Gramm-Leach-Bliley Act

Encyclopedia

The Gramm–Leach–Bliley Act (GLB), also known as the Financial Services Modernization Act of 1999, is an act

of the 106th United States Congress

(1999–2001). It repealed part of the Glass–Steagall Act of 1933, removing barriers in the market among bank

ing companies, securities

companies and insurance

companies that prohibited any one institution from acting as any combination of an investment bank, a commercial bank

, and an insurance company. With the passage of the Gramm–Leach–Bliley Act, commercial banks, investment banks, securities firms, and insurance companies were allowed to consolidate. The legislation was signed into law by President Bill Clinton

.

A year before the law was passed, Citicorp, a commercial bank holding company

, merged with the insurance company Travelers Group in 1998 to form the conglomerate Citigroup

, a corporation combining banking, securities and insurance services under a house of brands that included Citibank

, Smith Barney

, Primerica, and Travelers. Because this merger was a violation of the Glass–Steagall Act and the Bank Holding Company Act of 1956, the Federal Reserve gave Citigroup a temporary waiver in September 1998. Less than a year later, GLB was passed to legalize these types of mergers on a permanent basis. The law also repealed Glass–Steagall's conflict of interest prohibitions "against simultaneous service by any officer, director, or employee of a securities firm as an officer, director, or employee of any member bank."

The banking industry had been seeking the repeal of the 1933 Glass–Steagall Act since the 1980s, if not earlier. In 1987 the Congressional Research Service

The banking industry had been seeking the repeal of the 1933 Glass–Steagall Act since the 1980s, if not earlier. In 1987 the Congressional Research Service

prepared a report that explored the cases for and against preserving the Glass–Steagall act.

Respective versions of the legislation were introduced in the U.S. Senate by Phil Gramm

(Republican

of Texas) and in the U.S. House of Representatives by Jim Leach

(R-Iowa). The third lawmaker associated with the bill was Rep. Thomas J. Bliley, Jr.

(R-Virginia), Chairman of the House Commerce Committee from 1995 to 2001.

During debate in the House of Representatives, Rep. John Dingell

(Democrat

of Michigan) argued that the bill would result in banks becoming "too big to fail." Dingell further argued that this would necessarily result in a bailout by the Federal Government.

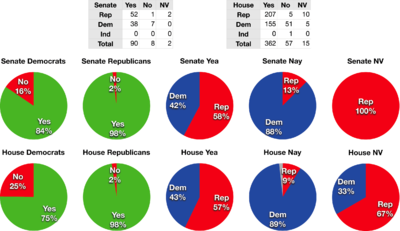

The House passed its version of the Financial Services Act of 1999 on July 1, 1999, by a bipartisan vote of 343-86 (Republicans 205–16; Democrats 138–69; Independent

0–1), two months after the Senate had already passed its version of the bill on May 6 by a much-narrower 54–44 vote along basically-partisan lines (53 Republicans and 1 Democrat in favor; 44 Democrats opposed).Sen. Fritz Hollings (D-S. Carolina) voted in favor, Sen. Peter Fitzgerald (R-Illinois) voted "present" and Sen. James Inhofe (R-Oklahoma) did not vote. A table with members' full names, sortable by vote, state, region and party, may be found at S.900 as amended: Gramm-Leach-Bliley Act, roll call 105, 106th Congress, 1st session. Votes Database at The Washington Post

. Retrieved on 2008-10-09 from http://projects.washingtonpost.com/congress/106/senate/1/votes/105/.

When the two chambers could not agree on a joint version of the bill, the House voted on July 30 by a vote of 241-132 (R 58-131; D 182-1; Ind. 1–0) to instruct its negotiators to work for a law which ensured that consumers enjoyed medical and financial privacy as well as "robust competition and equal and non-discriminatory access to financial services and economic opportunities in their communities" (i.e., protection against exclusionary redlining

).

The bill then moved to a joint conference committee to work out the differences between the Senate and House versions. Democrats agreed to support the bill after Republicans agreed to strengthen provisions of the anti-redlining Community Reinvestment Act

and address certain privacy concerns; the conference committee then finished its work by the beginning of November. On November 4, the final bill resolving the differences was passed by the Senate 90-8,52 Republicans and 38 Democrats voted for the bill. Sen. Richard Shelby

of Alabama (Republican, formerly a Democrat) voted against it, as did 7 Democratic Senators: Barbara Boxer

(Calif.), Richard Bryan

(Nevada), Byron Dorgan

(N. Dakota), Russell Feingold (Wisc.), Tom Harkin

(Iowa), Barbara Mikulski

(Maryland) and Paul Wellstone

(Minn.) Sen. Peter Fitzgerald (R-Illinois) again voted "present", while Sen. John McCain

(R-Arizona) did not vote. and by the House 362-57.Republicans voted 207-5 in favor with 10 not voting. Democrats voted 155-51 in favor, with 5 not voting. Independent-Socialist Rep. Bernard Sanders of Vermont voted no. The legislation was signed into law by President Bill Clinton

on November 12, 1999.

s when the economy turns bad. With the new Act, they would be able to do both 'savings' and 'investment' at the same financial institution, which would be able to do well in both good and bad economic times.

Prior to the Act, most financial services companies were already offering both saving and investment opportunities to their customers. On the retail/consumer side, a bank called Norwest

which would later merge with Wells Fargo Bank led the charge in offering all types of financial services products in 1986. American Express

attempted to own almost every field of financial business (although there was little synergy among them). Things culminated in 1998 when Citibank merged with Travelers Insurance creating CitiGroup. The merger violated the Bank Holding Company Act (BHCA), but Citibank was given a two-year forbearance that was based on an assumption that they would be able to force a change in the law. The Gramm–Leach–Bliley Act passed in November 1999, repealing portions of the BHCA and the Glass–Steagall Act, allowing banks, brokerages, and insurance companies to merge, thus making the CitiCorp/Travelers Group merger legal.

Also prior to the passage of the Act, there were many relaxations to the Glass–Steagall Act. For example, a few years earlier, commercial Banks were allowed to pursue investment banking, and before that banks were also allowed to begin stock and insurance brokerage. Insurance underwriting was the only main operation they weren't allowed to do, something rarely done by banks even after the passage of the Act.

Much consolidation occurred in the financial services industry since, but not at the scale some had expected. Retail banks, for example, do not tend to buy insurance underwriters, as they seek to engage in a more profitable business of insurance brokerage by selling products of other insurance companies. Other retail banks were slow to market investments and insurance products and package those products in a convincing way. Brokerage companies had a hard time getting into banking, because they do not have a large branch and backshop footprint. Banks have recently tended to buy other banks, such as the 2004 Bank of America

and Fleet Boston merger, yet they have had less success integrating with investment and insurance companies. Many banks have expanded into investment banking

, but have found it hard to package it with their banking services, without resorting to questionable tie-ins which caused scandals at Smith Barney

.

(CRA). This was an issue of hot contention, and the Clinton Administration stressed that it "would veto any legislation that would scale back minority-lending requirements."

The GLB also did not remove the restrictions on banks placed by the Bank Holding Company Act of 1956

which prevented financial institutions from owning non-financial corporations. It conversely prohibits corporations outside of the banking or finance industry from entering retail and/or commercial banking. Many assume Wal-Mart

's desire to convert its industrial bank to a commercial/retail bank ultimately drove the banking industry to back the GLB restrictions.

Some restrictions remain to provide some amount of separation between the investment and commercial banking operations of a company. For example, licensed

bankers must have separate business cards, e.g., "Personal Banker, Wells Fargo Bank" and "Investment Consultant, Wells Fargo Private Client Services". Much of the debate about financial privacy

is specifically centered around allowing or preventing the banking, brokerage, and insurances divisions of a company from working together.

In terms of compliance

, the key rules under the Act include The Financial Privacy Rule which governs the collection and disclosure of customers’ personal financial information by financial institutions. It also applies to companies, regardless of whether they are financial institutions, who receive such information. The Safeguards Rule requires all financial institutions to design, implement and maintain safeguards to protect customer information. The Safeguards Rule applies not only to financial institutions that collect information from their own customers, but also to financial institutions – such as credit reporting agencies, appraisers, and mortgage brokers – that receive customer information from other financial institutions.

The Financial Privacy Rule requires financial institutions to provide each consumer with a privacy notice at the time the consumer relationship is established and annually thereafter. The privacy notice must explain the information collected about the consumer, where that information is shared, how that information is used, and how that information is protected. The notice must also identify the consumer’s right to opt out of the information being shared with unaffiliated parties pursuant to the provisions of the Fair Credit Reporting Act

. Should the privacy policy change at any point in time, the consumer must be notified again for acceptance. Each time the privacy notice is reestablished, the consumer has the right to opt out again. The unaffiliated parties receiving the nonpublic information are held to the acceptance terms of the consumer under the original relationship agreement. In summary, the financial privacy rule provides for a privacy policy

agreement between the company and the consumer pertaining to the protection of the consumer’s personal nonpublic information.

On November 17, 2009, eight federal regulatory agencies released the final version of a model privacy notice form to make it easier for consumers to understand how financial institutions collect and share information about consumers.

(FTC) has jurisdiction over financial institutions similar to, and including, these:

These companies must also be considered significantly engaged in the financial service or production that defines them as a "financial institution".

Insurance has jurisdiction first by the state, provided the state law at minimum complies with the GLB. State law can require greater compliance, but not less than what is otherwise required by the GLB.

A ‘customer’ is a consumer that has developed a relationship with privacy rights protected under the GLB. A ‘customer’ is not someone using an automated teller machine (ATM) or having a check cashed at a cash advance business. These are not ongoing relationships like a ‘consumer’ might have; i.e., a mortgage loan

, tax advising, or credit financing. A business is not an individual with personal nonpublic information, so a business cannot be a customer under the GLB. A business, however, may be liable for compliance to the GLB depending upon the type of business and the activities utilizing individual’s personal nonpublic information.

The privacy notice must also explain to the customer the opportunity to ‘opt-out’. Opting out means that the client can say "no" to allowing their information to be shared with affiliated parties. The Fair Credit Reporting Act

is responsible for the ‘opt-out’ opportunity, but the privacy notice must inform the customer of this right under the GLB. The client cannot opt-out of:

The Safeguards Rule requires financial institutions to develop a written information security plan that describes how the company is prepared for, and plans to continue to protect clients’ nonpublic personal information. (The Safeguards Rule applies to information of any consumers past or present of the financial institution's products or services.) This plan must include:

This rule is intended to do what most businesses should already be doing: protecting their clients. The Safeguards Rule forces financial institutions to take a closer look at how they manage private data and to do a risk analysis on their current processes. No process is perfect, so this has meant that every financial institution has had to make some effort to comply with the GLB.

Pretexting (sometimes referred to as "social engineering") occurs when someone tries to gain access to personal nonpublic information without proper authority to do so. This may entail requesting private information while impersonating the account holder, by phone, by mail, by email, or even by "phishing

" (i.e., using a phony website or email to collect data). The GLB encourages the organizations covered by the GLB to implement safeguards against pretexting. For example, a well-written plan designed to meet GLB's Safeguards Rule ("develop, monitor, and test a program to secure the information") would likely include a section on training employees to recognize and deflect inquiries made under pretext. In fact, the evaluation of the effectiveness of such employee training probably should include a follow-up program of random spot-checks, "outside the classroom", after completion of the [initial] employee training, in order to check on the resistance of a given (randomly chosen) student to various types of "social engineering" -- perhaps even designed to focus attention on any new wrinkle that might have arisen after the [initial] effort to "develop" the curriculum for such employee training. Under United States

law, pretexting by individuals is punishable as a common law

crime of False Pretenses

.

, whose usury

limit was set at five percent above the Federal Reserve discount rate

by the Arkansas Constitution

and could not be changed by the Arkansas General Assembly

. When the Office of the Comptroller of the Currency

ruled that interstate banks established under the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

could use their home state's usury law for all branches nationwide with minimal restrictions, Arkansas-based banks were placed at a severe competitive disadvantage to Arkansas branches of interstate banks; this led to out-of-state takeovers of several Arkansas banks, including the sale of First Commercial Bank (then Arkansas' largest bank) to Regions Financial Corporation in 1998.

Under Section 731, all banks headquartered in a state covered by that law may charge up to the highest usury limit of any state that is headquarters to an interstate bank which has branches in the covered state. Therefore, since Arkansas has branches of banks based in Alabama

, Georgia

, Mississippi

, Missouri

, North Carolina

, Ohio

and Texas

, any loan that is legal under the usury laws of any of those states may be made by an Arkansas-based bank under Section 731. The section does not apply to interstate banks with branches in the covered state, but headquartered elsewhere; however, Arkansas-based interstate banks like Arvest Bank

may export their Section 731 limits to other states.

Due to Section 731, it is generally regarded that Arkansas-based banks now have no usury limit for credit card

s or for any loan of greater than $2,000 (since Alabama, Regions' home state, has no limits on those loans), with a limit of 18% (the minimum usury limit in Texas) or more on all other loans. However, once Wells Fargo

fully completes its proposed purchase of Century Bank

(a Texas bank with Arkansas branches), Section 731 will do away with all usury limits for Arkansas-based banks since Wells Fargo's main bank charter is based in South Dakota

, which repealed its usury laws many years ago.

Though designed for Arkansas, Section 731 may also apply to Alaska

and California

whose constitutions provide for the same basic usury limit, though unlike Arkansas their legislatures can (and generally do) set different limits. If Section 731 applies to those states, then all their usury limits are inapplicable to banks based in those states, since Wells Fargo has branches in both states.

and Mark Thornton

have also criticized the Act as contributing to the crisis. They state that "in a world regulated by a gold standard

, 100% reserve banking, and no FDIC

deposit insurance" the Financial Services Modernization Act would have made "perfect sense" as a legitimate act of deregulation, but under the present fiat monetary system

it "amounts to corporate welfare

for financial institutions and a moral hazard

that will make taxpayers pay dearly."

Nobel Prize

-winning economist

Joseph Stiglitz has also argued that the Act helped to create the crisis. An article in the liberal publication The Nation

asserted that GLB was responsible for the creation of entities that took on more risk due to their being considered “too big to fail

."

authored by one of the institute's directors, Mark A. Calabria

, critics of the legislation feared that, with the allowance for mergers between investment and commercial banks, GLB allowed the newly-merged banks to take on riskier investments while at the same time removing any requirements to maintain enough equity, exposing the assets of its banking customers. Calabria claimed that, prior to the passage of GLB in 1999, investment banks were already capable of holding and trading the very financial assets claimed to be the cause of the mortgage crisis, and were also already able to keep their books as they had. He concluded that greater access to investment capital as many investment banks went public on the market explains the shift in their holdings to trading portfolios. Calabria noted that after GLB passed, most investment banks did not merge with depository commercial banks, and that in fact, the few banks that did merge weathered the crisis better than those that did not.

In February 2009, one of the act's co-authors, former Senator Phil Gramm, also defended his bill:

Bill Clinton

, as well as economists Brad DeLong and Tyler Cowen

have all argued that the Gramm–Leach–Bliley Act softened the impact of the crisis.

Atlantic Monthly columnist Megan McArdle

has argued that if the act was "part of the problem, it would be the commercial banks, not the investment banks, that were in trouble" and repeal would not have helped the situation. An article in the conservative publication, National Review

, has made the same argument, calling liberal allegations about the Act “folk economics

.”

Act of Congress

An Act of Congress is a statute enacted by government with a legislature named "Congress," such as the United States Congress or the Congress of the Philippines....

of the 106th United States Congress

106th United States Congress

The One Hundred Sixth United States Congress was a meeting of the legislative branch of the United States federal government, composed of the United States Senate and the United States House of Representatives. It met in Washington, DC from January 3, 1999 to January 3, 2001, during the last two...

(1999–2001). It repealed part of the Glass–Steagall Act of 1933, removing barriers in the market among bank

Bank

A bank is a financial institution that serves as a financial intermediary. The term "bank" may refer to one of several related types of entities:...

ing companies, securities

Security (finance)

A security is generally a fungible, negotiable financial instrument representing financial value. Securities are broadly categorized into:* debt securities ,* equity securities, e.g., common stocks; and,...

companies and insurance

Insurance

In law and economics, insurance is a form of risk management primarily used to hedge against the risk of a contingent, uncertain loss. Insurance is defined as the equitable transfer of the risk of a loss, from one entity to another, in exchange for payment. An insurer is a company selling the...

companies that prohibited any one institution from acting as any combination of an investment bank, a commercial bank

Commercial bank

After the implementation of the Glass–Steagall Act, the U.S. Congress required that banks engage only in banking activities, whereas investment banks were limited to capital market activities. As the two no longer have to be under separate ownership under U.S...

, and an insurance company. With the passage of the Gramm–Leach–Bliley Act, commercial banks, investment banks, securities firms, and insurance companies were allowed to consolidate. The legislation was signed into law by President Bill Clinton

Bill Clinton

William Jefferson "Bill" Clinton is an American politician who served as the 42nd President of the United States from 1993 to 2001. Inaugurated at age 46, he was the third-youngest president. He took office at the end of the Cold War, and was the first president of the baby boomer generation...

.

A year before the law was passed, Citicorp, a commercial bank holding company

Holding company

A holding company is a company or firm that owns other companies' outstanding stock. It usually refers to a company which does not produce goods or services itself; rather, its purpose is to own shares of other companies. Holding companies allow the reduction of risk for the owners and can allow...

, merged with the insurance company Travelers Group in 1998 to form the conglomerate Citigroup

Citigroup

Citigroup Inc. or Citi is an American multinational financial services corporation headquartered in Manhattan, New York City, New York, United States. Citigroup was formed from one of the world's largest mergers in history by combining the banking giant Citicorp and financial conglomerate...

, a corporation combining banking, securities and insurance services under a house of brands that included Citibank

Citibank

Citibank, a major international bank, is the consumer banking arm of financial services giant Citigroup. Citibank was founded in 1812 as the City Bank of New York, later First National City Bank of New York...

, Smith Barney

Smith Barney

Morgan Stanley Smith Barney is a retail brokerage joint venture between Morgan Stanley and Citigroup.On January 13, 2009, Morgan Stanley and Citigroup announced that Citigroup would sell 51% of Smith Barney to Morgan Stanley, creating Morgan Stanley Smith Barney, which was formerly a division of...

, Primerica, and Travelers. Because this merger was a violation of the Glass–Steagall Act and the Bank Holding Company Act of 1956, the Federal Reserve gave Citigroup a temporary waiver in September 1998. Less than a year later, GLB was passed to legalize these types of mergers on a permanent basis. The law also repealed Glass–Steagall's conflict of interest prohibitions "against simultaneous service by any officer, director, or employee of a securities firm as an officer, director, or employee of any member bank."

Legislative history

Congressional Research Service

The Congressional Research Service , known as "Congress's think tank", is the public policy research arm of the United States Congress. As a legislative branch agency within the Library of Congress, CRS works exclusively and directly for Members of Congress, their Committees and staff on a...

prepared a report that explored the cases for and against preserving the Glass–Steagall act.

Respective versions of the legislation were introduced in the U.S. Senate by Phil Gramm

Phil Gramm

William Philip "Phil" Gramm is an American economist and politician, who has served as a Democratic Congressman , a Republican Congressman and a Republican Senator from Texas...

(Republican

Republican Party (United States)

The Republican Party is one of the two major contemporary political parties in the United States, along with the Democratic Party. Founded by anti-slavery expansion activists in 1854, it is often called the GOP . The party's platform generally reflects American conservatism in the U.S...

of Texas) and in the U.S. House of Representatives by Jim Leach

Jim Leach

James Albert Smith "Jim" Leach is a former member of the U.S. House of Representatives from Iowa. In August 2009, he became Chairman of the National Endowment for the Humanities ....

(R-Iowa). The third lawmaker associated with the bill was Rep. Thomas J. Bliley, Jr.

Thomas J. Bliley, Jr.

Thomas Jerome "Tom" Bliley, Jr. is a United States Republican politician and former U.S. Representative from the state of Virginia.-Background:...

(R-Virginia), Chairman of the House Commerce Committee from 1995 to 2001.

During debate in the House of Representatives, Rep. John Dingell

John Dingell

John David Dingell, Jr. is the U.S. Representative for , serving since 1955 . He is a member of the Democratic Party...

(Democrat

Democratic Party (United States)

The Democratic Party is one of two major contemporary political parties in the United States, along with the Republican Party. The party's socially liberal and progressive platform is largely considered center-left in the U.S. political spectrum. The party has the lengthiest record of continuous...

of Michigan) argued that the bill would result in banks becoming "too big to fail." Dingell further argued that this would necessarily result in a bailout by the Federal Government.

The House passed its version of the Financial Services Act of 1999 on July 1, 1999, by a bipartisan vote of 343-86 (Republicans 205–16; Democrats 138–69; Independent

Bernie Sanders

Bernard "Bernie" Sanders is the junior United States Senator from Vermont. He previously represented Vermont's at-large district in the United States House of Representatives...

0–1), two months after the Senate had already passed its version of the bill on May 6 by a much-narrower 54–44 vote along basically-partisan lines (53 Republicans and 1 Democrat in favor; 44 Democrats opposed).Sen. Fritz Hollings (D-S. Carolina) voted in favor, Sen. Peter Fitzgerald (R-Illinois) voted "present" and Sen. James Inhofe (R-Oklahoma) did not vote. A table with members' full names, sortable by vote, state, region and party, may be found at S.900 as amended: Gramm-Leach-Bliley Act, roll call 105, 106th Congress, 1st session. Votes Database at The Washington Post

The Washington Post

The Washington Post is Washington, D.C.'s largest newspaper and its oldest still-existing paper, founded in 1877. Located in the capital of the United States, The Post has a particular emphasis on national politics. D.C., Maryland, and Virginia editions are printed for daily circulation...

. Retrieved on 2008-10-09 from http://projects.washingtonpost.com/congress/106/senate/1/votes/105/.

When the two chambers could not agree on a joint version of the bill, the House voted on July 30 by a vote of 241-132 (R 58-131; D 182-1; Ind. 1–0) to instruct its negotiators to work for a law which ensured that consumers enjoyed medical and financial privacy as well as "robust competition and equal and non-discriminatory access to financial services and economic opportunities in their communities" (i.e., protection against exclusionary redlining

Redlining

Redlining is the practice of denying, or increasing the cost of services such as banking, insurance, access to jobs, access to health care, or even supermarkets to residents in certain, often racially determined, areas. The term "redlining" was coined in the late 1960s by John McKnight, a...

).

The bill then moved to a joint conference committee to work out the differences between the Senate and House versions. Democrats agreed to support the bill after Republicans agreed to strengthen provisions of the anti-redlining Community Reinvestment Act

Community Reinvestment Act

The Community Reinvestment Act is a United States federal law designed to encourage commercial banks and savings associations to help meet the needs of borrowers in all segments of their communities, including low- and moderate-income neighborhoods...

and address certain privacy concerns; the conference committee then finished its work by the beginning of November. On November 4, the final bill resolving the differences was passed by the Senate 90-8,52 Republicans and 38 Democrats voted for the bill. Sen. Richard Shelby

Richard Shelby

Richard Craig Shelby is the senior U.S. Senator from Alabama. First elected to the Senate in 1986, he is the ranking member of the United States Senate Committee on Banking, Housing, and Urban Affairs and was its chairman from 2003 to 2007....

of Alabama (Republican, formerly a Democrat) voted against it, as did 7 Democratic Senators: Barbara Boxer

Barbara Boxer

Barbara Levy Boxer is the junior United States Senator from California . A member of the Democratic Party, she previously served in the U.S. House of Representatives ....

(Calif.), Richard Bryan

Richard Bryan

Richard Hudson "Dick" Bryan is an American politician. He served as the 25th Governor of the U.S. state of Nevada from 1983 to 1989. He is a former United States Senator from Nevada. He is a member of the Democratic Party.-Early life:...

(Nevada), Byron Dorgan

Byron Dorgan

Byron Leslie Dorgan is a former United States Senator from North Dakota and is now a senior policy advisor for a Washington, DC law firm. He is a member of the North Dakota Democratic-NPL Party, the North Dakota affiliate of the Democratic Party. In the Senate, he was Chairman of the Democratic...

(N. Dakota), Russell Feingold (Wisc.), Tom Harkin

Tom Harkin

Thomas Richard "Tom" Harkin is the junior United States Senator from Iowa and a member of the Democratic Party. He previously served in the United States House of Representatives ....

(Iowa), Barbara Mikulski

Barbara Mikulski

Barbara Ann Mikulski is the senior United States Senator from Maryland and a member of the Democratic Party. Mikulski, a former U.S. Representative, is the longest-serving female senator in U.S...

(Maryland) and Paul Wellstone

Paul Wellstone

Paul David Wellstone was a two-term U.S. Senator from the state of Minnesota and member of the Democratic-Farmer-Labor Party, which is affiliated with the national Democratic Party. Before being elected to the Senate in 1990, he was a professor of political science at Carleton College...

(Minn.) Sen. Peter Fitzgerald (R-Illinois) again voted "present", while Sen. John McCain

John McCain

John Sidney McCain III is the senior United States Senator from Arizona. He was the Republican nominee for president in the 2008 United States election....

(R-Arizona) did not vote. and by the House 362-57.Republicans voted 207-5 in favor with 10 not voting. Democrats voted 155-51 in favor, with 5 not voting. Independent-Socialist Rep. Bernard Sanders of Vermont voted no. The legislation was signed into law by President Bill Clinton

Bill Clinton

William Jefferson "Bill" Clinton is an American politician who served as the 42nd President of the United States from 1993 to 2001. Inaugurated at age 46, he was the third-youngest president. He took office at the end of the Cold War, and was the first president of the baby boomer generation...

on November 12, 1999.

Changes caused by the Act

Many of the largest banks, brokerages, and insurance companies desired the Act at the time. The justification was that individuals usually put more money into investments when the economy is doing well, but they put most of their money into savings accountSavings account

Savings accounts are accounts maintained by retail financial institutions that pay interest but cannot be used directly as money . These accounts let customers set aside a portion of their liquid assets while earning a monetary return...

s when the economy turns bad. With the new Act, they would be able to do both 'savings' and 'investment' at the same financial institution, which would be able to do well in both good and bad economic times.

Prior to the Act, most financial services companies were already offering both saving and investment opportunities to their customers. On the retail/consumer side, a bank called Norwest

Norwest

Norwest Corporation was a banking and financial services company based in Minneapolis, Minnesota, United States. In 1998, it merged with Wells Fargo & Co. and since that time has traded under the Wells Fargo name.-Early formation:...

which would later merge with Wells Fargo Bank led the charge in offering all types of financial services products in 1986. American Express

American Express

American Express Company or AmEx, is an American multinational financial services corporation headquartered in Three World Financial Center, Manhattan, New York City, New York, United States. Founded in 1850, it is one of the 30 components of the Dow Jones Industrial Average. The company is best...

attempted to own almost every field of financial business (although there was little synergy among them). Things culminated in 1998 when Citibank merged with Travelers Insurance creating CitiGroup. The merger violated the Bank Holding Company Act (BHCA), but Citibank was given a two-year forbearance that was based on an assumption that they would be able to force a change in the law. The Gramm–Leach–Bliley Act passed in November 1999, repealing portions of the BHCA and the Glass–Steagall Act, allowing banks, brokerages, and insurance companies to merge, thus making the CitiCorp/Travelers Group merger legal.

Also prior to the passage of the Act, there were many relaxations to the Glass–Steagall Act. For example, a few years earlier, commercial Banks were allowed to pursue investment banking, and before that banks were also allowed to begin stock and insurance brokerage. Insurance underwriting was the only main operation they weren't allowed to do, something rarely done by banks even after the passage of the Act.

Much consolidation occurred in the financial services industry since, but not at the scale some had expected. Retail banks, for example, do not tend to buy insurance underwriters, as they seek to engage in a more profitable business of insurance brokerage by selling products of other insurance companies. Other retail banks were slow to market investments and insurance products and package those products in a convincing way. Brokerage companies had a hard time getting into banking, because they do not have a large branch and backshop footprint. Banks have recently tended to buy other banks, such as the 2004 Bank of America

Bank of America

Bank of America Corporation, an American multinational banking and financial services corporation, is the second largest bank holding company in the United States by assets, and the fourth largest bank in the U.S. by market capitalization. The bank is headquartered in Charlotte, North Carolina...

and Fleet Boston merger, yet they have had less success integrating with investment and insurance companies. Many banks have expanded into investment banking

Investment banking

An investment bank is a financial institution that assists individuals, corporations and governments in raising capital by underwriting and/or acting as the client's agent in the issuance of securities...

, but have found it hard to package it with their banking services, without resorting to questionable tie-ins which caused scandals at Smith Barney

Smith Barney

Morgan Stanley Smith Barney is a retail brokerage joint venture between Morgan Stanley and Citigroup.On January 13, 2009, Morgan Stanley and Citigroup announced that Citigroup would sell 51% of Smith Barney to Morgan Stanley, creating Morgan Stanley Smith Barney, which was formerly a division of...

.

Remaining restrictions

Crucial to the passing of this Act was an amendment made to the GLB, stating that no merger may go ahead if any of the financial holding institutions, or affiliates thereof, received a "less than satisfactory [sic] rating at its most recent CRA exam", essentially meaning that any merger may only go ahead with the strict approval of the regulatory bodies responsible for the Community Reinvestment ActCommunity Reinvestment Act

The Community Reinvestment Act is a United States federal law designed to encourage commercial banks and savings associations to help meet the needs of borrowers in all segments of their communities, including low- and moderate-income neighborhoods...

(CRA). This was an issue of hot contention, and the Clinton Administration stressed that it "would veto any legislation that would scale back minority-lending requirements."

The GLB also did not remove the restrictions on banks placed by the Bank Holding Company Act of 1956

Bank Holding Company Act of 1956

The Bank Holding Company Act of 1956 is a United States Act of Congress that regulates the actions of bank holding companies.The original law , specified that the Federal Reserve Board of Governors must approve the establishment of a bank holding company, and prohibited bank holding companies...

which prevented financial institutions from owning non-financial corporations. It conversely prohibits corporations outside of the banking or finance industry from entering retail and/or commercial banking. Many assume Wal-Mart

Wal-Mart

Wal-Mart Stores, Inc. , branded as Walmart since 2008 and Wal-Mart before then, is an American public multinational corporation that runs chains of large discount department stores and warehouse stores. The company is the world's 18th largest public corporation, according to the Forbes Global 2000...

's desire to convert its industrial bank to a commercial/retail bank ultimately drove the banking industry to back the GLB restrictions.

Some restrictions remain to provide some amount of separation between the investment and commercial banking operations of a company. For example, licensed

General Securities Representative Exam

The General Securities Representative Exam, commonly referred to as the Series 7 Exam, is a required exam to become a Registered Representative of a broker-dealer in the United States....

bankers must have separate business cards, e.g., "Personal Banker, Wells Fargo Bank" and "Investment Consultant, Wells Fargo Private Client Services". Much of the debate about financial privacy

Financial privacy

Financial Privacy is a blanket term for a multitude of privacy issues:*Financial Institutions ensuring that their customers information remains private to those outside the institution. Issues include the Patriot Act, and other debates of privacy vs...

is specifically centered around allowing or preventing the banking, brokerage, and insurances divisions of a company from working together.

In terms of compliance

Compliance (regulation)

In general, compliance means conforming to a rule, such as a specification, policy, standard or law. Regulatory compliance describes the goal that corporations or public agencies aspire to in their efforts to ensure that personnel are aware of and take steps to comply with relevant laws and...

, the key rules under the Act include The Financial Privacy Rule which governs the collection and disclosure of customers’ personal financial information by financial institutions. It also applies to companies, regardless of whether they are financial institutions, who receive such information. The Safeguards Rule requires all financial institutions to design, implement and maintain safeguards to protect customer information. The Safeguards Rule applies not only to financial institutions that collect information from their own customers, but also to financial institutions – such as credit reporting agencies, appraisers, and mortgage brokers – that receive customer information from other financial institutions.

Privacy

- GLB compliance is mandatory; whether a financial institution discloses nonpublic information or not, there must be a policy in place to protect the information from foreseeable threats in security and data integrity.

- Major components put into place to govern the collection, disclosure, and protection of consumers’ nonpublic personal information; or personally identifiable information include:

- Financial Privacy Rule

- Safeguards Rule

- Pretexting Protection

Financial Privacy Rule

(Subtitle A: Disclosure of Nonpublic Personal Information, codified at )The Financial Privacy Rule requires financial institutions to provide each consumer with a privacy notice at the time the consumer relationship is established and annually thereafter. The privacy notice must explain the information collected about the consumer, where that information is shared, how that information is used, and how that information is protected. The notice must also identify the consumer’s right to opt out of the information being shared with unaffiliated parties pursuant to the provisions of the Fair Credit Reporting Act

Fair Credit Reporting Act

The Fair Credit Reporting Act is a United States federal law that regulates the collection, dissemination, and use of consumer information, including consumer credit information. Along with the Fair Debt Collection Practices Act , it forms the base of consumer credit rights in the United States...

. Should the privacy policy change at any point in time, the consumer must be notified again for acceptance. Each time the privacy notice is reestablished, the consumer has the right to opt out again. The unaffiliated parties receiving the nonpublic information are held to the acceptance terms of the consumer under the original relationship agreement. In summary, the financial privacy rule provides for a privacy policy

Privacy policy

Privacy policy is a statement or a legal document that discloses some or all of the ways a party gathers, uses, discloses and manages a customer or client's data...

agreement between the company and the consumer pertaining to the protection of the consumer’s personal nonpublic information.

On November 17, 2009, eight federal regulatory agencies released the final version of a model privacy notice form to make it easier for consumers to understand how financial institutions collect and share information about consumers.

Financial institutions defined

The GLB defines "financial institutions" as: "…companies that offer financial products or services to individuals, like loans, financial or investment advice, or insurance." The Federal Trade CommissionFederal Trade Commission

The Federal Trade Commission is an independent agency of the United States government, established in 1914 by the Federal Trade Commission Act...

(FTC) has jurisdiction over financial institutions similar to, and including, these:

- non-bank mortgage lenders,

- real estate appraisers,

- loan brokers,

- some financial or investment advisers,

- debt collectors,

- tax return preparers,

- banks, and

- real estate settlement service providers.

These companies must also be considered significantly engaged in the financial service or production that defines them as a "financial institution".

Insurance has jurisdiction first by the state, provided the state law at minimum complies with the GLB. State law can require greater compliance, but not less than what is otherwise required by the GLB.

Consumer vs. customer defined

The Gramm–Leach–Bliley Act defines a ‘consumer’ as- "an individual who obtains, from a financial institution, financial products or services which are to be used primarily for personal, family, or household purposes, and also means the legal representative of such an individual." (See .}

A ‘customer’ is a consumer that has developed a relationship with privacy rights protected under the GLB. A ‘customer’ is not someone using an automated teller machine (ATM) or having a check cashed at a cash advance business. These are not ongoing relationships like a ‘consumer’ might have; i.e., a mortgage loan

Mortgage loan

A mortgage loan is a loan secured by real property through the use of a mortgage note which evidences the existence of the loan and the encumbrance of that realty through the granting of a mortgage which secures the loan...

, tax advising, or credit financing. A business is not an individual with personal nonpublic information, so a business cannot be a customer under the GLB. A business, however, may be liable for compliance to the GLB depending upon the type of business and the activities utilizing individual’s personal nonpublic information.

Consumer/client privacy rights

Under the GLB, financial institutions must provide their clients a privacy notice that explains what information the company gathers about the client, where this information is shared, and how the company safeguards that information. This privacy notice must be given to the client prior to entering into an agreement to do business. There are exceptions to this when the client accepts a delayed receipt of the notice in order to complete a transaction on a timely basis. This has been somewhat mitigated due to online acknowledgement agreements requiring the client to read or scroll through the notice and check a box to accept terms.The privacy notice must also explain to the customer the opportunity to ‘opt-out’. Opting out means that the client can say "no" to allowing their information to be shared with affiliated parties. The Fair Credit Reporting Act

Fair Credit Reporting Act

The Fair Credit Reporting Act is a United States federal law that regulates the collection, dissemination, and use of consumer information, including consumer credit information. Along with the Fair Debt Collection Practices Act , it forms the base of consumer credit rights in the United States...

is responsible for the ‘opt-out’ opportunity, but the privacy notice must inform the customer of this right under the GLB. The client cannot opt-out of:

- information shared with those providing priority service to the financial institution

- marketing of products or services for the financial institution

- when the information is deemed legally required.

Safeguards Rule

(Subtitle A: Disclosure of Nonpublic Personal Information, codified at )The Safeguards Rule requires financial institutions to develop a written information security plan that describes how the company is prepared for, and plans to continue to protect clients’ nonpublic personal information. (The Safeguards Rule applies to information of any consumers past or present of the financial institution's products or services.) This plan must include:

- Denoting at least one employee to manage the safeguards,

- Constructing a thorough risk managementRisk managementRisk management is the identification, assessment, and prioritization of risks followed by coordinated and economical application of resources to minimize, monitor, and control the probability and/or impact of unfortunate events or to maximize the realization of opportunities...

on each department handling the nonpublic information, - Develop, monitor, and test a program to secure the information, and

- Change the safeguards as needed with the changes in how information is collected, stored, and used.

This rule is intended to do what most businesses should already be doing: protecting their clients. The Safeguards Rule forces financial institutions to take a closer look at how they manage private data and to do a risk analysis on their current processes. No process is perfect, so this has meant that every financial institution has had to make some effort to comply with the GLB.

Pretexting protection

(Subtitle B: Fraudulent Access to Financial Information, codified at )Pretexting (sometimes referred to as "social engineering") occurs when someone tries to gain access to personal nonpublic information without proper authority to do so. This may entail requesting private information while impersonating the account holder, by phone, by mail, by email, or even by "phishing

Phishing

Phishing is a way of attempting to acquire information such as usernames, passwords, and credit card details by masquerading as a trustworthy entity in an electronic communication. Communications purporting to be from popular social web sites, auction sites, online payment processors or IT...

" (i.e., using a phony website or email to collect data). The GLB encourages the organizations covered by the GLB to implement safeguards against pretexting. For example, a well-written plan designed to meet GLB's Safeguards Rule ("develop, monitor, and test a program to secure the information") would likely include a section on training employees to recognize and deflect inquiries made under pretext. In fact, the evaluation of the effectiveness of such employee training probably should include a follow-up program of random spot-checks, "outside the classroom", after completion of the [initial] employee training, in order to check on the resistance of a given (randomly chosen) student to various types of "social engineering" -- perhaps even designed to focus attention on any new wrinkle that might have arisen after the [initial] effort to "develop" the curriculum for such employee training. Under United States

United States

The United States of America is a federal constitutional republic comprising fifty states and a federal district...

law, pretexting by individuals is punishable as a common law

Common law

Common law is law developed by judges through decisions of courts and similar tribunals rather than through legislative statutes or executive branch action...

crime of False Pretenses

False pretenses

Obtaining property by false pretenses is when a person obtains property by intentionally misrepresenting a past or existing fact.-Elements:The elements of false pretenses are: a false representation of a material past or existing fact...

.

Effect on usury law in Arkansas & other states

Section 731 of the GLB, codified as subsection (f) of , contains a unique provision aimed at ArkansasArkansas

Arkansas is a state located in the southern region of the United States. Its name is an Algonquian name of the Quapaw Indians. Arkansas shares borders with six states , and its eastern border is largely defined by the Mississippi River...

, whose usury

Usury

Usury Originally, when the charging of interest was still banned by Christian churches, usury simply meant the charging of interest at any rate . In countries where the charging of interest became acceptable, the term came to be used for interest above the rate allowed by law...

limit was set at five percent above the Federal Reserve discount rate

Discount window

The discount window is an instrument of monetary policy that allows eligible institutions to borrow money from the central bank, usually on a short-term basis, to meet temporary shortages of liquidity caused by internal or external disruptions...

by the Arkansas Constitution

Arkansas Constitution

The Constitution of the State of Arkansas is the governing document of the U.S. state of Arkansas. It was adopted in 1874, shortly after the Brooks-Baxter War replacing the 1868 constitution that had allowed Arkansas to rejoin the Union after the conclusion of the American Civil War; the new...

and could not be changed by the Arkansas General Assembly

Arkansas General Assembly

The Arkansas General Assembly is the state legislature of the U.S. state of Arkansas. The legislature is a bicameral body composed of the upper house Arkansas Senate with 35 members, and the lower Arkansas House of Representatives with 100 members. All 135 representatives and state senators...

. When the Office of the Comptroller of the Currency

Office of the Comptroller of the Currency

The Office of the Comptroller of the Currency is a US federal agency established by the National Currency Act of 1863 and serves to charter, regulate, and supervise all national banks and the federal branches and agencies of foreign banks in the United States...

ruled that interstate banks established under the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 [IBBEA] amended the laws governing federally-chartered banks in order to restore the laws' competitiveness with the recently relaxed laws governing state-chartered banks. The goal was the return to a balance between the...

could use their home state's usury law for all branches nationwide with minimal restrictions, Arkansas-based banks were placed at a severe competitive disadvantage to Arkansas branches of interstate banks; this led to out-of-state takeovers of several Arkansas banks, including the sale of First Commercial Bank (then Arkansas' largest bank) to Regions Financial Corporation in 1998.

Under Section 731, all banks headquartered in a state covered by that law may charge up to the highest usury limit of any state that is headquarters to an interstate bank which has branches in the covered state. Therefore, since Arkansas has branches of banks based in Alabama

Alabama

Alabama is a state located in the southeastern region of the United States. It is bordered by Tennessee to the north, Georgia to the east, Florida and the Gulf of Mexico to the south, and Mississippi to the west. Alabama ranks 30th in total land area and ranks second in the size of its inland...

, Georgia

Georgia (U.S. state)

Georgia is a state located in the southeastern United States. It was established in 1732, the last of the original Thirteen Colonies. The state is named after King George II of Great Britain. Georgia was the fourth state to ratify the United States Constitution, on January 2, 1788...

, Mississippi

Mississippi

Mississippi is a U.S. state located in the Southern United States. Jackson is the state capital and largest city. The name of the state derives from the Mississippi River, which flows along its western boundary, whose name comes from the Ojibwe word misi-ziibi...

, Missouri

Missouri

Missouri is a US state located in the Midwestern United States, bordered by Iowa, Illinois, Kentucky, Tennessee, Arkansas, Oklahoma, Kansas and Nebraska. With a 2010 population of 5,988,927, Missouri is the 18th most populous state in the nation and the fifth most populous in the Midwest. It...

, North Carolina

North Carolina

North Carolina is a state located in the southeastern United States. The state borders South Carolina and Georgia to the south, Tennessee to the west and Virginia to the north. North Carolina contains 100 counties. Its capital is Raleigh, and its largest city is Charlotte...

, Ohio

Ohio

Ohio is a Midwestern state in the United States. The 34th largest state by area in the U.S.,it is the 7th‑most populous with over 11.5 million residents, containing several major American cities and seven metropolitan areas with populations of 500,000 or more.The state's capital is Columbus...

and Texas

Texas

Texas is the second largest U.S. state by both area and population, and the largest state by area in the contiguous United States.The name, based on the Caddo word "Tejas" meaning "friends" or "allies", was applied by the Spanish to the Caddo themselves and to the region of their settlement in...

, any loan that is legal under the usury laws of any of those states may be made by an Arkansas-based bank under Section 731. The section does not apply to interstate banks with branches in the covered state, but headquartered elsewhere; however, Arkansas-based interstate banks like Arvest Bank

Arvest Bank

Arvest Bank is a diversified financial services company headquartered in Bentonville, Arkansas, with branches in Arkansas, Kansas, Oklahoma, and Missouri. Beginning with Benton County's first automatic teller machine in 1976 and the launch of an Internet banking web site in 1998, Arvest Bank has...

may export their Section 731 limits to other states.

Due to Section 731, it is generally regarded that Arkansas-based banks now have no usury limit for credit card

Credit card

A credit card is a small plastic card issued to users as a system of payment. It allows its holder to buy goods and services based on the holder's promise to pay for these goods and services...

s or for any loan of greater than $2,000 (since Alabama, Regions' home state, has no limits on those loans), with a limit of 18% (the minimum usury limit in Texas) or more on all other loans. However, once Wells Fargo

Wells Fargo

Wells Fargo & Company is an American multinational diversified financial services company with operations around the world. Wells Fargo is the fourth largest bank in the U.S. by assets and the largest bank by market capitalization. Wells Fargo is the second largest bank in deposits, home...

fully completes its proposed purchase of Century Bank

Century Bank

Century Bank was a bank headquartered in Texarkana, Texas that offered banking, mortgage, lending and trust services. Its holding company, Century Bancshares Inc., was based in Dallas, Texas...

(a Texas bank with Arkansas branches), Section 731 will do away with all usury limits for Arkansas-based banks since Wells Fargo's main bank charter is based in South Dakota

South Dakota

South Dakota is a state located in the Midwestern region of the United States. It is named after the Lakota and Dakota Sioux American Indian tribes. Once a part of Dakota Territory, South Dakota became a state on November 2, 1889. The state has an area of and an estimated population of just over...

, which repealed its usury laws many years ago.

Though designed for Arkansas, Section 731 may also apply to Alaska

Alaska

Alaska is the largest state in the United States by area. It is situated in the northwest extremity of the North American continent, with Canada to the east, the Arctic Ocean to the north, and the Pacific Ocean to the west and south, with Russia further west across the Bering Strait...

and California

California

California is a state located on the West Coast of the United States. It is by far the most populous U.S. state, and the third-largest by land area...

whose constitutions provide for the same basic usury limit, though unlike Arkansas their legislatures can (and generally do) set different limits. If Section 731 applies to those states, then all their usury limits are inapplicable to banks based in those states, since Wells Fargo has branches in both states.

Criticisms

Many believe that the Act directly helped cause the 2007 subprime mortgage financial crisis. President Barack Obama has stated that GLB led to deregulation that, among other things, allowed for the creation of giant financial supermarkets that could own investment banks, commercial banks and insurance firms, something banned since the Great Depression. Its passage, critics also say, cleared the way for companies that were too big and intertwined to fail. Economists Robert EkelundRobert Ekelund

Robert Burton Ekelund, Jr. is an American economist.-Education:Originally from Galveston, Texas, Ekelund attended St. Mary's University in San Antonio, Texas, earning his B.B.A. in economics in 1962 and his M.A. in economics and history the next year...

and Mark Thornton

Mark Thornton

Mark Thornton is an American economist of the Austrian School. Thornton has been described by the Advocates for Self-Government as "one of America's experts on the economics of illegal drugs." Thornton has written extensively on that topic, as well as on the economics of the American Civil War,...

have also criticized the Act as contributing to the crisis. They state that "in a world regulated by a gold standard

Gold standard

The gold standard is a monetary system in which the standard economic unit of account is a fixed mass of gold. There are distinct kinds of gold standard...

, 100% reserve banking, and no FDIC

Federal Deposit Insurance Corporation

The Federal Deposit Insurance Corporation is a United States government corporation created by the Glass–Steagall Act of 1933. It provides deposit insurance, which guarantees the safety of deposits in member banks, currently up to $250,000 per depositor per bank. , the FDIC insures deposits at...

deposit insurance" the Financial Services Modernization Act would have made "perfect sense" as a legitimate act of deregulation, but under the present fiat monetary system

Fiat money

Fiat money is money that has value only because of government regulation or law. The term derives from the Latin fiat, meaning "let it be done", as such money is established by government decree. Where fiat money is used as currency, the term fiat currency is used.Fiat money originated in 11th...

it "amounts to corporate welfare

Corporate welfare

Corporate welfare is a pejorative term describing a government's bestowal of money grants, tax breaks, or other special favorable treatment on corporations or selected corporations. The term compares corporate subsidies and welfare payments to the poor, and implies that corporations are much less...

for financial institutions and a moral hazard

Moral hazard

In economic theory, moral hazard refers to a situation in which a party makes a decision about how much risk to take, while another party bears the costs if things go badly, and the party insulated from risk behaves differently from how it would if it were fully exposed to the risk.Moral hazard...

that will make taxpayers pay dearly."

Nobel Prize

Nobel Prize

The Nobel Prizes are annual international awards bestowed by Scandinavian committees in recognition of cultural and scientific advances. The will of the Swedish chemist Alfred Nobel, the inventor of dynamite, established the prizes in 1895...

-winning economist

Economist

An economist is a professional in the social science discipline of economics. The individual may also study, develop, and apply theories and concepts from economics and write about economic policy...

Joseph Stiglitz has also argued that the Act helped to create the crisis. An article in the liberal publication The Nation

The Nation

The Nation is the oldest continuously published weekly magazine in the United States. The periodical, devoted to politics and culture, is self-described as "the flagship of the left." Founded on July 6, 1865, It is published by The Nation Company, L.P., at 33 Irving Place, New York City.The Nation...

asserted that GLB was responsible for the creation of entities that took on more risk due to their being considered “too big to fail

Too Big to Fail

Too Big to Fail is a television drama film in the United States broadcast on HBO on May 23, 2011. It is based on the non-fiction book Too Big to Fail by Andrew Ross Sorkin. The TV film was directed by Curtis Hanson...

."

Defense

According to a 2009 policy report from the libertarian Cato InstituteCato Institute

The Cato Institute is a libertarian think tank headquartered in Washington, D.C. It was founded in 1977 by Edward H. Crane, who remains president and CEO, and Charles Koch, chairman of the board and chief executive officer of the conglomerate Koch Industries, Inc., the largest privately held...

authored by one of the institute's directors, Mark A. Calabria

Mark A. Calabria

Mark A. Calabria, Ph.D. is Director of Financial Regulation Studies at the Cato Institute. He was a member of the senior staff of the U.S. Senate Committee on Banking, Housing and Urban Affairs where he handled issues related to housing, mortgage finance, economics, banking and insurance for...

, critics of the legislation feared that, with the allowance for mergers between investment and commercial banks, GLB allowed the newly-merged banks to take on riskier investments while at the same time removing any requirements to maintain enough equity, exposing the assets of its banking customers. Calabria claimed that, prior to the passage of GLB in 1999, investment banks were already capable of holding and trading the very financial assets claimed to be the cause of the mortgage crisis, and were also already able to keep their books as they had. He concluded that greater access to investment capital as many investment banks went public on the market explains the shift in their holdings to trading portfolios. Calabria noted that after GLB passed, most investment banks did not merge with depository commercial banks, and that in fact, the few banks that did merge weathered the crisis better than those that did not.

In February 2009, one of the act's co-authors, former Senator Phil Gramm, also defended his bill:

[I]f GLB was the problem, the crisis would have been expected to have originated in Europe where they never had Glass–Steagall requirements to begin with. Also, the financial firms that failed in this crisis, like LehmanLehman BrothersLehman Brothers Holdings Inc. was a global financial services firm. Before declaring bankruptcy in 2008, Lehman was the fourth largest investment bank in the USA , doing business in investment banking, equity and fixed-income sales and trading Lehman Brothers Holdings Inc. (former NYSE ticker...

, were the least diversified and the ones that survived, like J.P. Morgan, were the most diversified. Moreover, GLB didn't deregulate anything. It established the Federal Reserve as a superregulator, overseeing all Financial Services Holding Companies. All activities of financial institutions continued to be regulated on a functional basis by the regulators that had regulated those activities prior to GLB.

Bill Clinton

Bill Clinton

William Jefferson "Bill" Clinton is an American politician who served as the 42nd President of the United States from 1993 to 2001. Inaugurated at age 46, he was the third-youngest president. He took office at the end of the Cold War, and was the first president of the baby boomer generation...

, as well as economists Brad DeLong and Tyler Cowen

Tyler Cowen

Tyler Cowen is an American economist, academic, and writer. He occupies the Holbert C. Harris Chair of economics as a professor at George Mason University and is co-author, with Alex Tabarrok, of the popular economics blog Marginal Revolution...

have all argued that the Gramm–Leach–Bliley Act softened the impact of the crisis.

Atlantic Monthly columnist Megan McArdle

Megan McArdle

Megan McArdle is a Washington, D.C.-based blogger and journalist. She writes mostly about economics, finance and government policy from a moderate libertarian or classical liberal perspective. She currently serves as the business and economics editor, as well as a blogger, for The Atlantic. She is...

has argued that if the act was "part of the problem, it would be the commercial banks, not the investment banks, that were in trouble" and repeal would not have helped the situation. An article in the conservative publication, National Review

National Review

National Review is a biweekly magazine founded by the late author William F. Buckley, Jr., in 1955 and based in New York City. It describes itself as "America's most widely read and influential magazine and web site for conservative news, commentary, and opinion."Although the print version of the...

, has made the same argument, calling liberal allegations about the Act “folk economics

Folklore

Folklore consists of legends, music, oral history, proverbs, jokes, popular beliefs, fairy tales and customs that are the traditions of a culture, subculture, or group. It is also the set of practices through which those expressive genres are shared. The study of folklore is sometimes called...

.”

See also

- Bank regulationBank regulationBank regulations are a form of government regulation which subject banks to certain requirements, restrictions and guidelines. This regulatory structure creates transparency between banking institutions and the individuals and corporations with whom they conduct business, among other things...

- Financial regulationFinancial regulationFinancial regulation is a form of regulation or supervision, which subjects financial institutions to certain requirements, restrictions and guidelines, aiming to maintain the integrity of the financial system...

- U.S. Securities and Exchange Commission

- Commodity Futures Modernization Act of 2000Commodity Futures Modernization Act of 2000The Commodity Futures Modernization Act of 2000 is United States federal legislation that officially ensured the deregulation of financial products known as over-the-counter derivatives. It was signed into law on December 21, 2000 by President Bill Clinton...

- FACTA

- Sarbanes-Oxley ActSarbanes-Oxley ActThe Sarbanes–Oxley Act of 2002 , also known as the 'Public Company Accounting Reform and Investor Protection Act' and 'Corporate and Auditing Accountability and Responsibility Act' and commonly called Sarbanes–Oxley, Sarbox or SOX, is a United States federal law enacted on July 30, 2002, which...

Sources

- Financial Privacy: The Gramm-Leach Bliley Act, Federal Trade CommissionFederal Trade CommissionThe Federal Trade Commission is an independent agency of the United States government, established in 1914 by the Federal Trade Commission Act...

, 1999 - Gramm-Leach-Bliley Act,15 USC, Subchapter I, Sec. 6801-6809, Disclosure of Nonpublic Personal Information, FTC, 1999

- Mike Chapple, Gramm-Leach-Bliley and You, November 18, 2003

- Robert H. Ledig, Gramm-Leach-Bliley Act Financial Privacy Provisions:The Federal Government Imposes Broad Requirements to Address Consumer Privacy Concerns

- The Gramm-Leach-Bliley Act: The Financial Privacy Rule, Federal Trade Commission

- In Brief: The Financial Privacy Requirements of the Gramm-Leach-Bliley Act, Federal Trade Commission

- The Gramm-Leach-Bliley Act — “History of the GLBA”, Electronic Privacy Information CenterElectronic Privacy Information CenterElectronic Privacy Information Center is a public interest research group in Washington, D.C. It was established in 1994 to focus public attention on emerging civil liberties issues and to protect privacy, the First Amendment, and constitutional values in the information age...

- Financial Institution Privacy Protection Act of 2003 — 108th CONGRESS, 1st Session, S. 1458, “To amend the Gramm-Leach-Bliley Act to provide for enhanced protection of nonpublic personal information, including health information, and for other purposes.”, In the Senate of the United States; July 25 (legislative day, JULY 21), 2003, Library of CongressLibrary of CongressThe Library of Congress is the research library of the United States Congress, de facto national library of the United States, and the oldest federal cultural institution in the United States. Located in three buildings in Washington, D.C., it is the largest library in the world by shelf space and...

- Testimony of (Federal Reserve) Governor Laurence H. Meyer: Merchant banking, Federal Reserve BankFederal Reserve BankThe twelve Federal Reserve Banks form a major part of the Federal Reserve System, the central banking system of the United States. The twelve federal reserve banks together divide the nation into twelve Federal Reserve Districts, the twelve banking districts created by the Federal Reserve Act of...

- Martin McLaughlin, Clinton, Republicans agree to deregulation of US financial system, World Socialist Web Site, November 1, 1999, retrieved on October 9, 2008

Compliance information

- Gramm-Leach-Bliley Act, 15 USC, Subchapter I, Sec. 6801-6809 - Disclosure of Nonpublic Personal Information

- Financial Institutions and Customer Data: Complying with the Safeguards Rule

- How To Comply with the Privacy of Consumer Financial Information Rule of the Gramm-Leach-Bliley Act

Consumer/client rights information

- Disclosure of Nonpublic Personal Information

- What Can You Do To Protect Your Privacy

- Privacy Choices for Your Personal Financial Information

- Pretexting: Your Personal Information Revealed