Menu costs

Encyclopedia

In economics

, a menu cost is the cost to a firm

resulting from changing its prices. The name stems from the cost of restaurants literally printing new menu

s, but economists use it to refer to the costs of changing nominal prices in general. In this broader definition, menu costs might include updating computer systems, re-tagging items, and hiring consultants to develop new pricing strategies as well as the literal costs of printing menus. Because of this expense, firms sometimes do not always change their prices with every change in supply and demand

, leading to price stickiness.

Generally, the effect on the firm of small shifts in price (by changes in supply

and/or demand

, or else because of slight adjustments in monetary policy

) are relatively minor compared to the costs of notifying the public of this new information. Therefore, the firm would rather exist in slight disequilbrium than incur the menu costs.

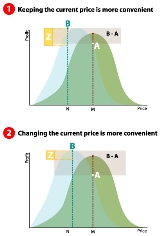

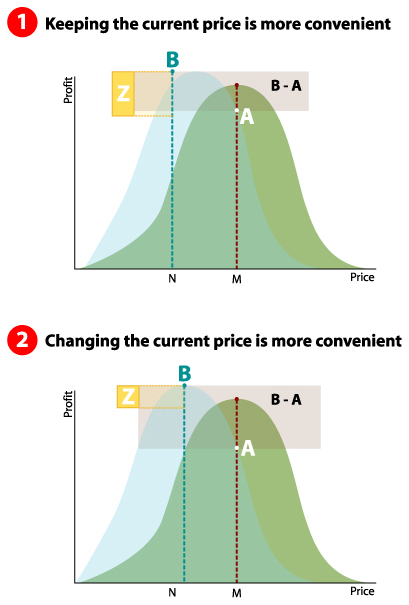

Consider a hypothetical firm in a hypothetical economy, with a concave

Consider a hypothetical firm in a hypothetical economy, with a concave

graph describing the relationship between the price

of its good and the firm's corresponding profit

. As always, the profit maximizing point lies at the very top for the curve.

Now suppose that there exists a drop in aggregate output. While this causes real wages to fall (shifting the profit curve upward, allowing more profit for the same price), it also diminishes demand for the firm's product (shifting the curve down). Suppose the net effect is a downward shift (as it usually is).

The result is a maximum profit associated with a lower price (the max profit shifts to the left a bit, as a result of the profit curve moving). Suppose the old price (and thus the old maximizing profit price) was M and the new maximizing price is N. Also suppose the new maximum profit is B and new profit corresponding to the old price is A. Thus price M yields A in profit and price N yields B in profit.

Now suppose there is a menu cost, Z, in changing from price M to price N. Because the firm must pay Z to make this change, they will only pay it if Z < B-A. Thus tiny fluctuations in the economy leads to small differences in B and A so firms do not change their price, even if Z is small.

Note that if Z is zero, then prices will change all the time, allowing for firms to squeeze out every bit of profit from every change in the economy.

Economics

Economics is the social science that analyzes the production, distribution, and consumption of goods and services. The term economics comes from the Ancient Greek from + , hence "rules of the house"...

, a menu cost is the cost to a firm

Theory of the firm

The theory of the firm consists of a number of economic theories that describe the nature of the firm, company, or corporation, including its existence, behavior, structure, and relationship to the market.-Overview:...

resulting from changing its prices. The name stems from the cost of restaurants literally printing new menu

Menu

In a restaurant, a menu is a presentation of food and beverage offerings. A menu may be a la carte – which guests use to choose from a list of options – or table d'hôte, in which case a pre-established sequence of courses is served....

s, but economists use it to refer to the costs of changing nominal prices in general. In this broader definition, menu costs might include updating computer systems, re-tagging items, and hiring consultants to develop new pricing strategies as well as the literal costs of printing menus. Because of this expense, firms sometimes do not always change their prices with every change in supply and demand

Supply and demand

Supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good will vary until it settles at a point where the quantity demanded by consumers will equal the quantity supplied by producers , resulting in an...

, leading to price stickiness.

Generally, the effect on the firm of small shifts in price (by changes in supply

Supply (economics)

In economics, supply is the amount of some product producers are willing and able to sell at a given price all other factors being held constant. Usually, supply is plotted as a supply curve showing the relationship of price to the amount of product businesses are willing to sell.In economics the...

and/or demand

Demand (economics)

In economics, demand is the desire to own anything, the ability to pay for it, and the willingness to pay . The term demand signifies the ability or the willingness to buy a particular commodity at a given point of time....

, or else because of slight adjustments in monetary policy

Monetary policy

Monetary policy is the process by which the monetary authority of a country controls the supply of money, often targeting a rate of interest for the purpose of promoting economic growth and stability. The official goals usually include relatively stable prices and low unemployment...

) are relatively minor compared to the costs of notifying the public of this new information. Therefore, the firm would rather exist in slight disequilbrium than incur the menu costs.

Deeper analysis

Concave function

In mathematics, a concave function is the negative of a convex function. A concave function is also synonymously called concave downwards, concave down, convex upwards, convex cap or upper convex.-Definition:...

graph describing the relationship between the price

Price

-Definition:In ordinary usage, price is the quantity of payment or compensation given by one party to another in return for goods or services.In modern economies, prices are generally expressed in units of some form of currency...

of its good and the firm's corresponding profit

Profit (economics)

In economics, the term profit has two related but distinct meanings. Normal profit represents the total opportunity costs of a venture to an entrepreneur or investor, whilst economic profit In economics, the term profit has two related but distinct meanings. Normal profit represents the total...

. As always, the profit maximizing point lies at the very top for the curve.

Now suppose that there exists a drop in aggregate output. While this causes real wages to fall (shifting the profit curve upward, allowing more profit for the same price), it also diminishes demand for the firm's product (shifting the curve down). Suppose the net effect is a downward shift (as it usually is).

The result is a maximum profit associated with a lower price (the max profit shifts to the left a bit, as a result of the profit curve moving). Suppose the old price (and thus the old maximizing profit price) was M and the new maximizing price is N. Also suppose the new maximum profit is B and new profit corresponding to the old price is A. Thus price M yields A in profit and price N yields B in profit.

Now suppose there is a menu cost, Z, in changing from price M to price N. Because the firm must pay Z to make this change, they will only pay it if Z < B-A. Thus tiny fluctuations in the economy leads to small differences in B and A so firms do not change their price, even if Z is small.

Note that if Z is zero, then prices will change all the time, allowing for firms to squeeze out every bit of profit from every change in the economy.

See also

- New Keynesian economicsNew Keynesian economicsNew Keynesian economics is a school of contemporary macroeconomics that strives to provide microeconomic foundations for Keynesian economics. It developed partly as a response to criticisms of Keynesian macroeconomics by adherents of New Classical macroeconomics.Two main assumptions define the New...

- Sticky (economics)Sticky (economics)Sticky, in the social sciences and particularly economics, describes a situation in which a variable is resistant to change. Sticky prices are an important part of macroeconomic theory since they may be used to explain why markets might not reach equilibrium right away. Nominal wages are often said...

- Shoe leather costShoe leather costShoe leather cost refers to the cost of time and effort that people spend trying to counter-act the effects of inflation, such as holding less cash and having to make additional trips to the bank...

- InflationInflationIn economics, inflation is a rise in the general level of prices of goods and services in an economy over a period of time.When the general price level rises, each unit of currency buys fewer goods and services. Consequently, inflation also reflects an erosion in the purchasing power of money – a...