Bull spread

Encyclopedia

In options trading, a bull spread is a bullish, vertical spread

options strategy that is designed to profit from a moderate rise in the price of the underlying security.

Because of put-call parity, a bull spread can be constructed using either put option

s or call option

s. If constructed using calls, it is a bull call spread. If constructed using puts, it is a bull put spread.

with a low exercise price (K), and selling another call option with a higher exercise price.

Often the call with the lower exercise price will be at-the-money

Often the call with the lower exercise price will be at-the-money

while the call with the higher exercise price is out-of-the-money

. Both calls must have the same underlying security and expiration month.

Assume that for next month, a call option with a strike price of $100 costs $3 per share, or $300 per contract, while a call option with a strike price of $115 is selling at $1 per share, or $100 per contract.

A trader can then buy a long position on the $100 strike price option for $300 and sell a short position on the $115 option for $100. The net debit for this trade then is $300 - 100 = $200.

This trade results in a profitable trade if the stock closes on expiry above $102. If the stock's closing price on expiry is $110, the $100 call option will end at $10 a share, or $1000 per contract, while the $115 call option expires worthless. Hence a total profit of $1000 - 200 = $800.

The trade's profit is limited to $13 per share, which is the difference in strike prices minus the net debit (15 - 2). The maximum loss possible on the trade equals $2 per share, the net debit.

Assume that for next month, a put option with a strike price of $105 costs $8 per share, or $800 per contract, while a put option with a strike price of $125 is selling at $27 per share, or $2700 per contract.

A trader can then open a long position on the $105 strike put option for $800 and open a short position on the $125 put option for $2700. The net credit for this trade then is $2700 - 800 = $1900.

This trade will be profitable if the stock closes on expiry above $106. If the stock's closing price on expiry is $110, the $105 put option will expire worthless while the $125 put option will end at $15 a share, or $1500 per contract. Hence a total profit of $1900 - 1500 = $400.

The trade's profit is limited to $19 per share, which is equal to the net credit. The maximum loss on the trade is $1 per share which is the difference in strike prices minus the net credit (20 - 19).

Vertical spread

In options trading, a vertical spread is an options strategy involving buying and selling of multiple options of the same underlying security, same expiration date, but at different strike prices...

options strategy that is designed to profit from a moderate rise in the price of the underlying security.

Because of put-call parity, a bull spread can be constructed using either put option

Put option

A put or put option is a contract between two parties to exchange an asset, the underlying, at a specified price, the strike, by a predetermined date, the expiry or maturity...

s or call option

Call option

A call option, often simply labeled a "call", is a financial contract between two parties, the buyer and the seller of this type of option. The buyer of the call option has the right, but not the obligation to buy an agreed quantity of a particular commodity or financial instrument from the seller...

s. If constructed using calls, it is a bull call spread. If constructed using puts, it is a bull put spread.

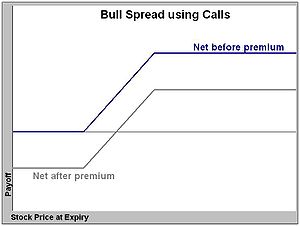

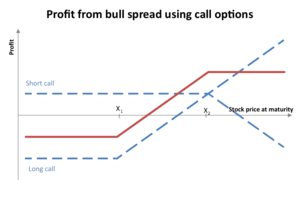

Bull call spread

A bull call spread is constructed by buying a call optionCall option

A call option, often simply labeled a "call", is a financial contract between two parties, the buyer and the seller of this type of option. The buyer of the call option has the right, but not the obligation to buy an agreed quantity of a particular commodity or financial instrument from the seller...

with a low exercise price (K), and selling another call option with a higher exercise price.

Moneyness

In finance, moneyness is a measure of the degree to which a derivative is likely to have positive monetary value at its expiration, in the risk-neutral measure. It can be measured in percentage probability, or in standard deviations....

while the call with the higher exercise price is out-of-the-money

Moneyness

In finance, moneyness is a measure of the degree to which a derivative is likely to have positive monetary value at its expiration, in the risk-neutral measure. It can be measured in percentage probability, or in standard deviations....

. Both calls must have the same underlying security and expiration month.

Example

Take an arbitrary stock XYZ currently priced at $100. Furthermore, assume it is a standard option, meaning every option contract controls 100 shares.Assume that for next month, a call option with a strike price of $100 costs $3 per share, or $300 per contract, while a call option with a strike price of $115 is selling at $1 per share, or $100 per contract.

A trader can then buy a long position on the $100 strike price option for $300 and sell a short position on the $115 option for $100. The net debit for this trade then is $300 - 100 = $200.

This trade results in a profitable trade if the stock closes on expiry above $102. If the stock's closing price on expiry is $110, the $100 call option will end at $10 a share, or $1000 per contract, while the $115 call option expires worthless. Hence a total profit of $1000 - 200 = $800.

The trade's profit is limited to $13 per share, which is the difference in strike prices minus the net debit (15 - 2). The maximum loss possible on the trade equals $2 per share, the net debit.

Bull put spread

A bull put spread is constructed by selling higher striking in-the-money put options and buying the same number of lower striking in-the-money put options on the same underlying security with the same expiration date. The options trader employing this strategy hopes that the price of the underlying security goes up far enough such that the written put options expire worthless.Example

Take an arbitrary stock ABC currently priced at $100. Furthermore, assume again that it is a standard option, meaning every option contract controls 100 shares.Assume that for next month, a put option with a strike price of $105 costs $8 per share, or $800 per contract, while a put option with a strike price of $125 is selling at $27 per share, or $2700 per contract.

A trader can then open a long position on the $105 strike put option for $800 and open a short position on the $125 put option for $2700. The net credit for this trade then is $2700 - 800 = $1900.

This trade will be profitable if the stock closes on expiry above $106. If the stock's closing price on expiry is $110, the $105 put option will expire worthless while the $125 put option will end at $15 a share, or $1500 per contract. Hence a total profit of $1900 - 1500 = $400.

The trade's profit is limited to $19 per share, which is equal to the net credit. The maximum loss on the trade is $1 per share which is the difference in strike prices minus the net credit (20 - 19).