Tax protester Sixteenth Amendment arguments

Encyclopedia

Tax protester Sixteenth Amendment arguments are assertions that the imposition of the U.S. federal income tax

is illegal because the Sixteenth Amendment

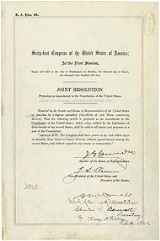

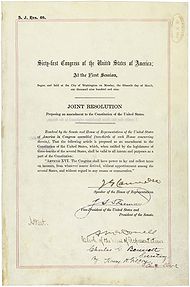

to the United States Constitution, which reads "The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration," was never properly ratified

, or that the amendment provides no power to tax income. Proper ratification of the Sixteenth Amendment is disputed by tax protesters

who argue that the quoted text of the Amendment differed from the text proposed by Congress

, or that Ohio

was not a State during ratification. Sixteenth Amendment ratification arguments have been rejected in every court case where they have been raised and have been identified as legally frivolous

.

Some protesters have argued that because the Sixteenth Amendment does not contain the words "repeal

" or "repealed", the Amendment is ineffective to change the law. Others argue that due to language in Stanton v. Baltic Mining Co.

, the income tax is an unconstitutional direct tax

that should be apportioned (divided equally amongst the population of the various states). Several tax protesters assert that the Congress has no constitutional power to tax labor or income from labor, citing a variety of court cases. These arguments include claims that the word "income

" as used in the Sixteenth Amendment cannot be interpreted as applying to wage

s; that wages are not income because labor is exchanged for them; that taxing wages violates individuals' right to property, and several others. Another argument raised is that because the federal income tax is progressive

, the discriminations and inequalities created by the tax should render the tax unconstitutional under the 14th Amendment

, which guarantees equal protection under the law. Such arguments have been ruled without merit under contemporary jurisprudence.

Many tax protesters contend that the Sixteenth Amendment to the United States Constitution was never properly ratified (see, e.g., Devvy Kidd).

Many tax protesters contend that the Sixteenth Amendment to the United States Constitution was never properly ratified (see, e.g., Devvy Kidd).

The "non-ratification" argument was presented by defendant James Walter Scott in the 1975 case of United States v. Scott, some sixty-two years after the ratification. In Scott, the defendant -- who called himself a "national tax resistance leader" -- had been convicted of willful failure to file federal income tax returns for the years 1969 through 1972, and the conviction was upheld by the United States Court of Appeals for the Ninth Circuit. In the 1977 case of Ex parte Tammen, the United States District Court for the Northern District of Texas noted testimony in the case to the effect that taxpayer Bob Tammen had become involved with a group called "United Tax Action Patriots," a group that took the position "that the Sixteenth Amendment was improperly passed and therefore invalid...." The specific issue of the validity of the ratification of the Amendment was neither presented to nor decided by the court in the Tammen case.

After the Scott and Tammen decisions, two lines of court cases eventually developed. The first group of cases deals with the claims of William J. Benson, co-author of the book The Law That Never Was

(1985). The second line of cases involves the contention that Ohio was not a state in 1913 at the time of the ratification.(Ohio became a state in 1803.)

The earliest reported court cases where Benson's arguments were actually raised appear to be United States v. Wojtas and United States v. House. Benson testified in the House case to no avail. The Benson contention was comprehensively addressed by the Seventh Circuit Court of Appeals in United States v. Thomas:

Benson was unsuccessful with his Sixteenth Amendment argument when he had his own legal problems. He was prosecuted for tax evasion and willful failure to file tax returns. The court rejected his Sixteenth Amendment "non-ratification" argument in United States v. Benson. William J. Benson was convicted of tax evasion and willful failure to file tax returns in connection with over $100,000 of unreported income, and his conviction was upheld on appeal. He was sentenced to four years in prison and five years of probation.

On December 17, 2007, the United States District Court for the Northern District of Illinois ruled that Benson's non-ratification argument constituted a "fraud perpetrated by Benson" that had "caused needless confusion and a waste of the customers' and the IRS' time and resources." The court stated: "Benson has failed to point to evidence that would create a genuinely disputed fact regarding whether the Sixteenth Amendment was properly ratified or whether United States Citizens are legally obligated to pay federal taxes." The court ruled that "Benson's position has no merit and he has used his fraudulent tax advice to deceive other citizens and profit from it" in violation of . The court granted an injunction under prohibiting Benson from promoting the theories in Benson's "Reliance Defense Package" (containing the non-ratification argument), which the court referred to as "false and fraudulent advice concerning the payment of federal taxes."

Benson appealed that decision, and the United States Court of Appeals for the Seventh Circuit also ruled against Benson. The Court of Appeals stated:

The Court of Appeals also ruled that the government could obtain a ruling ordering Benson to turn his customer list over to the government. Benson petitioned the United States Supreme Court, and the Supreme Court rejected his petition on November 30, 2009.

Similar Sixteenth Amendment arguments have been uniformly rejected by other United States Circuit courts in other cases including Sisk v. Commissioner; United States v. Sitka; and United States v. Stahl. The non-ratification argument has been specifically deemed legally frivolous

in Brown v. Commissioner; Lysiak v. Commissioner; and Miller v. United States.

did not pass an official proclamation (Pub. L. 204) recognizing the date of Ohio's 1803 admission to statehood until 1953 (see Ohio and the Constitution), Ohio

was not a state until 1953 and therefore the Sixteenth Amendment was not properly ratified. The earliest reported court case where this argument was raised appears to be Ivey v. United States, some sixty-three years after the ratification and 173 years after Ohio's admission as a state. This argument was rejected in the Ivey case, and has been uniformly rejected by the courts. See also McMullen v. United States, McCoy v. Alexander, Lorre v. Alexander, McKenney v. Blumenthal and Knoblauch v. Commissioner. Further, even if Ohio's ratification was not valid, the Amendment was ratified by 41 other states, well in excess of the 36 needed for it to be properly ratified.

In Baker v. Commissioner, the court stated:

The argument that the Sixteenth Amendment was not ratified and variations of this argument have been officially identified as legally frivolous federal tax return positions for purposes of the $5,000 frivolous tax return penalty imposed under Internal Revenue Code section 6702(a).

In Buchbinder v. Commissioner, the taxpayers cited the case of Eisner v. Macomber and argued that "the Sixteenth Amendment must be interpreted so as not to 'repeal or modify' the original Articles of the Constitution." The United States Tax Court

rejected that and all other arguments by Bruce and Elaine Buchbinder (the taxpayer-petitioners), stating: "We will not dress petitioners' frivolous tax-protester ramblings with a cloak of respectability.... We find that petitioners in this case have pursued a frivolous cause of action. We find that they are liable for a penalty in the amount of $250.00 under the provisions of [Internal Revenue Code] section 6673." The actual statement by the United States Supreme Court in Eisner v. Macomber is that the Sixteenth Amendment "shall not be extended by loose construction, so as to repeal or modify, except as applied to income, those provisions of the Constitution that require an apportionment according to population for direct taxes upon property, real and personal ... In order, therefore, that the clauses cited from Article I of the Constitution may have proper force and effect, save only as modified by the Amendment ... it becomes essential to distinguish between what is and what is not 'income'...."

Tax protesters argue that in light of this language, the income tax is unconstitutional in that it is a direct tax and that the tax should be apportioned (divided equally amongst the population of the various states).

The above quoted language in Stanton v. Baltic Mining Co. is not a holding of law in the case. (Compare Ratio decidendi

, Precedent

, Stare decisis

and Obiter dictum

for a fuller explanation.)

The quoted language regarding the "complete and plenary power of income taxation possessed by Congress from the beginning" is a reference to the power granted to Congress by the original text of Article I of the U.S. Constitution. The reference to "being taken out of the category of indirect taxation to which it [the income tax] belonged" is a reference to the effect of the 1895 Court decision in Pollock v. Farmers' Loan & Trust Co.

, where taxes on income from property (such as interest income and dividend income) — which, like taxes on income from labor, had always been considered indirect taxes (and therefore not subject to the apportionment rule) — were, beginning in 1895, treated as direct taxes. The Sixteenth Amendment overruled the effect of Pollock, making the source of the income irrelevant with respect to the apportionment rule, and thereby placing taxes on income from property back into the category of indirect taxes such as income from labor (the Sixteenth Amendment expressly stating that Congress has power to impose income taxes regardless of the source of the income, without apportionment among the states, and without regard to any census or enumeration).

The Court noted that the case "was commenced by the appellant [John R. Stanton] as a stockholder of the Baltic Mining Company, the appellee, to enjoin [i.e., prevent] the voluntary payment by the corporation and its officers of the tax assessed against it under the income tax section of the tariff act of October 3, 1913." On a direct appeal from the trial court, the U.S. Supreme Court affirmed the lower court's decision, which had dismissed Stanton's motion (i.e., had rejected Stanton's request) for a court order to prevent Baltic Mining Company from paying the income tax.

Stanton argued that the tax law was unconstitutional and void under the Fifth Amendment to the United States Constitution

in that the law denied "to mining companies and their stockholders equal protection of the laws and deprive[d] them of their property without due process of law." The Court rejected that argument. Stanton also argued that the Sixteenth Amendment "authorizes only an exceptional direct income tax without apportionment, to which the tax in question does not conform" and that therefore the income tax was "not within the authority of that Amendment." The Court also rejected this argument. Thus, the U.S. Supreme Court, in upholding the constitutionality of the income tax under the 1913 Act, contradicts those tax protesters arguments that the income tax is unconstitutional under either the Fifth Amendment or the Sixteenth Amendment.

In Abrams v. Commissioner, the United States Tax Court stated: "Since the ratification of the Sixteenth Amendment, it is immaterial with respect to income taxes, whether the tax is a direct or indirect tax. The whole purpose of the Sixteenth Amendment was to relieve all income taxes when imposed from [the requirement of] apportionment and from [the requirement of] a consideration of the source whence the income was derived."

Income tax in the United States

In the United States, a tax is imposed on income by the Federal, most states, and many local governments. The income tax is determined by applying a tax rate, which may increase as income increases, to taxable income as defined. Individuals and corporations are directly taxable, and estates and...

is illegal because the Sixteenth Amendment

Sixteenth Amendment to the United States Constitution

The Sixteenth Amendment to the United States Constitution allows the Congress to levy an income tax without apportioning it among the states or basing it on Census results...

to the United States Constitution, which reads "The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration," was never properly ratified

Ratification

Ratification is a principal's approval of an act of its agent where the agent lacked authority to legally bind the principal. The term applies to private contract law, international treaties, and constitutionals in federations such as the United States and Canada.- Private law :In contract law, the...

, or that the amendment provides no power to tax income. Proper ratification of the Sixteenth Amendment is disputed by tax protesters

Tax protester (United States)

A tax protester is someone who refuses to pay a tax on constitutional or legal grounds, typically because he or she believes that the tax laws are unconstitutional or otherwise invalid...

who argue that the quoted text of the Amendment differed from the text proposed by Congress

United States Congress

The United States Congress is the bicameral legislature of the federal government of the United States, consisting of the Senate and the House of Representatives. The Congress meets in the United States Capitol in Washington, D.C....

, or that Ohio

Ohio

Ohio is a Midwestern state in the United States. The 34th largest state by area in the U.S.,it is the 7th‑most populous with over 11.5 million residents, containing several major American cities and seven metropolitan areas with populations of 500,000 or more.The state's capital is Columbus...

was not a State during ratification. Sixteenth Amendment ratification arguments have been rejected in every court case where they have been raised and have been identified as legally frivolous

Frivolous litigation

In law, frivolous litigation is the practice of starting or carrying on law suits that, due to their lack of legal merit, have little to no chance of being won. The term does not include cases that may be lost due to other matters not related to legal merit...

.

Some protesters have argued that because the Sixteenth Amendment does not contain the words "repeal

Repeal

A repeal is the amendment, removal or reversal of a law. This is generally done when a law is no longer effective, or it is shown that a law is having far more negative consequences than were originally envisioned....

" or "repealed", the Amendment is ineffective to change the law. Others argue that due to language in Stanton v. Baltic Mining Co.

Stanton v. Baltic Mining Co.

Stanton v. Baltic Mining Co., 240 U.S. 103 , was a case decided by the Supreme Court of the United States.- History of the case :Plaintiff John R...

, the income tax is an unconstitutional direct tax

Direct tax

The term direct tax generally means a tax paid directly to the government by the persons on whom it is imposed.-General meaning:In the general sense, a direct tax is one paid directly to the government by the persons on whom it is imposed...

that should be apportioned (divided equally amongst the population of the various states). Several tax protesters assert that the Congress has no constitutional power to tax labor or income from labor, citing a variety of court cases. These arguments include claims that the word "income

Income

Income is the consumption and savings opportunity gained by an entity within a specified time frame, which is generally expressed in monetary terms. However, for households and individuals, "income is the sum of all the wages, salaries, profits, interests payments, rents and other forms of earnings...

" as used in the Sixteenth Amendment cannot be interpreted as applying to wage

Wage

A wage is a compensation, usually financial, received by workers in exchange for their labor.Compensation in terms of wages is given to workers and compensation in terms of salary is given to employees...

s; that wages are not income because labor is exchanged for them; that taxing wages violates individuals' right to property, and several others. Another argument raised is that because the federal income tax is progressive

Progressive tax

A progressive tax is a tax by which the tax rate increases as the taxable base amount increases. "Progressive" describes a distribution effect on income or expenditure, referring to the way the rate progresses from low to high, where the average tax rate is less than the marginal tax rate...

, the discriminations and inequalities created by the tax should render the tax unconstitutional under the 14th Amendment

Fourteenth Amendment to the United States Constitution

The Fourteenth Amendment to the United States Constitution was adopted on July 9, 1868, as one of the Reconstruction Amendments.Its Citizenship Clause provides a broad definition of citizenship that overruled the Dred Scott v...

, which guarantees equal protection under the law. Such arguments have been ruled without merit under contemporary jurisprudence.

Sixteenth Amendment ratification

The "non-ratification" argument was presented by defendant James Walter Scott in the 1975 case of United States v. Scott, some sixty-two years after the ratification. In Scott, the defendant -- who called himself a "national tax resistance leader" -- had been convicted of willful failure to file federal income tax returns for the years 1969 through 1972, and the conviction was upheld by the United States Court of Appeals for the Ninth Circuit. In the 1977 case of Ex parte Tammen, the United States District Court for the Northern District of Texas noted testimony in the case to the effect that taxpayer Bob Tammen had become involved with a group called "United Tax Action Patriots," a group that took the position "that the Sixteenth Amendment was improperly passed and therefore invalid...." The specific issue of the validity of the ratification of the Amendment was neither presented to nor decided by the court in the Tammen case.

After the Scott and Tammen decisions, two lines of court cases eventually developed. The first group of cases deals with the claims of William J. Benson, co-author of the book The Law That Never Was

The Law that Never Was

The Law That Never Was: The Fraud of the 16th Amendment and Personal Income Tax is a 1985 book by William J. Benson and Martin J. "Red" Beckman which claims that the Sixteenth Amendment to the United States Constitution, commonly known as the income tax amendment, was never properly ratified...

(1985). The second line of cases involves the contention that Ohio was not a state in 1913 at the time of the ratification.(Ohio became a state in 1803.)

Benson contentions

The William J. Benson contention is essentially that the legislatures of various states passed ratifying resolutions in which the quoted text of the Amendment differed from the text proposed by Congress in terms of capitalization, spelling of words, or punctuation marks (e.g. semi-colons instead of commas), and that these differences made the ratification invalid. Benson makes other assertions including claims that one or more states rejected the Amendment and that the state or states were falsely reported as having ratified the Amendment. As explained below, the Benson arguments have been rejected in every court case where they have been raised, and were explicitly ruled to be fraudulent in 2007.The earliest reported court cases where Benson's arguments were actually raised appear to be United States v. Wojtas and United States v. House. Benson testified in the House case to no avail. The Benson contention was comprehensively addressed by the Seventh Circuit Court of Appeals in United States v. Thomas:

Benson was unsuccessful with his Sixteenth Amendment argument when he had his own legal problems. He was prosecuted for tax evasion and willful failure to file tax returns. The court rejected his Sixteenth Amendment "non-ratification" argument in United States v. Benson. William J. Benson was convicted of tax evasion and willful failure to file tax returns in connection with over $100,000 of unreported income, and his conviction was upheld on appeal. He was sentenced to four years in prison and five years of probation.

On December 17, 2007, the United States District Court for the Northern District of Illinois ruled that Benson's non-ratification argument constituted a "fraud perpetrated by Benson" that had "caused needless confusion and a waste of the customers' and the IRS' time and resources." The court stated: "Benson has failed to point to evidence that would create a genuinely disputed fact regarding whether the Sixteenth Amendment was properly ratified or whether United States Citizens are legally obligated to pay federal taxes." The court ruled that "Benson's position has no merit and he has used his fraudulent tax advice to deceive other citizens and profit from it" in violation of . The court granted an injunction under prohibiting Benson from promoting the theories in Benson's "Reliance Defense Package" (containing the non-ratification argument), which the court referred to as "false and fraudulent advice concerning the payment of federal taxes."

Benson appealed that decision, and the United States Court of Appeals for the Seventh Circuit also ruled against Benson. The Court of Appeals stated:

-

- Benson knew or had reason to know that his statements were false or fraudulent. 26 U.S.C. [section] 6700(a)(2)(A). Benson's claim to have discovered that the Sixteenth Amendment was not ratified has been rejected by this Court in Benson's own criminal appeal.... Benson knows that his claim that he can rely on his book to prevent federal prosecution is equally false because his attempt to rely on his book in his own criminal case was ineffective.

The Court of Appeals also ruled that the government could obtain a ruling ordering Benson to turn his customer list over to the government. Benson petitioned the United States Supreme Court, and the Supreme Court rejected his petition on November 30, 2009.

Similar Sixteenth Amendment arguments have been uniformly rejected by other United States Circuit courts in other cases including Sisk v. Commissioner; United States v. Sitka; and United States v. Stahl. The non-ratification argument has been specifically deemed legally frivolous

Frivolous litigation

In law, frivolous litigation is the practice of starting or carrying on law suits that, due to their lack of legal merit, have little to no chance of being won. The term does not include cases that may be lost due to other matters not related to legal merit...

in Brown v. Commissioner; Lysiak v. Commissioner; and Miller v. United States.

Ohio's statehood

Another argument made by some tax protesters is that because the United States CongressUnited States Congress

The United States Congress is the bicameral legislature of the federal government of the United States, consisting of the Senate and the House of Representatives. The Congress meets in the United States Capitol in Washington, D.C....

did not pass an official proclamation (Pub. L. 204) recognizing the date of Ohio's 1803 admission to statehood until 1953 (see Ohio and the Constitution), Ohio

Ohio

Ohio is a Midwestern state in the United States. The 34th largest state by area in the U.S.,it is the 7th‑most populous with over 11.5 million residents, containing several major American cities and seven metropolitan areas with populations of 500,000 or more.The state's capital is Columbus...

was not a state until 1953 and therefore the Sixteenth Amendment was not properly ratified. The earliest reported court case where this argument was raised appears to be Ivey v. United States, some sixty-three years after the ratification and 173 years after Ohio's admission as a state. This argument was rejected in the Ivey case, and has been uniformly rejected by the courts. See also McMullen v. United States, McCoy v. Alexander, Lorre v. Alexander, McKenney v. Blumenthal and Knoblauch v. Commissioner. Further, even if Ohio's ratification was not valid, the Amendment was ratified by 41 other states, well in excess of the 36 needed for it to be properly ratified.

In Baker v. Commissioner, the court stated:

-

- Petitioner's theory [that Ohio was not a state until 1953 and that the Sixteenth Amendment was not properly ratified] is based on the enactment of Pub. L. 204, ch. 337, 67 Stat. 407 (1953) relating to Ohio's Admission into the Union. As the legislative history of this Act makes clear, its purpose was to settle a burning debate as to the precise date upon which Ohio became one of the United States. S. Rept. No. 720 to accompany H.J. Res. 121 (Pub. L. 204), 82d Cong. 2d Sess. (1953). We have been cited to no authorities which indicate that Ohio became a state later than March 1, 1803, irrespective of Pub. L. 204.

The argument that the Sixteenth Amendment was not ratified and variations of this argument have been officially identified as legally frivolous federal tax return positions for purposes of the $5,000 frivolous tax return penalty imposed under Internal Revenue Code section 6702(a).

Repeal clause

Some protesters have argued that because the Sixteenth Amendment does not contain the words "repeal" or "repealed", the Amendment is ineffective to change the law. According to legal commentator Daniel B. Evans:In Buchbinder v. Commissioner, the taxpayers cited the case of Eisner v. Macomber and argued that "the Sixteenth Amendment must be interpreted so as not to 'repeal or modify' the original Articles of the Constitution." The United States Tax Court

United States Tax Court

The United States Tax Court is a federal trial court of record established by Congress under Article I of the U.S. Constitution, section 8 of which provides that the Congress has the power to "constitute Tribunals inferior to the supreme Court"...

rejected that and all other arguments by Bruce and Elaine Buchbinder (the taxpayer-petitioners), stating: "We will not dress petitioners' frivolous tax-protester ramblings with a cloak of respectability.... We find that petitioners in this case have pursued a frivolous cause of action. We find that they are liable for a penalty in the amount of $250.00 under the provisions of [Internal Revenue Code] section 6673." The actual statement by the United States Supreme Court in Eisner v. Macomber is that the Sixteenth Amendment "shall not be extended by loose construction, so as to repeal or modify, except as applied to income, those provisions of the Constitution that require an apportionment according to population for direct taxes upon property, real and personal ... In order, therefore, that the clauses cited from Article I of the Constitution may have proper force and effect, save only as modified by the Amendment ... it becomes essential to distinguish between what is and what is not 'income'...."

Stanton v. Baltic Mining Co.

In Parker v. Commissioner, tax protester Alton M. Parker, Sr., challenged the levying of tax upon individual income, based on language in the U.S. Supreme Court decision in Stanton v. Baltic Mining Co., to the effect that the Sixteenth Amendment "conferred no new power of taxation, but simply prohibited the previous complete and plenary power of income taxation possessed by Congress from the beginning from being taken out of the category of indirect taxation to which it inherently belonged [. . . .]" The United States Court of Appeals for the Fifth Circuit rejected Parker's argument, and stated that Parker's proposition is "only partially correct, and in its critical aspect, is incorrect. The Court of Appeals re-affirmed that the Congress has the power to impose the income tax, and stated that the Sixteenth Amendment "merely eliminates the requirement that the direct income tax be apportioned among the states." The court ruled that Parker had raised a "frivolous" appeal.Tax protesters argue that in light of this language, the income tax is unconstitutional in that it is a direct tax and that the tax should be apportioned (divided equally amongst the population of the various states).

The above quoted language in Stanton v. Baltic Mining Co. is not a holding of law in the case. (Compare Ratio decidendi

Ratio decidendi

Ratio decidendi is a Latin phrase meaning "the reason" or "the rationale for the decision." The ratio decidendi is "[t]he point in a case which determines the judgment" or "the principle which the case establishes."...

, Precedent

Precedent

In common law legal systems, a precedent or authority is a principle or rule established in a legal case that a court or other judicial body may apply when deciding subsequent cases with similar issues or facts...

, Stare decisis

Stare decisis

Stare decisis is a legal principle by which judges are obliged to respect the precedents established by prior decisions...

and Obiter dictum

Obiter dictum

Obiter dictum is Latin for a statement "said in passing". An obiter dictum is a remark or observation made by a judge that, although included in the body of the court's opinion, does not form a necessary part of the court's decision...

for a fuller explanation.)

The quoted language regarding the "complete and plenary power of income taxation possessed by Congress from the beginning" is a reference to the power granted to Congress by the original text of Article I of the U.S. Constitution. The reference to "being taken out of the category of indirect taxation to which it [the income tax] belonged" is a reference to the effect of the 1895 Court decision in Pollock v. Farmers' Loan & Trust Co.

Pollock v. Farmers' Loan & Trust Co.

Pollock v. Farmers' Loan & Trust Company, , aff'd on reh'g, , with a ruling of 5–4, was a landmark case in which the Supreme Court of the United States ruled that the unapportioned income taxes on interest, dividends and rents imposed by the Income Tax Act of 1894 were, in effect, direct taxes, and...

, where taxes on income from property (such as interest income and dividend income) — which, like taxes on income from labor, had always been considered indirect taxes (and therefore not subject to the apportionment rule) — were, beginning in 1895, treated as direct taxes. The Sixteenth Amendment overruled the effect of Pollock, making the source of the income irrelevant with respect to the apportionment rule, and thereby placing taxes on income from property back into the category of indirect taxes such as income from labor (the Sixteenth Amendment expressly stating that Congress has power to impose income taxes regardless of the source of the income, without apportionment among the states, and without regard to any census or enumeration).

The Court noted that the case "was commenced by the appellant [John R. Stanton] as a stockholder of the Baltic Mining Company, the appellee, to enjoin [i.e., prevent] the voluntary payment by the corporation and its officers of the tax assessed against it under the income tax section of the tariff act of October 3, 1913." On a direct appeal from the trial court, the U.S. Supreme Court affirmed the lower court's decision, which had dismissed Stanton's motion (i.e., had rejected Stanton's request) for a court order to prevent Baltic Mining Company from paying the income tax.

Stanton argued that the tax law was unconstitutional and void under the Fifth Amendment to the United States Constitution

Fifth Amendment to the United States Constitution

The Fifth Amendment to the United States Constitution, which is part of the Bill of Rights, protects against abuse of government authority in a legal procedure. Its guarantees stem from English common law which traces back to the Magna Carta in 1215...

in that the law denied "to mining companies and their stockholders equal protection of the laws and deprive[d] them of their property without due process of law." The Court rejected that argument. Stanton also argued that the Sixteenth Amendment "authorizes only an exceptional direct income tax without apportionment, to which the tax in question does not conform" and that therefore the income tax was "not within the authority of that Amendment." The Court also rejected this argument. Thus, the U.S. Supreme Court, in upholding the constitutionality of the income tax under the 1913 Act, contradicts those tax protesters arguments that the income tax is unconstitutional under either the Fifth Amendment or the Sixteenth Amendment.

Summary

Tax lawyer Alan O. Dixler has written:-

- Each year some misguided souls refuse to pay their federal income tax liability on the theory that the 16th Amendment was never properly ratified, or on the theory that the 16th Amendment lacks an enabling clause. Not surprisingly, neither the IRS nor the courts have exhibited much patience for that sort of thing. If, strictly for the purposes of this discussion, the 16th Amendment could be disregarded, the taxpayers making those frivolous claims would still be subject to the income tax. In the first place, income from personal services is taxable without apportionment in the absence of the 16th Amendment. Pollock specifically endorsed SpringerSpringer v. United StatesSpringer v. United States, 102 U.S. 586 , was a case in which the United States Supreme Court upheld the Federal income tax imposed under the Revenue Act of 1864.- Background :...

's holding that such income could be taxed without apportionment. The second Pollock decision invalidated the entire 1894 income tax act, including its tax on personal services income, due to inseverability; but, unlike the 1894 act, the current code contains a severability provision. Also, given the teaching of Graves [v. New York ex rel. O'Keefe, 306 U.S. 466 (1939)] -- that the theory that taxing income from a particular source is, in effect, taxing the source itself is untenable -- the holding in Pollock that taxing income from property is the same thing as taxing the property as such cannot be viewed as good law.

- Each year some misguided souls refuse to pay their federal income tax liability on the theory that the 16th Amendment was never properly ratified, or on the theory that the 16th Amendment lacks an enabling clause. Not surprisingly, neither the IRS nor the courts have exhibited much patience for that sort of thing. If, strictly for the purposes of this discussion, the 16th Amendment could be disregarded, the taxpayers making those frivolous claims would still be subject to the income tax. In the first place, income from personal services is taxable without apportionment in the absence of the 16th Amendment. Pollock specifically endorsed Springer

In Abrams v. Commissioner, the United States Tax Court stated: "Since the ratification of the Sixteenth Amendment, it is immaterial with respect to income taxes, whether the tax is a direct or indirect tax. The whole purpose of the Sixteenth Amendment was to relieve all income taxes when imposed from [the requirement of] apportionment and from [the requirement of] a consideration of the source whence the income was derived."

External links

- Tax Protester FAQ - specific rebuttals concerning the ratification of the 16th amendment

- The Truth About Frivolous Tax Arguments- The official response of the IRS.