property. Due to the political difficulties of taxing individual wages without taxing income from property, a federal income tax was impractical from the time of the Pollock decision until the time of ratification of the Sixteenth Amendment (below).

16th Amendment

Sixteenth Amendment to the United States Constitution

The Sixteenth Amendment to the United States Constitution allows the Congress to levy an income tax without apportioning it among the states or basing it on Census results...

, which was ratified in 1913, and which states:

The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.

The Supreme Court

Supreme Court of the United States

The Supreme Court of the United States is the highest court in the United States. It has ultimate appellate jurisdiction over all state and federal courts, and original jurisdiction over a small range of cases...

in Brushaber v. Union Pacific Railroad

Brushaber v. Union Pacific Railroad

Brushaber v. Union Pacific Railroad, 240 U.S. 1 , was a landmark United States Supreme Court case in which the Court upheld the validity of a tax statute called the Revenue Act of 1913, also known as the Tariff Act, Ch. 16, 38 Stat. 166 Brushaber v. Union Pacific Railroad, 240 U.S. 1 (1916), was a...

, , indicated that the Sixteenth Amendment did not expand the federal government's existing power to tax income (meaning profit or gain from any source) but rather removed the possibility of classifying an income tax as a direct tax on the basis of the source of the income. The Amendment removed the need for the income tax on interest, dividends and rents to be apportioned among the states on the basis of population. Income taxes are required, however, to abide by the law of geographical uniformity.

Congress enacted an income tax in October 1913 as part of the Revenue Act of 1913

Revenue Act of 1913

The United States Revenue Act of 1913 also known as the Tariff Act, Underwood Tariff, Underwood Tariff Act, or Underwood-Simmons Act , re-imposed the federal income tax following the ratification of the Sixteenth Amendment and lowered basic tariff rates from 40% to 25%, well below the Payne-Aldrich...

, levying a 1% tax on net personal incomes above $3,000, with a 6% surtax on incomes above $500,000. By 1918, the top rate of the income tax was increased to 77% (on income over $1,000,000) to finance World War I

World War I

World War I , which was predominantly called the World War or the Great War from its occurrence until 1939, and the First World War or World War I thereafter, was a major war centred in Europe that began on 28 July 1914 and lasted until 11 November 1918...

. The top marginal tax rate was reduced to 58% in 1922, to 25% in 1925 and finally to 24% in 1929. In 1932 the top marginal tax rate was increased to 63% during the Great Depression

Great Depression

The Great Depression was a severe worldwide economic depression in the decade preceding World War II. The timing of the Great Depression varied across nations, but in most countries it started in about 1929 and lasted until the late 1930s or early 1940s...

and steadily increased, reaching 94% (on all income over $200,000) in 1945. During World War II, Congress introduced payroll withholding and quarterly tax payments.

Top marginal tax rates stayed near or above 90% until 1964 when the top marginal tax rate was lowered to 70%. The top marginal tax rate was lowered to 50% in 1982 and eventually to 28% in 1988. It slowly increased to 39.6% in 2000, then was reduced to 35% for the period 2003 through 2010.

Development of the modern income tax

Congress re-adopted the income tax in 1916, levying a 1% tax on net personal incomes above $3,000, with a 6% surtaxSurtax

A surtax may be a tax levied upon a tax, or a tax levied upon income.-United Kingdom:In 1929, Supertax was renamed Sur-tax...

on incomes above $500,000. By 1918, the top rate of the income tax was increased to 77% (on income over $1,000,000) to finance World War I

World War I

World War I , which was predominantly called the World War or the Great War from its occurrence until 1939, and the First World War or World War I thereafter, was a major war centred in Europe that began on 28 July 1914 and lasted until 11 November 1918...

. The top marginal tax rate was reduced to 58% in 1922, to 25% in 1925, and finally to 24% in 1929. In 1932 the top marginal tax rate was increased to 63% during the Great Depression

Great Depression

The Great Depression was a severe worldwide economic depression in the decade preceding World War II. The timing of the Great Depression varied across nations, but in most countries it started in about 1929 and lasted until the late 1930s or early 1940s...

and steadily increased.

During World War II, Congress introduced payroll withholding and quarterly tax payments, Franklin D. Roosevelt

Franklin D. Roosevelt

Franklin Delano Roosevelt , also known by his initials, FDR, was the 32nd President of the United States and a central figure in world events during the mid-20th century, leading the United States during a time of worldwide economic crisis and world war...

tried to impose a 100% tax on all incomes over $25,000 to help with the war effort. For tax years 1944 through 1951, the highest marginal tax rate for individuals was 91%, increasing to 92% for 1952 and 1953, and reverting to 91% for tax years 1954 through 1963.

For the 1964 tax year, the top marginal tax rate for individuals was lowered to 77%, and then to 70% for tax years 1965 through 1981. The top marginal tax rate was lowered to 50% for tax years 1982 through 1986.

For tax year 1987, the highest marginal tax rate was 38.5% for individuals. It was lowered to 28%, eliminating many loopholes and shelters, (with a 33% "bubble rate") for tax years 1988 through 1990.

For the 1991 and 1992 tax years, the top marginal rate was increased to 31% in a budget deal President George H. W. Bush

George H. W. Bush

George Herbert Walker Bush is an American politician who served as the 41st President of the United States . He had previously served as the 43rd Vice President of the United States , a congressman, an ambassador, and Director of Central Intelligence.Bush was born in Milton, Massachusetts, to...

made with the Congress.

In 1993 the Clinton

Bill Clinton

William Jefferson "Bill" Clinton is an American politician who served as the 42nd President of the United States from 1993 to 2001. Inaugurated at age 46, he was the third-youngest president. He took office at the end of the Cold War, and was the first president of the baby boomer generation...

administration proposed and the Congress accepted (with no Republican support) an increase in the top marginal rate to 39.6% for the 1993 tax year, where it remained through tax year 2000.

In 2001, President George W. Bush

George W. Bush

George Walker Bush is an American politician who served as the 43rd President of the United States, from 2001 to 2009. Before that, he was the 46th Governor of Texas, having served from 1995 to 2000....

proposed and the Congress accepted an eventual lowering of the top marginal rate to 35%. However, this was done in stages: with a highest marginal rate of 39.1% for 2001, then 38.6% for 2002 and finally 35% for years 2003 through 2010. This measure had a sunset provision and was scheduled to expire for the 2011 tax year, when rates would have returned to those adopted during the Clinton years unless Congress changed the law; Congress did so by passing the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010, signed by President Barack Obama on December 17, 2010.

At first the income tax was incrementally expanded by the Congress of the United States, and then inflation automatically raised most persons into tax bracket

Tax bracket

Tax brackets are the divisions at which tax rates change in a progressive tax system . Essentially, they are the cutoff values for taxable income — income past a certain point will be taxed at a higher rate.-Example:Imagine that there are three tax brackets: 10%, 20%, and 30%...

s formerly reserved for the wealthy until income tax brackets were adjusted for inflation. Income tax now applies to almost two-thirds of the population. The lowest earning workers, especially those with dependents, pay no income taxes as a group and actually get a small subsidy from the federal government because of child credits and the Earned Income Tax Credit

Earned income tax credit

The United States federal earned income tax credit or earned income credit is a refundable tax credit primarily for individuals and families who have low to moderate earned income. Greater tax credit is given to those who also have qualifying children...

.

While the government was originally funded via tariff

Tariff

A tariff may be either tax on imports or exports , or a list or schedule of prices for such things as rail service, bus routes, and electrical usage ....

s upon imported goods, tariffs now represent only a minor portion of federal revenues. Non-tax fees are generated to recompense agencies for services or to fill specific trust funds such as the fee placed upon airline ticket

Airline ticket

An airline ticket is a document, issued by an airline or a travel agency, to confirm that an individual has purchased a seat on a flight on an aircraft. This document is then used to obtain a boarding pass, at the airport...

s for airport expansion and air traffic control

Air traffic control

Air traffic control is a service provided by ground-based controllers who direct aircraft on the ground and in the air. The primary purpose of ATC systems worldwide is to separate aircraft to prevent collisions, to organize and expedite the flow of traffic, and to provide information and other...

. Often the receipts intended to be placed in "trust" funds are used for other purposes, with the government posting an IOU

IOU (debt)

An IOU is usually an informal document acknowledging debt. An IOU differs from a promissory note in that an IOU is not a negotiable instrument and does not specify repayment terms such as the time of repayment. IOUs usually specify the debtor, the amount owed, and sometimes the creditor...

('I owe you') in the form of a federal bond or other accounting instrument, then spending the money on unrelated current expenditures.

Net long-term capital gain

Capital gain

A capital gain is a profit that results from investments into a capital asset, such as stocks, bonds or real estate, which exceeds the purchase price. It is the difference between a higher selling price and a lower purchase price, resulting in a financial gain for the investor...

s as well as certain types of qualified dividend

Qualified dividend

Qualified dividends, as defined by the United States Internal Revenue Code, are ordinary dividends that meet specific criteria to be taxed at the lower long-term capital gains tax rate rather than at higher tax rate for an individual's ordinary income...

income are taxed preferentially. The federal government collects several specific taxes in addition to the general income tax. Social Security

Social Security (United States)

In the United States, Social Security refers to the federal Old-Age, Survivors, and Disability Insurance program.The original Social Security Act and the current version of the Act, as amended encompass several social welfare and social insurance programs...

and Medicare

Medicare (United States)

Medicare is a social insurance program administered by the United States government, providing health insurance coverage to people who are aged 65 and over; to those who are under 65 and are permanently physically disabled or who have a congenital physical disability; or to those who meet other...

are large social support programs which are funded by taxes on personal earned income (see below).

Treatment of "income"

Tax statutes passed after the ratification of the Sixteenth Amendment in 1913 are sometimes referred to as the "modern" tax statutes. Hundreds of Congressional acts have been passed since 1913, as well as several codifications (i.e., topical reorganizations) of the statutes (see Codification).The modern interpretation of the Sixteenth Amendment taxation power can be found in Commissioner v. Glenshaw Glass Co.

Commissioner v. Glenshaw Glass Co.

Commissioner v. Glenshaw Glass Co., , was an important income tax case before the United States Supreme Court. The Court held as follows:...

. In that case, a taxpayer had received an award of punitive damages from a competitor, and sought to avoid paying taxes on that award. The Court observed that Congress, in imposing the income tax, had defined income to include:

gains, profits, and income derived from salaries, wages, or compensation for personal service . . . of whatever kind and in whatever form paid, or from professions, vocations, trades, businesses, commerce, or sales, or dealings in property, whether real or personal, growing out of the ownership or use of or interest in such property; also from interest, rent, dividends, securities, or the transaction of any business carried on for gain or profit, or gains or profits and income derived from any source whatever.

The Court held that "this language was used by Congress to exert in this field the full measure of its taxing power", id., and that "the Court has given a liberal construction to this broad phraseology in recognition of the intention of Congress to tax all gains except those specifically exempted."

The Court then enunciated what is now understood by Congress and the Courts to be the definition of taxable income, "instances of undeniable accessions to wealth, clearly realized, and over which the taxpayers have complete dominion." Id. at 431. The defendant in that case suggested that a 1954 rewording of the tax code had limited the income that could be taxed, a position which the Court rejected, stating:

The definition of gross income has been simplified, but no effect upon its present broad scope was intended. Certainly punitive damages cannot reasonably be classified as gifts, nor do they come under any other exemption provision in the Code. We would do violence to the plain meaning of the statute and restrict a clear legislative attempt to bring the taxing power to bear upon all receipts constitutionally taxable were we to say that the payments in question here are not gross income.

In Conner v. United States, a couple had lost their home to a fire, and had received compensation for their loss from the insurance company, partly in the form of hotel costs reimbursed. The court acknowledged the authority of the IRS to assess taxes on all forms of payment, but did not permit taxation on the compensation provided by the insurance company, because unlike a wage or a sale of goods at a profit, this was not a gain. As the court noted, "Congress has taxed income, not compensation". By contrast, at least two other Federal courts have indicated that Congress may constitutionally tax an item as "income," regardless of whether that item is in fact income. See Penn Mutual Indemnity Co. v. Commissioner and Murphy v. Internal Revenue Serv.

Murphy v. IRS

Marrita Murphy and Daniel J. Leveille, Appellants v. Internal Revenue Service and United States of America, Appellees , is a controversial tax case in which the United States Court of Appeals for the District of Columbia Circuit originally held that the taxation of emotional distress awards by the...

Estate & Gift Tax

- Main articles: Estate tax in the United StatesEstate tax in the United StatesThe estate tax in the United States is a tax imposed on the transfer of the "taxable estate" of a deceased person, whether such property is transferred via a will, according to the state laws of intestacy or otherwise made as an incident of the death of the owner, such as a transfer of property...

, Gift tax in the United States

The origins of the estate and gift tax occurred during the rise of the state inheritance tax in the late 19th century and the progressive era

Progressive Era

The Progressive Era in the United States was a period of social activism and political reform that flourished from the 1890s to the 1920s. One main goal of the Progressive movement was purification of government, as Progressives tried to eliminate corruption by exposing and undercutting political...

.

In the 1880s and 1890s many states passed inheritance taxes, which taxed the donees on the receipt of their inheritance. While many objected to the application of an inheritance tax, some including Andrew Carnegie

Andrew Carnegie

Andrew Carnegie was a Scottish-American industrialist, businessman, and entrepreneur who led the enormous expansion of the American steel industry in the late 19th century...

and John D. Rockefeller

John D. Rockefeller

John Davison Rockefeller was an American oil industrialist, investor, and philanthropist. He was the founder of the Standard Oil Company, which dominated the oil industry and was the first great U.S. business trust. Rockefeller revolutionized the petroleum industry and defined the structure of...

supported increases in the taxation of inheritance.

At the beginning of the 20th century President Theodore Roosevelt

Theodore Roosevelt

Theodore "Teddy" Roosevelt was the 26th President of the United States . He is noted for his exuberant personality, range of interests and achievements, and his leadership of the Progressive Movement, as well as his "cowboy" persona and robust masculinity...

advocated the application of a progressive inheritance tax on the federal level.

In 1916, Congress adopted the present federal estate tax, which instead of taxing the wealth that a donee inherited as occurred in the state inheritance taxes it taxed the wealth of a donor's estate upon transfer.

Later, Congress passed the Revenue Act of 1924

Revenue Act of 1924

The United States Revenue Act of 1924 , also known as the Mellon tax bill cut federal tax rates and established the U.S. Board of Tax Appeals, which was later renamed the United States Tax Court in 1942. The bill was named after U.S...

, which imposed the gift tax, a tax on gifts given by the donor.

In 1948 Congress allowed marital deductions for the estate and the gift tax. In 1981, Congress expanded this deduction to an unlimited amount for gifts between spouses.

Today, the estate tax is a tax imposed on the transfer of the "taxable estate

Estate (law)

An estate is the net worth of a person at any point in time. It is the sum of a person's assets - legal rights, interests and entitlements to property of any kind - less all liabilities at that time. The issue is of special legal significance on a question of bankruptcy and death of the person...

" of a deceased person, whether such property is transferred via a will

Will (law)

A will or testament is a legal declaration by which a person, the testator, names one or more persons to manage his/her estate and provides for the transfer of his/her property at death...

or according to the state laws of intestacy

Intestacy

Intestacy is the condition of the estate of a person who dies owning property greater than the sum of their enforceable debts and funeral expenses without having made a valid will or other binding declaration; alternatively where such a will or declaration has been made, but only applies to part of...

. The estate tax is one part of the Unified Gift and Estate Tax system in the United States. The other part of the system, the gift tax, imposes a tax on transfers of property during a person's life; the gift tax prevents avoidance of the estate tax should a person want to give away his/her estate just before dying.

In addition to the federal government, many states also impose an estate tax, with the state version called either an estate tax or an inheritance tax

Inheritance tax

An inheritance tax or estate tax is a levy paid by a person who inherits money or property or a tax on the estate of a person who has died...

. Since the 1990s, the term "death tax" has been widely used by those who want to eliminate the estate tax, because the terminology used in discussing a political issue affects popular opinion.

If an asset is left to a spouse or a charitable organization, the tax usually does not apply. The tax is imposed on other transfers of property made as an incident of the death of the owner, such as a transfer of property from an intestate estate or trust, or the payment of certain life insurance