Modern portfolio theory

Encyclopedia

Modern portfolio theory (MPT) is a theory of investment

which attempts to maximize portfolio expected return

for a given amount of portfolio risk, or equivalently minimize risk

for a given level of expected return, by carefully choosing the proportions of various asset

s. Although MPT is widely used in practice in the financial industry and several of its creators won a Nobel memorial prize

for the theory, in recent years the basic assumptions of MPT have been widely challenged by fields such as behavioral economics.

MPT is a mathematical formulation of the concept of diversification

in investing, with the aim of selecting a collection of investment assets that has collectively lower risk than any individual asset. That this is possible can be seen intuitively because different types of assets often change in value in opposite ways. For example, to the extent prices in the stock market

move differently from prices in the bond market

, a collection of both types of assets can in theory face lower overall risk than either individually. But diversification lowers risk even if assets' returns are not negatively correlated—indeed, even if they are positively correlated.

More technically, MPT models an asset's return as a normally distributed function (or more generally as an elliptically distributed

random variable

), defines risk

as the standard deviation

of return, and models a portfolio as a weighted combination of assets, so that the return of a portfolio is the weighted combination of the assets' returns. By combining different assets whose returns are not perfectly positively correlated, MPT seeks to reduce the total variance

of the portfolio return. MPT also assumes that investors are rational

and markets are efficient

.

MPT was developed in the 1950s through the early 1970s and was considered an important advance in the mathematical modeling of finance. Since then, many theoretical and practical criticisms have been leveled against it. These include the fact that financial returns do not follow a Gaussian distribution or indeed any symmetric distribution, and that correlations between asset classes are not fixed but can vary depending on external events (especially in crises). Further, there is growing evidence that investors are not rational and markets are not efficient

.

s in an investment portfolio

should not be selected individually, each on their own merits. Rather, it is important to consider how each asset changes in price relative to how every other asset in the portfolio changes in price.

Investing is a tradeoff between risk

and expected return. In general, assets with higher expected returns are riskier. For a given amount of risk, MPT describes how to select a portfolio with the highest possible expected return. Or, for a given expected return, MPT explains how to select a portfolio with the lowest possible risk (the targeted expected return cannot be more than the highest-returning available security, of course, unless negative holdings of assets are possible.)

Therefore, MPT is a form of diversification

. Under certain assumptions and for specific quantitative

definitions of risk and return, MPT explains how to find the best possible diversification strategy.

introduced MPT in a 1952 article and a 1959 book. Markowitz classifies it simply as "Portfolio Theory," because "There's nothing modern about it." See also this survey of the history.

The portfolio management is combination security and risk, due to markowitz approach investor can analyse the varies security and risk which gave highest return and minimum risk.

This section develops the "classic" MPT model. There have been many extensions since.

investor will not invest in a portfolio if a second portfolio exists with a more favorable risk-expected return profile

– i.e., if for that level of risk an alternative portfolio exists which has better expected returns.

Note that the theory uses standard deviation of return as a proxy for risk, which is valid if asset returns are jointly normally distributed or otherwise elliptically distributed

. There are problems with this, however; see criticism.

Under the model:

(correlation coefficient

). In other words, investors can reduce their exposure to individual asset risk by holding a diversified

). In other words, investors can reduce their exposure to individual asset risk by holding a diversified

portfolio of assets. Diversification may allow for the same portfolio expected return with reduced risk.

If all the asset pairs have correlations of 0—they are perfectly uncorrelated—the portfolio's return variance is the sum over all assets of the square of the fraction held in the asset times the asset's return variance (and the portfolio standard deviation is the square root of this sum).

As shown in this graph, every possible combination of the risky assets, without including any holdings of the risk-free asset, can be plotted in risk-expected return space, and the collection of all such possible portfolios defines a region in this space. The left boundary of this region is a hyperbola, and the upper edge of this region is the efficient frontier in the absence of a risk-free asset (sometimes called "the Markowitz bullet"). Combinations along this upper edge represent portfolios (including no holdings of the risk-free asset) for which there is lowest risk for a given level of expected return. Equivalently, a portfolio lying on the efficient frontier represents the combination offering the best possible expected return for given risk level.

As shown in this graph, every possible combination of the risky assets, without including any holdings of the risk-free asset, can be plotted in risk-expected return space, and the collection of all such possible portfolios defines a region in this space. The left boundary of this region is a hyperbola, and the upper edge of this region is the efficient frontier in the absence of a risk-free asset (sometimes called "the Markowitz bullet"). Combinations along this upper edge represent portfolios (including no holdings of the risk-free asset) for which there is lowest risk for a given level of expected return. Equivalently, a portfolio lying on the efficient frontier represents the combination offering the best possible expected return for given risk level.

risk. The risk-free asset has zero variance in returns (hence is risk-free); it is also uncorrelated with any other asset (by definition, since its variance is zero). As a result, when it is combined with any other asset or portfolio of assets, the change in return is linearly related to the change in risk as the proportions in the combination vary.

When a risk-free asset is introduced, the half-line shown in the figure is the new efficient frontier. It is tangent to the hyperbola at the pure risky portfolio with the highest Sharpe ratio

. Its horizontal intercept represents a portfolio with 100% of holdings in the risk-free asset; the tangency with the hyperbola represents a portfolio with no risk-free holdings and 100% of assets held in the portfolio occurring at the tangency point; points between those points are portfolios containing positive amounts of both the risky tangency portfolio and the risk-free asset; and points on the half-line beyond the tangency point are leverage

d portfolios involving negative holdings of the risk-free asset (the latter has been sold short—in other words, the investor has borrowed at the risk-free rate) and an amount invested in the tangency portfolio equal to more than 100% of the investor's initial capital. This efficient half-line is called the capital allocation line

(CAL), and its formula can be shown to be

In this formula P is the sub-portfolio of risky assets at the tangency with the Markowitz bullet, F is the risk-free asset, and C is a combination of portfolios P and F.

By the diagram, the introduction of the risk-free asset as a possible component of the portfolio has improved the range of risk-expected return combinations available, because everywhere except at the tangency portfolio the half-line gives a higher expected return than the hyperbola does at every possible risk level. The fact that all points on the linear efficient locus can be achieved by a combination of holdings of the risk-free asset and the tangency portfolio is known as the one mutual fund theorem, where the mutual fund referred to is the tangency portfolio.

(a.k.a. portfolio risk or market risk) refers to the risk common to all securities—except for selling short as noted below, systematic risk cannot be diversified away (within one market). Within the market portfolio, asset specific risk will be diversified away to the extent possible. Systematic risk is therefore equated with the risk (standard deviation) of the market portfolio.

Since a security will be purchased only if it improves the risk-expected return characteristics of the market portfolio, the relevant measure of the risk of a security is the risk it adds to the market portfolio, and not its risk in isolation.

In this context, the volatility of the asset, and its correlation with the market portfolio, are historically observed and are therefore given. (There are several approaches to asset pricing that attempt to price assets by modelling the stochastic properties of the moments of assets' returns - these are broadly referred to as conditional asset pricing models.)

Systematic risks within one market can be managed through a strategy of using both long and short positions within one portfolio, creating a "market neutral" portfolio.

is a model which derives the theoretical required expected return (i.e., discount rate) for an asset in a market, given the risk-free rate available to investors and the risk of the market as a whole. The CAPM is usually expressed:

This equation can be statistically estimated

using the following regression

equation:

where αi is called the asset's alpha, βi is the asset's beta coefficient

and SCL is the Security Characteristic Line

.

Once an asset's expected return, , is calculated using CAPM, the future cash flow

, is calculated using CAPM, the future cash flow

s of the asset can be discounted to their present value

using this rate to establish the correct price for the asset. A riskier stock will have a higher beta and will be discounted at a higher rate; less sensitive stocks will have lower betas and be discounted at a lower rate. In theory, an asset is correctly priced when its observed price is the same as its value calculated using the CAPM derived discount rate. If the observed price is higher than the valuation, then the asset is overvalued; it is undervalued for a too low price.

Efforts to translate the theoretical foundation into a viable portfolio construction algorithm have been plagued by technical difficulties stemming from the instability of the original optimization problem with respect to the available data. Recent research has shown that instabilities of this type disappear when a regularizing constraint or penalty term is incorporated in the optimization procedure.

More complex versions of MPT can take into account a more sophisticated model of the world (such as one with non-normal distributions and taxes) but all mathematical models of finance still rely on many unrealistic premises.

s, which means that they are mathematical statements about the future (the expected value of returns is explicit in the above equations, and implicit in the definitions of variance

and covariance

). In practice investors must substitute predictions based on historical measurements of asset return and volatility

for these values in the equations. Very often such expected values fail to take account of new circumstances which did not exist when the historical data were generated.

More fundamentally, investors are stuck with estimating key parameters from past market data because MPT attempts to model risk in terms of the likelihood of losses, but says nothing about why those losses might occur. The risk measurements used are probabilistic

in nature, not structural. This is a major difference as compared to many engineering approaches to risk management

.

Essentially, the mathematics of MPT view the markets as a collection of dice. By examining past market data we can develop hypotheses about how the dice are weighted, but this isn't helpful if the markets are actually dependent upon a much bigger and more complicated chaotic

system—the world. For this reason, accurate structural models of real financial markets are unlikely to be forthcoming because they would essentially be structural models of the entire world. Nonetheless there is growing awareness of the concept of systemic risk

in financial markets, which should lead to more sophisticated market models.

Mathematical risk measurements are also useful only to the degree that they reflect investors' true concerns—there is no point minimizing a variable that nobody cares about in practice. MPT uses the mathematical concept of variance

to quantify risk, and this might be justified under the assumption of elliptically distributed

returns such as normally distributed returns, but for general return distributions

other risk measures (like coherent risk measure

s) might better reflect investors' true preferences.

In particular, variance

is a symmetric measure that counts abnormally high returns as just as risky as abnormally low returns. Some would argue that, in reality, investors are only concerned about losses, and do not care about the dispersion or tightness of above-average returns. According to this view, our intuitive concept of risk is fundamentally asymmetric in nature.

MPT does not account for the personal, environmental, strategic, or social dimensions of investment decisions. It only attempts to maximize risk-adjusted returns, without regard to other consequences. In a narrow sense, its complete reliance on asset price

s makes it vulnerable to all the standard market failures such as those arising from information asymmetry

, externalities, and public goods. It also rewards corporate fraud and dishonest accounting. More broadly, a firm may have strategic or social goals that shape its investment decisions, and an individual investor might have personal goals. In either case, information other than historical returns is relevant.

Financial economist Nassim Nicholas Taleb has also criticized modern portfolio theory because it assumes a Gaussian distribution:

. Diversification forces the portfolio manager to invest in assets without analyzing their fundamentals, solely for the benefit of eliminating the portfolio’s non-systematic risk (the CAPM assumes investment in all available assets). This artificially increased demand pushes up the price of assets that, when analyzed individually, would be of little fundamental value. The result is that the whole portfolio becomes more expensive and, as a result, the probability of a positive return decreases (i.e. the risk of the portfolio increases).

Empirical evidence for this is the price hike that stocks typically experience once they are included in major indices like the S&P 500

.

Post-modern portfolio theory

extends MPT by adopting non-normally distributed, asymmetric measures of risk. This helps with some of these problems, but not others.

Black-Litterman model

optimization is an extension of unconstrained Markowitz optimization which incorporates relative and absolute `views' on inputs of risk and returns.

Neither of these necessarily eliminate the possibility of using MPT and such portfolios. They simply indicate the need to run the optimization with an additional set of mathematically-expressed constraints that would not normally apply to financial portfolios.

Furthermore, some of the simplest elements of Modern Portfolio Theory are applicable to virtually any kind of portfolio. The concept of capturing the risk tolerance of an investor by documenting how much risk is acceptable for a given return may be applied to a variety of decision analysis problems. MPT uses historical variance as a measure of risk, but portfolios of assets like major projects don't have a well-defined "historical variance". In this case, the MPT investment boundary can be expressed in more general terms like "chance of an ROI less than cost of capital" or "chance of losing more than half of the investment". When risk is put in terms of uncertainty about forecasts and possible losses then the concept is transferable to various types of investment.

. In a series of seminal works, Michael Conroy modeled the labor force in the economy using portfolio-theoretic methods to examine growth and variability in the labor force. This was followed by a long literature on the relationship between economic growth and volatility.

More recently, modern portfolio theory has been used to model the self-concept in social psychology. When the self attributes comprising the self-concept constitute a well-diversified portfolio, then psychological outcomes at the level of the individual such as mood and self-esteem should be more stable than when the self-concept is undiversified. This prediction has been confirmed in studies involving human subjects.

Recently, modern portfolio theory has been applied to modelling the uncertainty and correlation between documents in information retrieval. Given a query, the aim is to maximize the overall relevance of a ranked list of documents and at the same time minimize the overall uncertainty of the ranked list.

(APT), which holds that the expected return

of a financial asset can be modeled as a linear function

of various macro-economic

factors, where sensitivity to changes in each factor is represented by a factor specific beta coefficient

.

The APT is less restrictive in its assumptions: it allows for a statistical model of asset returns, and assumes that each investor will hold a unique portfolio with its own particular array of betas, as opposed to the identical "market portfolio". Unlike the CAPM, the APT, however, does not itself reveal the identity of its priced factors - the number and nature of these factors is likely to change over time and between economies.

Investment

Investment has different meanings in finance and economics. Finance investment is putting money into something with the expectation of gain, that upon thorough analysis, has a high degree of security for the principal amount, as well as security of return, within an expected period of time...

which attempts to maximize portfolio expected return

Rate of return

In finance, rate of return , also known as return on investment , rate of profit or sometimes just return, is the ratio of money gained or lost on an investment relative to the amount of money invested. The amount of money gained or lost may be referred to as interest, profit/loss, gain/loss, or...

for a given amount of portfolio risk, or equivalently minimize risk

Financial risk

Financial risk an umbrella term for multiple types of risk associated with financing, including financial transactions that include company loans in risk of default. Risk is a term often used to imply downside risk, meaning the uncertainty of a return and the potential for financial loss...

for a given level of expected return, by carefully choosing the proportions of various asset

Asset

In financial accounting, assets are economic resources. Anything tangible or intangible that is capable of being owned or controlled to produce value and that is held to have positive economic value is considered an asset...

s. Although MPT is widely used in practice in the financial industry and several of its creators won a Nobel memorial prize

Nobel Memorial Prize in Economic Sciences

The Nobel Memorial Prize in Economic Sciences, commonly referred to as the Nobel Prize in Economics, but officially the Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel , is an award for outstanding contributions to the field of economics, generally regarded as one of the...

for the theory, in recent years the basic assumptions of MPT have been widely challenged by fields such as behavioral economics.

MPT is a mathematical formulation of the concept of diversification

Diversification (finance)

In finance, diversification means reducing risk by investing in a variety of assets. If the asset values do not move up and down in perfect synchrony, a diversified portfolio will have less risk than the weighted average risk of its constituent assets, and often less risk than the least risky of...

in investing, with the aim of selecting a collection of investment assets that has collectively lower risk than any individual asset. That this is possible can be seen intuitively because different types of assets often change in value in opposite ways. For example, to the extent prices in the stock market

Stock market

A stock market or equity market is a public entity for the trading of company stock and derivatives at an agreed price; these are securities listed on a stock exchange as well as those only traded privately.The size of the world stock market was estimated at about $36.6 trillion...

move differently from prices in the bond market

Bond market

The bond market is a financial market where participants can issue new debt, known as the primary market, or buy and sell debt securities, known as the Secondary market, usually in the form of bonds. The primary goal of the bond market is to provide a mechanism for long term funding of public and...

, a collection of both types of assets can in theory face lower overall risk than either individually. But diversification lowers risk even if assets' returns are not negatively correlated—indeed, even if they are positively correlated.

More technically, MPT models an asset's return as a normally distributed function (or more generally as an elliptically distributed

Elliptical distribution

In probability and statistics, an elliptical distribution is any member of a broad family of probability distributions that generalize the multivariate normal distribution and inherit some of its properties.-Definition:...

random variable

Random variable

In probability and statistics, a random variable or stochastic variable is, roughly speaking, a variable whose value results from a measurement on some type of random process. Formally, it is a function from a probability space, typically to the real numbers, which is measurable functionmeasurable...

), defines risk

Risk

Risk is the potential that a chosen action or activity will lead to a loss . The notion implies that a choice having an influence on the outcome exists . Potential losses themselves may also be called "risks"...

as the standard deviation

Standard deviation

Standard deviation is a widely used measure of variability or diversity used in statistics and probability theory. It shows how much variation or "dispersion" there is from the average...

of return, and models a portfolio as a weighted combination of assets, so that the return of a portfolio is the weighted combination of the assets' returns. By combining different assets whose returns are not perfectly positively correlated, MPT seeks to reduce the total variance

Variance

In probability theory and statistics, the variance is a measure of how far a set of numbers is spread out. It is one of several descriptors of a probability distribution, describing how far the numbers lie from the mean . In particular, the variance is one of the moments of a distribution...

of the portfolio return. MPT also assumes that investors are rational

Homo economicus

Homo economicus, or Economic human, is the concept in some economic theories of humans as rational and narrowly self-interested actors who have the ability to make judgments toward their subjectively defined ends...

and markets are efficient

Efficient market hypothesis

In finance, the efficient-market hypothesis asserts that financial markets are "informationally efficient". That is, one cannot consistently achieve returns in excess of average market returns on a risk-adjusted basis, given the information available at the time the investment is made.There are...

.

MPT was developed in the 1950s through the early 1970s and was considered an important advance in the mathematical modeling of finance. Since then, many theoretical and practical criticisms have been leveled against it. These include the fact that financial returns do not follow a Gaussian distribution or indeed any symmetric distribution, and that correlations between asset classes are not fixed but can vary depending on external events (especially in crises). Further, there is growing evidence that investors are not rational and markets are not efficient

Efficient market hypothesis

In finance, the efficient-market hypothesis asserts that financial markets are "informationally efficient". That is, one cannot consistently achieve returns in excess of average market returns on a risk-adjusted basis, given the information available at the time the investment is made.There are...

.

Concept

The fundamental concept behind MPT is that the assetAsset

In financial accounting, assets are economic resources. Anything tangible or intangible that is capable of being owned or controlled to produce value and that is held to have positive economic value is considered an asset...

s in an investment portfolio

Portfolio (finance)

Portfolio is a financial term denoting a collection of investments held by an investment company, hedge fund, financial institution or individual.-Definition:The term portfolio refers to any collection of financial assets such as stocks, bonds and cash...

should not be selected individually, each on their own merits. Rather, it is important to consider how each asset changes in price relative to how every other asset in the portfolio changes in price.

Investing is a tradeoff between risk

Risk

Risk is the potential that a chosen action or activity will lead to a loss . The notion implies that a choice having an influence on the outcome exists . Potential losses themselves may also be called "risks"...

and expected return. In general, assets with higher expected returns are riskier. For a given amount of risk, MPT describes how to select a portfolio with the highest possible expected return. Or, for a given expected return, MPT explains how to select a portfolio with the lowest possible risk (the targeted expected return cannot be more than the highest-returning available security, of course, unless negative holdings of assets are possible.)

Therefore, MPT is a form of diversification

Diversification (finance)

In finance, diversification means reducing risk by investing in a variety of assets. If the asset values do not move up and down in perfect synchrony, a diversified portfolio will have less risk than the weighted average risk of its constituent assets, and often less risk than the least risky of...

. Under certain assumptions and for specific quantitative

Quantification

Quantification has several distinct senses. In mathematics and empirical science, it is the act of counting and measuring that maps human sense observations and experiences into members of some set of numbers. Quantification in this sense is fundamental to the scientific method.In logic,...

definitions of risk and return, MPT explains how to find the best possible diversification strategy.

History

Harry MarkowitzHarry Markowitz

Harry Max Markowitz is an American economist and a recipient of the John von Neumann Theory Prize and the Nobel Memorial Prize in Economic Sciences....

introduced MPT in a 1952 article and a 1959 book. Markowitz classifies it simply as "Portfolio Theory," because "There's nothing modern about it." See also this survey of the history.

The portfolio management is combination security and risk, due to markowitz approach investor can analyse the varies security and risk which gave highest return and minimum risk.

Mathematical model

In some sense the mathematical derivation below is MPT, although the basic concepts behind the model have also been very influential.This section develops the "classic" MPT model. There have been many extensions since.

Risk and expected return

MPT assumes that investors are risk averse, meaning that given two portfolios that offer the same expected return, investors will prefer the less risky one. Thus, an investor will take on increased risk only if compensated by higher expected returns. Conversely, an investor who wants higher expected returns must accept more risk. The exact trade-off will be the same for all investors, but different investors will evaluate the trade-off differently based on individual risk aversion characteristics. The implication is that a rationalRationality

In philosophy, rationality is the exercise of reason. It is the manner in which people derive conclusions when considering things deliberately. It also refers to the conformity of one's beliefs with one's reasons for belief, or with one's actions with one's reasons for action...

investor will not invest in a portfolio if a second portfolio exists with a more favorable risk-expected return profile

Risk-return spectrum

The risk-return spectrum is the relationship between the amount of return gained on an investment and the amount of risk undertaken in that investment. The more return sought, the more risk that must be undertaken.-The progression:...

– i.e., if for that level of risk an alternative portfolio exists which has better expected returns.

Note that the theory uses standard deviation of return as a proxy for risk, which is valid if asset returns are jointly normally distributed or otherwise elliptically distributed

Elliptical distribution

In probability and statistics, an elliptical distribution is any member of a broad family of probability distributions that generalize the multivariate normal distribution and inherit some of its properties.-Definition:...

. There are problems with this, however; see criticism.

Under the model:

- Portfolio return is the proportion-weighted combinationLinear combinationIn mathematics, a linear combination is an expression constructed from a set of terms by multiplying each term by a constant and adding the results...

of the constituent assets' returns. - Portfolio volatility is a function of the correlationCorrelationIn statistics, dependence refers to any statistical relationship between two random variables or two sets of data. Correlation refers to any of a broad class of statistical relationships involving dependence....

s ρij of the component assets, for all asset pairs (i, j).

In general:

- Expected return:

- where

is the return on the portfolio,

is the return on asset i and

is the weighting of component asset

(that is, the share of asset i in the portfolio).

- Portfolio return variance:

- where

is the correlation coefficient

Pearson product-moment correlation coefficientIn statistics, the Pearson product-moment correlation coefficient is a measure of the correlation between two variables X and Y, giving a value between +1 and −1 inclusive...

between the returns on assets i and j. Alternatively the expression can be written as:

,

- where

for i=j.

- Portfolio return volatility (standard deviation):

For a two asset portfolio:

- Portfolio return:

- Portfolio variance:

For a three asset portfolio:

- Portfolio return:

- Portfolio variance:

Diversification

An investor can reduce portfolio risk simply by holding combinations of instruments which are not perfectly positively correlatedCorrelation

In statistics, dependence refers to any statistical relationship between two random variables or two sets of data. Correlation refers to any of a broad class of statistical relationships involving dependence....

(correlation coefficient

Pearson product-moment correlation coefficient

In statistics, the Pearson product-moment correlation coefficient is a measure of the correlation between two variables X and Y, giving a value between +1 and −1 inclusive...

). In other words, investors can reduce their exposure to individual asset risk by holding a diversifiedDiversification (finance)

In finance, diversification means reducing risk by investing in a variety of assets. If the asset values do not move up and down in perfect synchrony, a diversified portfolio will have less risk than the weighted average risk of its constituent assets, and often less risk than the least risky of...

portfolio of assets. Diversification may allow for the same portfolio expected return with reduced risk.

If all the asset pairs have correlations of 0—they are perfectly uncorrelated—the portfolio's return variance is the sum over all assets of the square of the fraction held in the asset times the asset's return variance (and the portfolio standard deviation is the square root of this sum).

The efficient frontier with no risk-free asset

MatricesMatrix (mathematics)In mathematics, a matrix is a rectangular array of numbers, symbols, or expressions. The individual items in a matrix are called its elements or entries. An example of a matrix with six elements isMatrices of the same size can be added or subtracted element by element...

are preferred for calculations of the efficient frontier.

In matrix form, for a given "risk tolerance", the efficient frontier is found by minimizing the following expression:

where

is a vector of portfolio weights and

(The weights can be negative, which means investors can short a security.);

is the covariance matrix

Covariance matrixIn probability theory and statistics, a covariance matrix is a matrix whose element in the i, j position is the covariance between the i th and j th elements of a random vector...

for the returns on the assets in the portfolio;

is a "risk tolerance" factor, where 0 results in the portfolio with minimal risk and

results in the portfolio infinitely far out on the frontier with both expected return and risk unbounded; and

is a vector of expected returns.

is the variance of portfolio return.

is the expected return on the portfolio.

The above optimization finds the point on the frontier at which the inverse of the slope of the frontier would be q if portfolio return variance instead of standard deviation were plotted horizontally. The frontier in its entirety is parametric on q.

Many software packages, including Microsoft ExcelMicrosoft ExcelMicrosoft Excel is a proprietary commercial spreadsheet application written and distributed by Microsoft for Microsoft Windows and Mac OS X. It features calculation, graphing tools, pivot tables, and a macro programming language called Visual Basic for Applications...

, MathematicaMathematicaMathematica is a computational software program used in scientific, engineering, and mathematical fields and other areas of technical computing...

and RR (programming language)R is a programming language and software environment for statistical computing and graphics. The R language is widely used among statisticians for developing statistical software, and R is widely used for statistical software development and data analysis....

, provide optimizationQuadratic programmingQuadratic programming is a special type of mathematical optimization problem. It is the problem of optimizing a quadratic function of several variables subject to linear constraints on these variables....

routines suitable for the above problem.

An alternative approach to specifying the efficient frontier is to do so parametrically on the expected portfolio returnThis version of the problem requires that we minimize

subject to

for parameter. This problem is easily solved using a Lagrange multiplier.

The two mutual fund theorem

One key result of the above analysis is the two mutual fund theorem. This theorem states that any portfolio on the efficient frontier can be generated by holding a combination of any two given portfolios on the frontier; the latter two given portfolios are the "mutual funds" in the theorem's name. So in the absence of a risk-free asset, an investor can achieve any desired efficient portfolio even if all that is accessible is a pair of efficient mutual funds. If the location of the desired portfolio on the frontier is between the locations of the two mutual funds, both mutual funds will be held in positive quantities. If the desired portfolio is outside the range spanned by the two mutual funds, then one of the mutual funds must be sold short (held in negative quantity) while the size of the investment in the other mutual fund must be greater than the amount available for investment (the excess being funded by the borrowing from the other fund).The risk-free asset and the capital allocation line

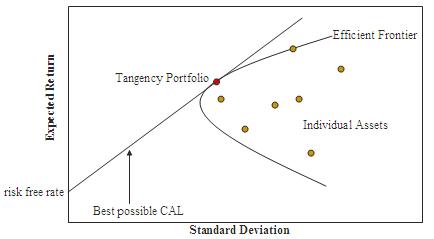

The risk-free asset is the (hypothetical) asset which pays a risk-free rate. In practice, short-term government securities (such as US treasury bills) are used as a risk-free asset, because they pay a fixed rate of interest and have exceptionally low defaultDefault (finance)

In finance, default occurs when a debtor has not met his or her legal obligations according to the debt contract, e.g. has not made a scheduled payment, or has violated a loan covenant of the debt contract. A default is the failure to pay back a loan. Default may occur if the debtor is either...

risk. The risk-free asset has zero variance in returns (hence is risk-free); it is also uncorrelated with any other asset (by definition, since its variance is zero). As a result, when it is combined with any other asset or portfolio of assets, the change in return is linearly related to the change in risk as the proportions in the combination vary.

When a risk-free asset is introduced, the half-line shown in the figure is the new efficient frontier. It is tangent to the hyperbola at the pure risky portfolio with the highest Sharpe ratio

Sharpe ratio

The Sharpe ratio or Sharpe index or Sharpe measure or reward-to-variability ratio is a measure of the excess return per unit of deviation in an investment asset or a trading strategy, typically referred to as risk , named after William Forsyth Sharpe...

. Its horizontal intercept represents a portfolio with 100% of holdings in the risk-free asset; the tangency with the hyperbola represents a portfolio with no risk-free holdings and 100% of assets held in the portfolio occurring at the tangency point; points between those points are portfolios containing positive amounts of both the risky tangency portfolio and the risk-free asset; and points on the half-line beyond the tangency point are leverage

Leverage (finance)

In finance, leverage is a general term for any technique to multiply gains and losses. Common ways to attain leverage are borrowing money, buying fixed assets and using derivatives. Important examples are:* A public corporation may leverage its equity by borrowing money...

d portfolios involving negative holdings of the risk-free asset (the latter has been sold short—in other words, the investor has borrowed at the risk-free rate) and an amount invested in the tangency portfolio equal to more than 100% of the investor's initial capital. This efficient half-line is called the capital allocation line

Capital allocation line

Capital allocation line is a graph created by investors to measure the risk of risky and risk-free assets. The graph displays to the investors on the return they can make by taking on a certain level of risk...

(CAL), and its formula can be shown to be

In this formula P is the sub-portfolio of risky assets at the tangency with the Markowitz bullet, F is the risk-free asset, and C is a combination of portfolios P and F.

By the diagram, the introduction of the risk-free asset as a possible component of the portfolio has improved the range of risk-expected return combinations available, because everywhere except at the tangency portfolio the half-line gives a higher expected return than the hyperbola does at every possible risk level. The fact that all points on the linear efficient locus can be achieved by a combination of holdings of the risk-free asset and the tangency portfolio is known as the one mutual fund theorem, where the mutual fund referred to is the tangency portfolio.

Asset pricing using MPT

The above analysis describes optimal behavior of an individual investor. Asset pricing theory builds on this analysis in the following way. Since everyone holds the risky assets in identical proportions to each other—namely in the proportions given by the tangency portfolio—in market equilibrium the risky assets' prices, and therefore their expected returns, will adjust so that the ratios in the tangency portfolio are the same as the ratios in which the risky assets are supplied to the market. Thus relative supplies will equal relative demands. MPT derives the required expected return for a correctly priced asset in this context.Systematic risk and specific risk

Specific risk is the risk associated with individual assets - within a portfolio these risks can be reduced through diversification (specific risks "cancel out"). Specific risk is also called diversifiable, unique, unsystematic, or idiosyncratic risk. Systematic riskSystematic risk

In finance, systematic risk, sometimes called market risk, aggregate risk, or undiversifiable risk, is the risk associated with aggregate market returns....

(a.k.a. portfolio risk or market risk) refers to the risk common to all securities—except for selling short as noted below, systematic risk cannot be diversified away (within one market). Within the market portfolio, asset specific risk will be diversified away to the extent possible. Systematic risk is therefore equated with the risk (standard deviation) of the market portfolio.

Since a security will be purchased only if it improves the risk-expected return characteristics of the market portfolio, the relevant measure of the risk of a security is the risk it adds to the market portfolio, and not its risk in isolation.

In this context, the volatility of the asset, and its correlation with the market portfolio, are historically observed and are therefore given. (There are several approaches to asset pricing that attempt to price assets by modelling the stochastic properties of the moments of assets' returns - these are broadly referred to as conditional asset pricing models.)

Systematic risks within one market can be managed through a strategy of using both long and short positions within one portfolio, creating a "market neutral" portfolio.

Capital asset pricing model

The asset return depends on the amount paid for the asset today. The price paid must ensure that the market portfolio's risk / return characteristics improve when the asset is added to it. The CAPMCapital asset pricing model

In finance, the capital asset pricing model is used to determine a theoretically appropriate required rate of return of an asset, if that asset is to be added to an already well-diversified portfolio, given that asset's non-diversifiable risk...

is a model which derives the theoretical required expected return (i.e., discount rate) for an asset in a market, given the risk-free rate available to investors and the risk of the market as a whole. The CAPM is usually expressed:

, Beta, is the measure of asset sensitivity to a movement in the overall market; Beta is usually found via regressionRegression analysisIn statistics, regression analysis includes many techniques for modeling and analyzing several variables, when the focus is on the relationship between a dependent variable and one or more independent variables...

, Beta, is the measure of asset sensitivity to a movement in the overall market; Beta is usually found via regressionRegression analysisIn statistics, regression analysis includes many techniques for modeling and analyzing several variables, when the focus is on the relationship between a dependent variable and one or more independent variables...

on historical data. Betas exceeding one signify more than average "riskiness" in the sense of the asset's contribution to overall portfolio risk; betas below one indicate a lower than average risk contribution.

is the market premium, the expected excess return of the market portfolio's expected return over the risk-free rate.

is the market premium, the expected excess return of the market portfolio's expected return over the risk-free rate.

This equation can be statistically estimated

Estimation theory

Estimation theory is a branch of statistics and signal processing that deals with estimating the values of parameters based on measured/empirical data that has a random component. The parameters describe an underlying physical setting in such a way that their value affects the distribution of the...

using the following regression

Regression analysis

In statistics, regression analysis includes many techniques for modeling and analyzing several variables, when the focus is on the relationship between a dependent variable and one or more independent variables...

equation:

where αi is called the asset's alpha, βi is the asset's beta coefficient

Beta coefficient

In finance, the Beta of a stock or portfolio is a number describing the relation of its returns with those of the financial market as a whole.An asset has a Beta of zero if its returns change independently of changes in the market's returns...

and SCL is the Security Characteristic Line

Security characteristic line

Security characteristic line is a regression line, plotting performance of a particular security or portfolio against that of the market portfolio at every point in time. The SCL is plotted on a graph where the Y-axis is the excess return on a security over the risk-free return and the X-axis is...

.

Once an asset's expected return,

, is calculated using CAPM, the future cash flowCash flow

Cash flow is the movement of money into or out of a business, project, or financial product. It is usually measured during a specified, finite period of time. Measurement of cash flow can be used for calculating other parameters that give information on a company's value and situation.Cash flow...

s of the asset can be discounted to their present value

Present value

Present value, also known as present discounted value, is the value on a given date of a future payment or series of future payments, discounted to reflect the time value of money and other factors such as investment risk...

using this rate to establish the correct price for the asset. A riskier stock will have a higher beta and will be discounted at a higher rate; less sensitive stocks will have lower betas and be discounted at a lower rate. In theory, an asset is correctly priced when its observed price is the same as its value calculated using the CAPM derived discount rate. If the observed price is higher than the valuation, then the asset is overvalued; it is undervalued for a too low price.

(1) The incremental impact on risk and expected return when an additional risky asset, a, is added to the market portfolio, m, follows from the formulae for a two-asset portfolio. These results are used to derive the asset-appropriate discount rate.

- Market portfolio's risk =

- Hence, risk added to portfolio =

- but since the weight of the asset will be relatively low,

- i.e. additional risk =

- Market portfolio's expected return =

- Hence additional expected return =

(2) If an asset, a, is correctly priced, the improvement in its risk-to-expected return ratio achieved by adding it to the market portfolio, m, will at least match the gains of spending that money on an increased stake in the market portfolio. The assumption is that the investor will purchase the asset with funds borrowed at the risk-free rate,; this is rational if

.

- Thus:

- i.e. :

- i.e. :

is the “beta”,

return— the covariance

CovarianceIn probability theory and statistics, covariance is a measure of how much two variables change together. Variance is a special case of the covariance when the two variables are identical.- Definition :...

between the asset's return and the market's return divided by the variance of the market return— i.e. the sensitivity of the asset price to movement in the market portfolio's value.

Criticism

Despite its theoretical importance, critics of MPT question whether it is an ideal investing strategy, because its model of financial markets does not match the real world in many ways.Efforts to translate the theoretical foundation into a viable portfolio construction algorithm have been plagued by technical difficulties stemming from the instability of the original optimization problem with respect to the available data. Recent research has shown that instabilities of this type disappear when a regularizing constraint or penalty term is incorporated in the optimization procedure.

Assumptions

The framework of MPT makes many assumptions about investors and markets. Some are explicit in the equations, such as the use of Normal distributions to model returns. Others are implicit, such as the neglect of taxes and transaction fees. None of these assumptions are entirely true, and each of them compromises MPT to some degree.- Investors are interested in the optimization problem described above (maximizing the mean for a given variance). In reality, investors have utility functions that may sensitive to higher moments of the distribution of the returns. For the investors to use the mean-variance optimization, on must suppose that the combination of utility and returns make the optimization of utility problem similar to the mean-variance optimization problem. A quadratic utility without any assumption about returns is sufficient. Another assumption is to use exponential utility and normal distribution, as discussed below.

- Asset returns are (jointly) normally distributed random variables. In fact, it is frequently observed that returns in equity and other markets are not normally distributed. Large swings (3 to 6 standard deviations from the mean) occur in the market far more frequently than the normal distribution assumption would predict. While the model can also be justified by assuming any return distribution which is jointly ellipticalElliptical distributionIn probability and statistics, an elliptical distribution is any member of a broad family of probability distributions that generalize the multivariate normal distribution and inherit some of its properties.-Definition:...

, all the joint elliptical distributions are symmetrical whereas asset returns empirically are not.

- Correlations between assets are fixed and constant forever. Correlations depend on systemic relationships between the underlying assets, and change when these relationships change. Examples include one country declaring war on another, or a general market crash. During times of financial crisis all assets tend to become positively correlated, because they all move (down) together. In other words, MPT breaks down precisely when investors are most in need of protection from risk.

- All investors aim to maximize economic utility (in other words, to make as much money as possible, regardless of any other considerations). This is a key assumption of the efficient market hypothesisEfficient market hypothesisIn finance, the efficient-market hypothesis asserts that financial markets are "informationally efficient". That is, one cannot consistently achieve returns in excess of average market returns on a risk-adjusted basis, given the information available at the time the investment is made.There are...

, upon which MPT relies.

- All investors are rational and risk-averse. This is another assumption of the efficient market hypothesisEfficient market hypothesisIn finance, the efficient-market hypothesis asserts that financial markets are "informationally efficient". That is, one cannot consistently achieve returns in excess of average market returns on a risk-adjusted basis, given the information available at the time the investment is made.There are...

, but we now know from behavioral economics that market participants are not rationalRational choice theoryRational choice theory, also known as choice theory or rational action theory, is a framework for understanding and often formally modeling social and economic behavior. It is the main theoretical paradigm in the currently-dominant school of microeconomics...

. It does not allow for "herd behavior" or investors who will accept lower returns for higher risk. Casino gamblersGamblingGambling is the wagering of money or something of material value on an event with an uncertain outcome with the primary intent of winning additional money and/or material goods...

clearly pay for risk, and it is possible that some stock traders will pay for risk as well.

- All investors have access to the same information at the same time. In fact, real markets contain information asymmetryInformation asymmetryIn economics and contract theory, information asymmetry deals with the study of decisions in transactions where one party has more or better information than the other. This creates an imbalance of power in transactions which can sometimes cause the transactions to go awry, a kind of market failure...

, insider tradingInsider tradingInsider trading is the trading of a corporation's stock or other securities by individuals with potential access to non-public information about the company...

, and those who are simply better informed than others. Moreover, estimating the mean (for instance, there is no consistent estimator of the drift of a brownian when subsampling between 0 and T) and the covariance matrix of the returns (when the number of assets is of the same order of the number of periods) are difficult statistical tasks.

- Investors have an accurate conception of possible returns, i.e., the probability beliefs of investors match the true distribution of returns. A different possibility is that investors' expectations are biased, causing market prices to be informationally inefficient. This possibility is studied in the field of behavioral financeBehavioral financeBehavioral economics and its related area of study, behavioral finance, use social, cognitive and emotional factors in understanding the economic decisions of individuals and institutions performing economic functions, including consumers, borrowers and investors, and their effects on market...

, which uses psychological assumptions to provide alternatives to the CAPM such as the overconfidence-based asset pricing model of Kent Daniel, David HirshleiferDavid HirshleiferDavid Hirshleifer is a prominent American economist. He is a professor of finance and currently holds the Merage chair in Business Growth at the University of California at Irvine. He previously held tenured positions at the University of Michigan, The Ohio State University, and UCLA. His work...

, and Avanidhar Subrahmanyam (2001).

- There are no taxes or transaction costs. Real financial products are subject both to taxes and transaction costs (such as broker fees), and taking these into account will alter the composition of the optimum portfolio. These assumptions can be relaxed with more complicated versions of the model.

- All investors are price takers, i.e., their actions do not influence prices. In reality, sufficiently large sales or purchases of individual assets can shift market prices for that asset and others (via cross-elasticity of demand.) An investor may not even be able to assemble the theoretically optimal portfolio if the market moves too much while they are buying the required securities.

- Any investor can lend and borrow an unlimited amount at the risk free rate of interest. In reality, every investor has a credit limit.

- All securities can be divided into parcels of any size. In reality, fractional shares usually cannot be bought or sold, and some assets have minimum orders sizes.

More complex versions of MPT can take into account a more sophisticated model of the world (such as one with non-normal distributions and taxes) but all mathematical models of finance still rely on many unrealistic premises.

MPT does not really model the market

The risk, return, and correlation measures used by MPT are based on expected valueExpected value

In probability theory, the expected value of a random variable is the weighted average of all possible values that this random variable can take on...

s, which means that they are mathematical statements about the future (the expected value of returns is explicit in the above equations, and implicit in the definitions of variance

Variance

In probability theory and statistics, the variance is a measure of how far a set of numbers is spread out. It is one of several descriptors of a probability distribution, describing how far the numbers lie from the mean . In particular, the variance is one of the moments of a distribution...

and covariance

Covariance

In probability theory and statistics, covariance is a measure of how much two variables change together. Variance is a special case of the covariance when the two variables are identical.- Definition :...

). In practice investors must substitute predictions based on historical measurements of asset return and volatility

Volatility (finance)

In finance, volatility is a measure for variation of price of a financial instrument over time. Historic volatility is derived from time series of past market prices...

for these values in the equations. Very often such expected values fail to take account of new circumstances which did not exist when the historical data were generated.

More fundamentally, investors are stuck with estimating key parameters from past market data because MPT attempts to model risk in terms of the likelihood of losses, but says nothing about why those losses might occur. The risk measurements used are probabilistic

Probability

Probability is ordinarily used to describe an attitude of mind towards some proposition of whose truth we arenot certain. The proposition of interest is usually of the form "Will a specific event occur?" The attitude of mind is of the form "How certain are we that the event will occur?" The...

in nature, not structural. This is a major difference as compared to many engineering approaches to risk management

Risk management

Risk management is the identification, assessment, and prioritization of risks followed by coordinated and economical application of resources to minimize, monitor, and control the probability and/or impact of unfortunate events or to maximize the realization of opportunities...

.

Essentially, the mathematics of MPT view the markets as a collection of dice. By examining past market data we can develop hypotheses about how the dice are weighted, but this isn't helpful if the markets are actually dependent upon a much bigger and more complicated chaotic

Chaos theory

Chaos theory is a field of study in mathematics, with applications in several disciplines including physics, economics, biology, and philosophy. Chaos theory studies the behavior of dynamical systems that are highly sensitive to initial conditions, an effect which is popularly referred to as the...

system—the world. For this reason, accurate structural models of real financial markets are unlikely to be forthcoming because they would essentially be structural models of the entire world. Nonetheless there is growing awareness of the concept of systemic risk

Systemic risk

In finance, systemic risk is the risk of collapse of an entire financial system or entire market, as opposed to risk associated with any one individual entity, group or component of a system. It can be defined as "financial system instability, potentially catastrophic, caused or exacerbated by...

in financial markets, which should lead to more sophisticated market models.

Mathematical risk measurements are also useful only to the degree that they reflect investors' true concerns—there is no point minimizing a variable that nobody cares about in practice. MPT uses the mathematical concept of variance

Variance

In probability theory and statistics, the variance is a measure of how far a set of numbers is spread out. It is one of several descriptors of a probability distribution, describing how far the numbers lie from the mean . In particular, the variance is one of the moments of a distribution...

to quantify risk, and this might be justified under the assumption of elliptically distributed

Elliptical distribution

In probability and statistics, an elliptical distribution is any member of a broad family of probability distributions that generalize the multivariate normal distribution and inherit some of its properties.-Definition:...

returns such as normally distributed returns, but for general return distributions

Probability distribution

In probability theory, a probability mass, probability density, or probability distribution is a function that describes the probability of a random variable taking certain values....

other risk measures (like coherent risk measure

Coherent risk measure

In the field of financial economics there are a number of ways that risk can be defined; to clarify the concept theoreticians have described a number of properties that a risk measure might or might not have...

s) might better reflect investors' true preferences.

In particular, variance

Variance

In probability theory and statistics, the variance is a measure of how far a set of numbers is spread out. It is one of several descriptors of a probability distribution, describing how far the numbers lie from the mean . In particular, the variance is one of the moments of a distribution...

is a symmetric measure that counts abnormally high returns as just as risky as abnormally low returns. Some would argue that, in reality, investors are only concerned about losses, and do not care about the dispersion or tightness of above-average returns. According to this view, our intuitive concept of risk is fundamentally asymmetric in nature.

MPT does not account for the personal, environmental, strategic, or social dimensions of investment decisions. It only attempts to maximize risk-adjusted returns, without regard to other consequences. In a narrow sense, its complete reliance on asset price

Price

-Definition:In ordinary usage, price is the quantity of payment or compensation given by one party to another in return for goods or services.In modern economies, prices are generally expressed in units of some form of currency...

s makes it vulnerable to all the standard market failures such as those arising from information asymmetry

Information asymmetry

In economics and contract theory, information asymmetry deals with the study of decisions in transactions where one party has more or better information than the other. This creates an imbalance of power in transactions which can sometimes cause the transactions to go awry, a kind of market failure...

, externalities, and public goods. It also rewards corporate fraud and dishonest accounting. More broadly, a firm may have strategic or social goals that shape its investment decisions, and an individual investor might have personal goals. In either case, information other than historical returns is relevant.

Financial economist Nassim Nicholas Taleb has also criticized modern portfolio theory because it assumes a Gaussian distribution:

- After the stock market crash (in 1987), they rewarded two theoreticians, Harry Markowitz and William Sharpe, who built beautifully Platonic models on a Gaussian base, contributing to what is called Modern Portfolio Theory. Simply, if you remove their Gaussian assumptions and treat prices as scalable, you are left with hot air. The Nobel Committee could have tested the Sharpe and Markowitz models – they work like quack remedies sold on the Internet – but nobody in Stockholm seems to have thought about it.

The MPT does not take its own effect on asset prices into account

Diversification eliminates non-systematic risk, but at the cost of increasing the systematic riskSystematic risk

In finance, systematic risk, sometimes called market risk, aggregate risk, or undiversifiable risk, is the risk associated with aggregate market returns....

. Diversification forces the portfolio manager to invest in assets without analyzing their fundamentals, solely for the benefit of eliminating the portfolio’s non-systematic risk (the CAPM assumes investment in all available assets). This artificially increased demand pushes up the price of assets that, when analyzed individually, would be of little fundamental value. The result is that the whole portfolio becomes more expensive and, as a result, the probability of a positive return decreases (i.e. the risk of the portfolio increases).

Empirical evidence for this is the price hike that stocks typically experience once they are included in major indices like the S&P 500

S&P 500

The S&P 500 is a free-float capitalization-weighted index published since 1957 of the prices of 500 large-cap common stocks actively traded in the United States. The stocks included in the S&P 500 are those of large publicly held companies that trade on either of the two largest American stock...

.

Extensions

Since MPT's introduction in 1952, many attempts have been made to improve the model, especially by using more realistic assumptions.Post-modern portfolio theory

Post-modern portfolio theory

Post-modern portfolio theory is an extension of the traditional modern portfolio theory...

extends MPT by adopting non-normally distributed, asymmetric measures of risk. This helps with some of these problems, but not others.

Black-Litterman model

Black-Litterman model

In Finance the Black–Litterman model is a mathematical model for portfolio allocation developed in 1990 at Goldman Sachs by Fischer Black and Robert Litterman, and published in 1992. It seeks to overcome problems that institutional investors have encountered in applying modern portfolio theory in...

optimization is an extension of unconstrained Markowitz optimization which incorporates relative and absolute `views' on inputs of risk and returns.

Applications to project portfolios and other "non-financial" assets

Some experts apply MPT to portfolios of projects and other assets besides financial instruments. When MPT is applied outside of traditional financial portfolios, some differences between the different types of portfolios must be considered.- The assets in financial portfolios are, for practical purposes, continuously divisible while portfolios of projects are "lumpy". For example, while we can compute that the optimal portfolio position for 3 stocks is, say, 44%, 35%, 21%, the optimal position for a project portfolio may not allow us to simply change the amount spent on a project. Projects might be all or nothing or, at least, have logical units that cannot be separated. A portfolio optimization method would have to take the discrete nature of projects into account.

- The assets of financial portfolios are liquid; they can be assessed or re-assessed at any point in time. But opportunities for launching new projects may be limited and may occur in limited windows of time. Projects that have already been initiated cannot be abandoned without the loss of the sunk costs (i.e., there is little or no recovery/salvage value of a half-complete project).

Neither of these necessarily eliminate the possibility of using MPT and such portfolios. They simply indicate the need to run the optimization with an additional set of mathematically-expressed constraints that would not normally apply to financial portfolios.

Furthermore, some of the simplest elements of Modern Portfolio Theory are applicable to virtually any kind of portfolio. The concept of capturing the risk tolerance of an investor by documenting how much risk is acceptable for a given return may be applied to a variety of decision analysis problems. MPT uses historical variance as a measure of risk, but portfolios of assets like major projects don't have a well-defined "historical variance". In this case, the MPT investment boundary can be expressed in more general terms like "chance of an ROI less than cost of capital" or "chance of losing more than half of the investment". When risk is put in terms of uncertainty about forecasts and possible losses then the concept is transferable to various types of investment.

Application to other disciplines

In the 1970s, concepts from Modern Portfolio Theory found their way into the field of regional scienceRegional science

Regional science is a field of the social sciences concerned with analytical approaches to problems that are specifically urban, rural, or regional...

. In a series of seminal works, Michael Conroy modeled the labor force in the economy using portfolio-theoretic methods to examine growth and variability in the labor force. This was followed by a long literature on the relationship between economic growth and volatility.

More recently, modern portfolio theory has been used to model the self-concept in social psychology. When the self attributes comprising the self-concept constitute a well-diversified portfolio, then psychological outcomes at the level of the individual such as mood and self-esteem should be more stable than when the self-concept is undiversified. This prediction has been confirmed in studies involving human subjects.

Recently, modern portfolio theory has been applied to modelling the uncertainty and correlation between documents in information retrieval. Given a query, the aim is to maximize the overall relevance of a ranked list of documents and at the same time minimize the overall uncertainty of the ranked list.

Comparison with arbitrage pricing theory

The SML and CAPM are often contrasted with the arbitrage pricing theoryArbitrage pricing theory

In finance, arbitrage pricing theory is a general theory of asset pricing that holds that the expected return of a financial asset can be modeled as a linear function of various macro-economic factors or theoretical market indices, where sensitivity to changes in each factor is represented by a...

(APT), which holds that the expected return

Expected return

The expected return is the weighted-average outcome in gambling, probability theory, economics or finance.It isthe average of a probability distribution of possible returns, calculated by using the following formula:...

of a financial asset can be modeled as a linear function

Linear function

In mathematics, the term linear function can refer to either of two different but related concepts:* a first-degree polynomial function of one variable;* a map between two vector spaces that preserves vector addition and scalar multiplication....

of various macro-economic

Macroeconomics

Macroeconomics is a branch of economics dealing with the performance, structure, behavior, and decision-making of the whole economy. This includes a national, regional, or global economy...

factors, where sensitivity to changes in each factor is represented by a factor specific beta coefficient

Beta coefficient

In finance, the Beta of a stock or portfolio is a number describing the relation of its returns with those of the financial market as a whole.An asset has a Beta of zero if its returns change independently of changes in the market's returns...

.

The APT is less restrictive in its assumptions: it allows for a statistical model of asset returns, and assumes that each investor will hold a unique portfolio with its own particular array of betas, as opposed to the identical "market portfolio". Unlike the CAPM, the APT, however, does not itself reveal the identity of its priced factors - the number and nature of these factors is likely to change over time and between economies.

See also

- Investment theoryInvestment theoryInvestment theory encompasses the body of knowledge used to support the decision-making process of choosing investments for various purposes. It includes portfolio theory, the Capital Asset Pricing Model, Arbitrage Pricing Theory, and the Efficient market hypothesis.-References:*...

- Treynor ratioTreynor ratioThe Treynor ratio , named after Jack L. Treynor, is a measurement of the returns earned in excess of that which could have been earned on an investment that has no diversifiable risk , per each unit of market risk assumed.The Treynor ratio relates...

- Jensen's alphaJensen's alphaIn finance, Jensen's alpha is used to determine the abnormal return of a security or portfolio of securities over the theoretical expected return....

- Sortino ratioSortino ratioThe Sortino ratio measures the risk-adjusted return of an investment asset, portfolio or strategy. It is a modification of the Sharpe ratio but penalizes only those returns falling below a user-specified target, or required rate of return, while the Sharpe ratio penalizes both upside and downside...

- Bias ratio (finance)Bias ratio (finance)The bias ratio is an indicator used in finance to analyze the returns of investment portfolios, and in performing due diligence.The bias ratio is a concrete metric that detects valuation bias or deliberate price manipulation of portfolio assets by a manager of a hedge fund, mutual fund or similar...

- Black-Litterman modelBlack-Litterman modelIn Finance the Black–Litterman model is a mathematical model for portfolio allocation developed in 1990 at Goldman Sachs by Fischer Black and Robert Litterman, and published in 1992. It seeks to overcome problems that institutional investors have encountered in applying modern portfolio theory in...

- Roll's critique

- Value investingValue investingValue investing is an investment paradigm that derives from the ideas on investment and speculation that Ben Graham and David Dodd began teaching at Columbia Business School in 1928 and subsequently developed in their 1934 text Security Analysis...

- Two-moment decision modelsTwo-moment decision modelsIn decision theory, economics, and finance, a two-moment decision model is a model that describes or prescribes the process of making decisions in a context in which the decision-maker is faced with random variables whose realizations cannot be known in advance, and in which choices are made based...

- Fundamental analysisFundamental analysisFundamental analysis of a business involves analyzing its financial statements and health, its management and competitive advantages, and its competitors and markets. When applied to futures and forex, it focuses on the overall state of the economy, interest rates, production, earnings, and...

- Marginal conditional stochastic dominanceMarginal conditional stochastic dominanceIn finance, marginal conditional stochastic dominance is a condition under which a portfolio can be improved in the eyes of all risk-averse investors by incrementally moving funds out of one asset and into another...

External links

- Macro-Investment Analysis, Prof. William F. SharpeWilliam Forsyth SharpeWilliam Forsyth Sharpe is the STANCO 25 Professor of Finance, Emeritus at Stanford University's Graduate School of Business and the winner of the 1990 Nobel Memorial Prize in Economic Sciences....

, Stanford - An Introduction to Investment Theory, Prof. William N. Goetzmann, Yale School of ManagementYale School of ManagementThe Yale School of Management is the graduate business school of Yale University and is located on Hillhouse Avenue in New Haven, Connecticut, United States. The School offers Master of Business Administration and Ph.D. degree programs. As of January 2011, 454 students were enrolled in its MBA...

- Free Stock Portfolio Optimization Online Allows users to compare stock performance, make free stock analysis, and optimize stock portfolio.

- Free Web Based Tool For Portfolio Optimization Optimize portfolios with constraints (e.g. no short selling), track portfolio performance and carry out sensitivity analyses. Detailed graphical reporting.